End of Summer Portfolio Update

End of Summer Portfolio Update

16% YTD

While I was relaxing on the beach, my portfolio positions have been releasing important results. Now that I'm back in the office and my positions are back to quiet mode, I feel like it's time for a portfolio update.

When someone asks me how I feel about 2024, the first word that comes to mind is: odd.

ChatGPT-fueled AI narrative continues to dominate the headspace and animal instincts of most fund managers, and everyone appears to be shaking off any negative news coming from around the world. And there are many.

I guess as long as Mag7 is still „going up,“ this can and will remain the status quo.

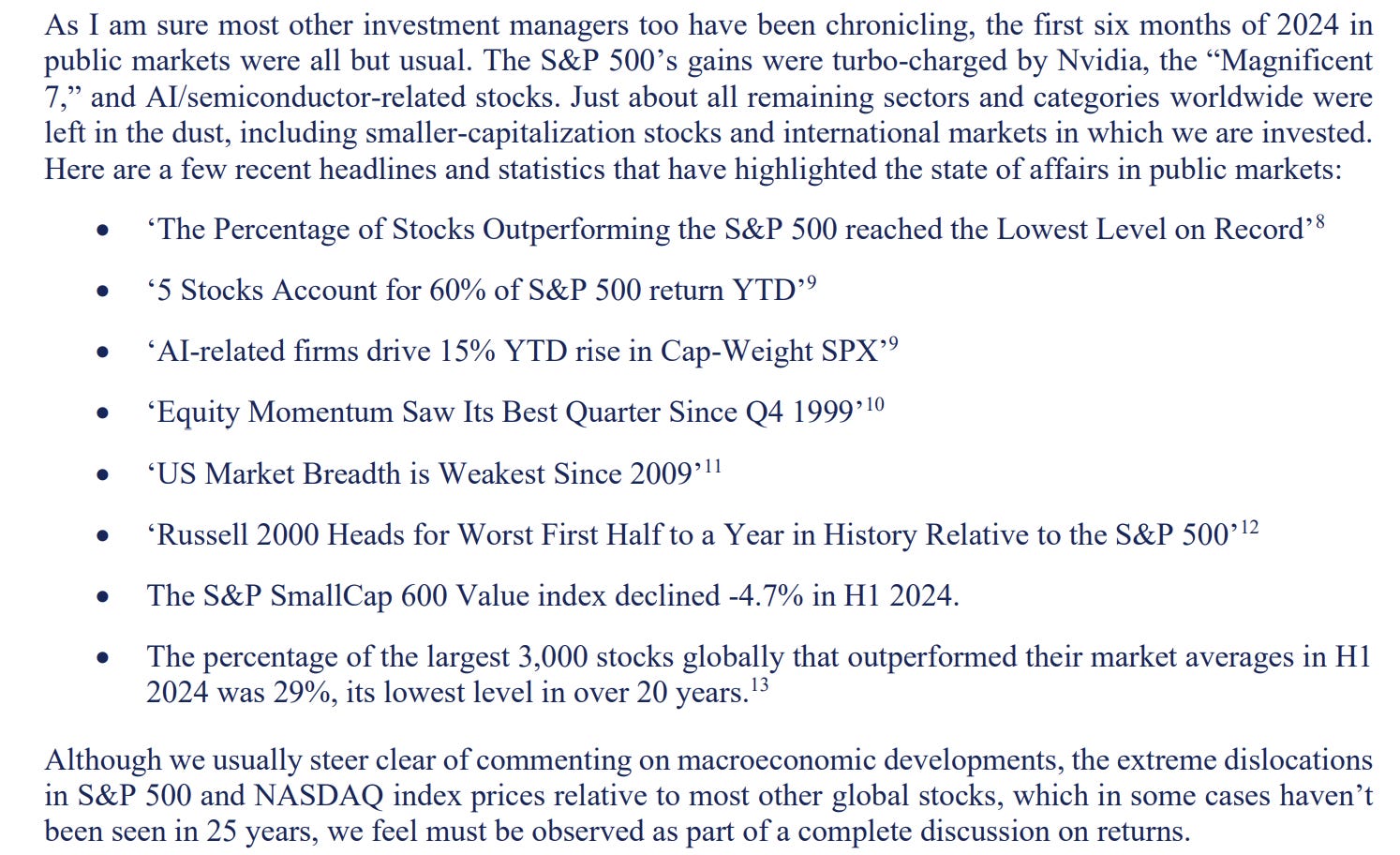

Jon Cukierwar and his Sohra Peak Capital provided a far better overview of “YTD state of the markets” than I ever could, so I might as well highlight it here:

I'd say I'm pleased I wasn't left in the dust and with how my year is going. Despite the fact that I held no AI-related stocks, no Mag7, no tech, and no US large caps and am mostly concentrated in international micro-cap names, I've managed to slightly outperform the market.

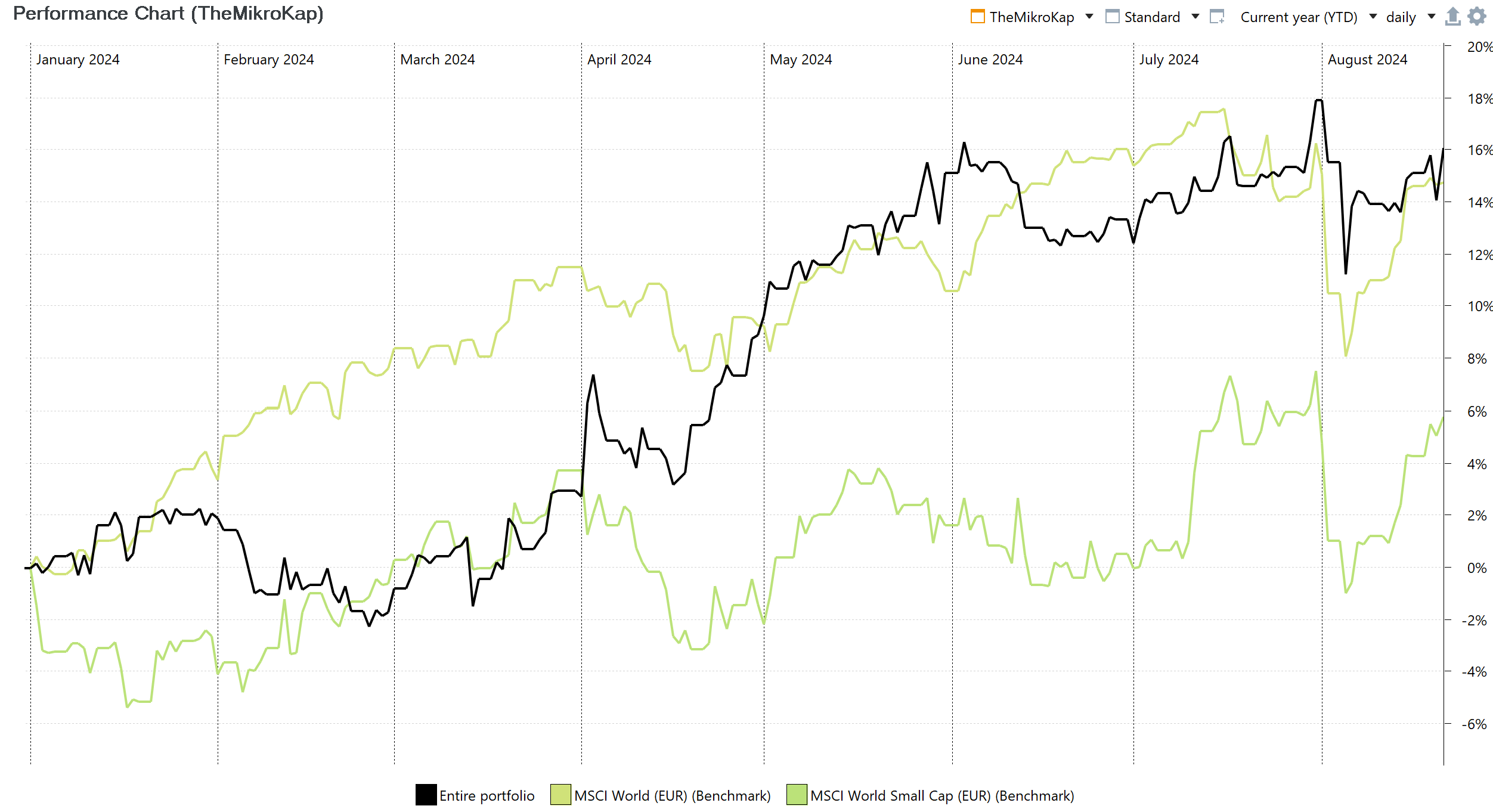

At the moment I'm writing this, my returns are 16.3% YTD, compared to 14.9% for MSCI World (my opportunity cost, where I would index all my money there if I wasn't stock picking) and 5.9% for MSCI World Small Cap index (an index to double check if I am a good stock picker or if my current strategy is only working because I am “going smaller")

As I've stated numerous times, I don't think in terms of benchmarks and couldn't care less whether I outperform or underperform over a short period of time. This short-term insignificance of my strategy was most evident this summer; I was up 18.1% YTD on July 31st, up (only) 11.4% on August 5th, and now up 16% YTD two weeks later. There's literally nothing to take away from this; I wasn't a good investor in July, and I wasn't a poor one a few days later. It's just volatility or a short-term price to pay for long-term riches. However, given I had already decided to embark on a journey of sharing all my buy/sell decisions publicly, I shared the picture above for anyone who might be interested. And I'll keep doing it with all of the following portfolio updates.

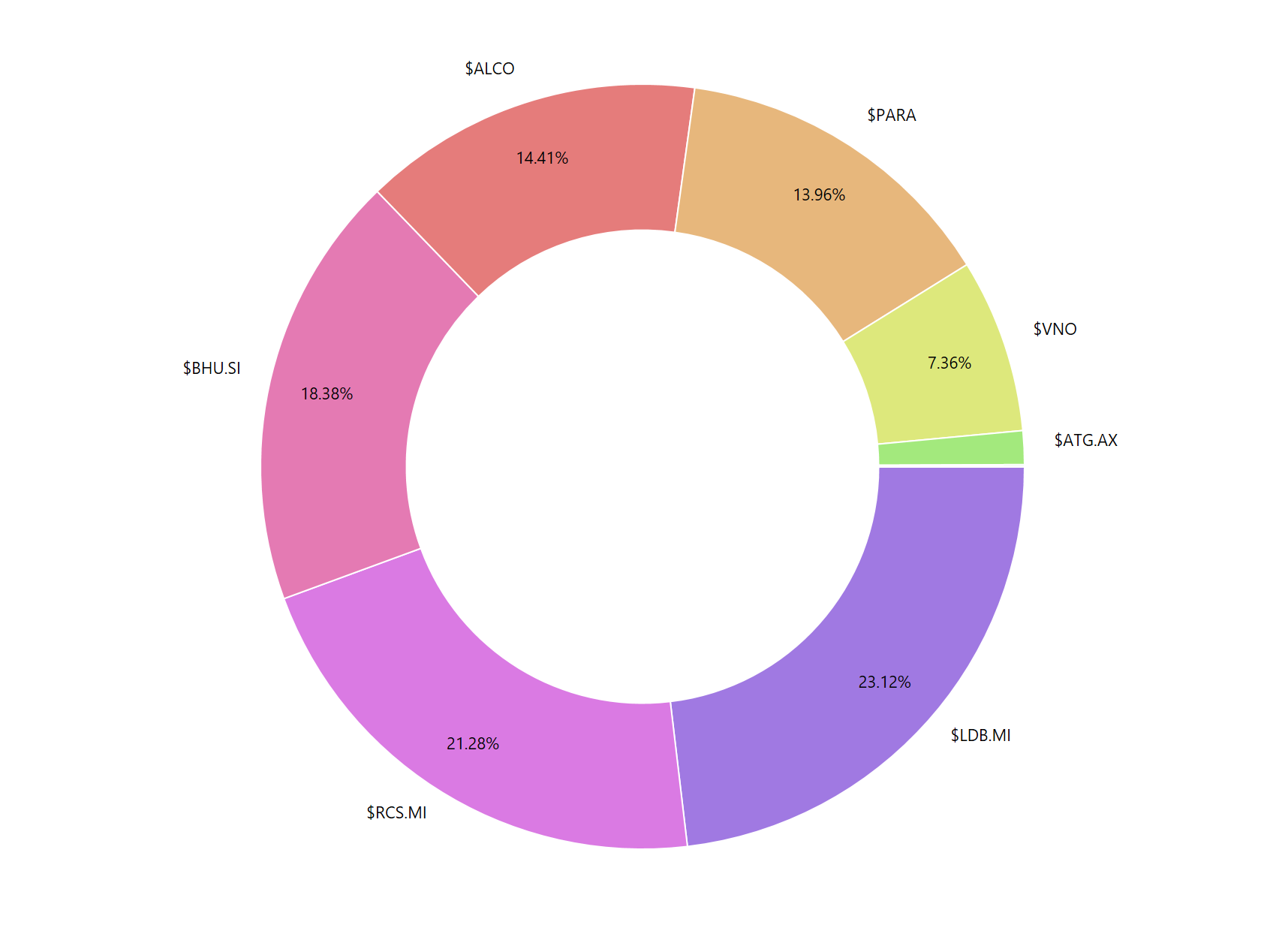

As of 21/8/2024 TheMikroKap portfolio looks like this.

I remain concentrated in the lower end of my (current) sweet spot of 6–8 portfolio positions. As is the case now and has been for the past year or two, I have more ideas than money, which is why I expect my cash position to remain low and my portfolio turnover to be relatively high.

I believe that in a few years' time, this type of market will prove to be a blessing in disguise. For anyone who views illiquidity as a friend and for anyone who is immune to the siren song of the broader indices. Buffett keeps having trouble deploying his cash pile since his opportunity set of large and megacap stocks is far too expensive. On the other hand, we, micro-cap investors, despite missing billions in our pockets, should consider ourselves lucky to be able to buy dirt-cheap and attractive ideas in any market environment. Regardless of how frothy the indices get.

Now onto the important stuff. Business, results.

Business results

$ ATG.AX

Articore is by far the tiniest piece of my portfolio and one of two positions in which I am currently underwater on YTD. As I indicated in my March write-up, it's the only company I own that has no downside protection and the only bet I consider somewhat speculative. Nonetheless, with 423M in revenue, a market cap of less than 100M, a large net cash position, and a decent chance of returning to profitable revenue growth with operating leverage kicking in, I still believe that the risk-reward is asymmetric enough for me to want to own a small position. Especially now that it's demonstrated that it can be cash flow positive.

My general rule of thumb for positions that lack a proper downside protection is:

Always size them small

Don't allow them to take a lot of head space

Follow the quarterlies and add when the downside gets taken off the table or sell immediately when gut tells you the bears were right, and the business model is actually structurally unprofitable

I wasn't pleased with yesterday's H2 results, which you can read about here

$ VNO

Vornado continues to demonstrate why it is „the closest thing to a never-sell that I have in the portfolio.”

The last few quarters have shown that both Manhattan's and Vornado's occupancy appear to be nearing or have reached a bottom. Leasing activity has also been improving for some time, and rents for quality buildings are increasing.

The lack of supply of quality office space, along with PENN assets becoming crowded with tenants are positioning VNO for a business inflection in the next few years. And if interest rates and WFH change from being a headwind to being a tailwind, for any reason whatsoever, I'm looking at a home run investment.

Roth said it best on the earnings call:

“New York City is as crowded as ever, and that's a good thing. As I predicted over the past couple of years, working at the kitchen table wasn't an existential threat. We now see building utilization percentages in the '70s, and that's just about normal. Tenants are expanding and growing and actively searching for space.We actually competed in a market of over 200 million square feet. And in many of the prime submarkets, good spaces being eaten up and rents are rising. It may be that the most important dynamic in our market is that it is almost economically impossible to build new, thereby cutting off new supply. There hasn't been a new office building of size started in New York in the last 5 years. If history is a guide, when supply shuts down, it quickly leads to a landlord's market.” ~Q2 2024 earnings call

Another fun fact about VNO is that only 12-18 months ago, the sentiment was so bad that nearly all analysts were rounding up its retail operations to 0. Zero.

Fast forward to today, and most investors consider retail to be the crown asset of Vornado's portfolio.

Just this month, Vornado began selling some of its Fifth Avenue retail, and the management believes that the remaining retail footage is worth about 16$ a share, or nearly half of the current 34.5$ price. Coincidentally, that happens to be the exact cost basis for my $VNO position.

$ PARA

Paramount was one company this year where I deviated from my micro-cap specialty and decided to buy „disgust“ in the SMID cap land. Little did I know this would turn out to be the most exhausting story I've ever been involved with. John Rogers, founder of Ariel Investments, summarized it well:

„Ariel has been in business for 41 years. We've not seen anything remotely like this. It's just extraordinary.“

I haven't been in business for nearly that long, but I very much agree with his take. If I had known what I was getting myself into at the time, I would never have made this bet.

Nonetheless, maybe it's the commitment bias speaking, maybe I'm rational, but even today, I feel more uncomfortable selling my position into chaos at this valuation at the absolute trough earnings with the business about to inflect, than holding it through and waiting for bright days without dilution under Edgar Bronfman Jr. or tolerable days under Ellison.

I could write a 10,000-word essay covering everything Paramount related since I first initiated my position, however, I know most of you came here for micro-caps and not Paramount. For those interested in hearing my full thoughts, simply go to my Twitter profile and key in $PARA to read what I was thinking in real time as events unfolded. It reads like a journal, but be warned: there are a lot of tweets.

Or if there is enough interest, please let me know in the comments, and I'll make a dedicated Paramount update article.

The thing that bothers me most about Paramount, aside from the time lost while sitting at a loss, is that my original thesis, which claimed that Paramount should be valued as SOTP based on the private market value, was correct. I knew Shari wanted to sell, I knew there were interested parties prepared to pay a much higher price than Paramount was trading for at the time, and I knew that this would happen rather quickly. Many may argue now that this was obvious at the time, but I think that's the hindsight speaking, and I vividly recall that 99% of market participants believed in none of those things, including everyone to whom I pitched the stock at the time. „Far fetched“ was the answer I got. Just read older SA articles or sell-side research reports.

It wasn't until Byron Allen bid that things started to heat up. Unfortunately, while I was right directionally, there was one thing I heavily understimated. Bad corporate governance. If I wind up losing money on this idea after all, I think I should tattoo on my forehead Buffett's quote, „You can't make a good deal with a bad person.“

And if you ask any of the former or current $PARA shareholders, they will all tell you Shari is a bad person. Could I have predicted/known that she would do all in her power to „preserve the legacy“ or wring one extra penny from the Ellisons, no matter how much it harms the minority shareholders? Maybe I could. I don't know.

Ironically, by engaging in this type of forced-meger maneuver, she did the complete opposite and harmed her name and legacy.

Okay, enough with the rant.

The drama continues and, just yesterday, the go-shop period was extended for another 15 days due to a higher 6B counter offer from Edgar Bronfman Jr. There aren't enough details available for me to form a firm opinion but as long as I'm avoiding heavy dilution, I'll take anyone over Skydance and Ellison. Also, a higher Ellison bid or a sweetener for minorities is likely IMO.

$ ALCO

I wrote about Alico in July and there has been nothing valuable to add since then.

$ BHU.SI

SUTL Enterprise, which I believe is the highest barrier to entry business in my portfolio, reported disappointing H1 2024 results. It's not that they are bad, far from it, especially at this valuation. However, for a business of this caliber in a growing industry, I'd anticipate stronger revenue/PBT growth than 3-4%. Especially now that Nirup Island is operational, extra berths have been added, and Sentosa was configured to allow for larger yacht accommodations.

On a positive note, with a conditional sales and purchase agreement signed, it appears that the new marina in Phuket, Thailand is finally close to reality and will most likely be something to „move the needle“ for SUTL. I'm neither bullish nor bearish on Phuket until I see the price paid and how the deal is structured.

While I wait for higher growth, Sentosa lease renewal, or for a (part of) massive cash pile to be deployed in Phuket, SUTL will be paying me a 5-cent dividend, or 7.5% yield on the current price. And as long as the revenue is not declining, and the net cash pile is almost as large as the market cap, I sleep soundly knowing I own this one in size.

PS if anyone (local) has a way to reach the management for a 1 on 1 call or has talked to them in the past, I would appreciate the help.

$ RCS.MI

RCS Media maintained its dominant leading position in both Italy and Spain while growing its profits and cashflows at a satisfactory rate. Importantly, following the H2 2023 results, Cairo decided to increase the already large dividend by 16.7% to 7 cents a share, which is a 9+% yield on the current share price of 75 cents.

The one thing I don't like about RCS's recent performance is that despite significant digital subscriber growth, there has been no impact on the digital revenue, implying they weren't able to properly monetize them (yet).

Given that RCS grew EBITDA 10% in H1 2024 and trades for less than 4X EV/EBITDA, I'll let this slide for now.

As I stated in my January portfolio update, it's up to Cairo, who I believe to be the best media executive in Italy, to decide how quickly or slowly I make money on this one. Until there's a word from him, I'll collect my growing 9% dividend cheques.

You can read my comments on RCS’ FY 2023 and H1 2024 here and here

$ LDB.MI

Lindbergh is responsible for the vast majority of my performance in 2024. It's up 69% (nice)YTD and has earned its spot as my largest holding. From the interview with the CEO to a deep dive, scuttlebutt notes, and the interview with a large customer, I've already covered it extensively on my blog.

Aside from these, the most important things to highlight in 2024 are the two major acquisitions that occured in the recent few months, gaining Lindbergh the reputation of a serial acquirer. You can find my comment about the two HVACquisitions here and here.

After building a large position in $LDB.MI at 2.08 euros last fall while paying a higher FCF multiple than I usually do, I found it difficult not to take some gains off the table once it reached 4 euros. I'm glad I didn't because I believe that their transition to HVAC and strong execution made me confident that they'll grow into the current valuation in no time. And it's not everyday that I come across a company where I have seen everything firsthand and am likely among the best-informed market participants.

Sell decisions

Aside from the progress from my portfolio companies, I think it would be worth mentioning two positions I sold in 2024: Nisshin Group and Card Factory. The former was a matter of opportunity cost whereas the latter was an error in my analysis. You can read the complete rationale behind my sell decisions here and here.

That concludes my portfolio update, but before we go, I'd like to provide an update for this blog as well.

Quick blog update

TheMikroKap has reached a scale that I never expected. I'm excited to write more, and I've made some "moves" in my life that will allow me to do even more micro-cap-focused research than before.

So going forward I plan to be more active here, even publishing research on companies I do not own but still find fascinating, as well as other overlooked ideas I find actionable. Also, I think it would be more convenient for readers if I covered major developments and all my buy/sell decisions in the Substack subscriber chat rather than on Twitter, so you can stay up to date on everything without having to follow me there. If you have any suggestions on where I could take this blog, feel free to leave a comment or DM me. If you wish to come along for the ride, feel free to subscribe.

Thank you for reading!

This is NOT investment advice. All content on this website is for entertainment, informational, and educational purposes only and should not be considered to be advice of any nature. Due your own due diligence.

Great work, cook up that PARA update! One of the most twisted stories I've invested in, curious about your insights here. Personally, adopting a similar approach -- will do my best not to get shaken out along the ride (unless there's a red flag like a confirmed plan to heavily dilute)

I've been following your newsletter since my sophomore year of college, and I can't express enough how valuable it has been to my market journey. Your analysis has been instrumental in teaching me how to properly analyze companies. You've opened my eyes to the fact that there's value in unexpected places and have encouraged me to look at companies I would have never considered before. It's fascinating how you've helped transform my perspective on finance and investments - I never thought I'd pursue a career in this field, but after exploring various majors and internships, I find myself fully immersed in it, largely thanks to your influence. The recent Alico report particularly resonated with me as a Florida native. Your analysis of the citrus industry in my home state was not only interesting but also gave me a new appreciation for local industries I hadn't considered from an investment standpoint before.

Thank you for consistently providing such insightful and educational content. Your newsletter has truly help shape my professional path and continues to enhance my ability to mentally model investment scenarios. Keep up the fantastic work!