Adventures in the value trap land

Nisshin Group Holdings, $8881.T investment thesis

I've spent the last few weeks turning over Japanese rocks that are selling for less than 0.7x P/B and 1x P/NCAV in an effort to find cheap companies that could benefit from the recent corporate governance push in Japan and potentially adjust their capital allocation strategy. Based on my observations, I can confidently say that no country has more value traps than Japan. Most of these companies have no desire to generate returns for shareholders, do not deserve your capital, and exist solely because of the Japanese culture of being overly conservative and hoarding unreasonable amounts of cash on the balance sheet.

Luckily, there are always exceptions to the rule, and Nisshin Group Holdings is one such exception.

Nisshin Group ($8881.T) is a Japanese net-net that's actually a stable value-creating business with improving capital allocation at play, selling for 0.45x P/NCAV and 0.35x P/B.

Quick business overview

Nisshin considers itself a „comprehensive“ real estate corporation with 14 different subsidiaries operating in 3 major segments:

1) Real Estate segment

The cornerstone of the RE segment is Nisshin Real Estate, a subsidiary engaged in the business of purchasing and selling condominiums in the Tokyo Metropolitan area. Essentially, they are RE flippers who buy land, build a new building on top of that land, and sell condos inside that building as quickly as possible. It takes an average of 1.5 years from the time the land is purchased to the time the condos are sold. Its target market consists of either singles or DINKS (dual income, no kids), with a preference for female buyers.

Recently, Nisshin has successfully widened its offering and increased margins within the RE segment by managing assets for large institutional investors in the form of private placement REITs. And by buying run-down condos and detached houses, renovating them, and quickly reselling them for a profit.

2) Construction segment

Subsidiaries within the construction business build condos for the Group and third parties, as well as do some civil engineering work. Recently, they have started to extend into the development of schools and health care facilities for the elderly.

3) Real estate management segment

In this segment, they carry out long-term management of buildings, rental properties, and condomium common areas, as well as renovations, and act as a broker/agent for interested parties. This is by far the highest-quality part of the company due to the higher margin, asset-light recurring nature of the business, which is more resilient to economic downturns than construction or even the RE segment.

On paper, the company appears very cyclical, yet in the last 20 years, Nisshin has only had one year of negative profitability, which is understandable given that it happened in 2009, in the midst of the financial crisis. Most years, the company is value creative and easily generates >8% ROE and ROIC (and that's including a cash-heavy capital structure). Its book value has doubled in the last 10 years.

Now that we've covered the basics, let's look at what makes this investment attractive.

Anti-Japanese capital allocation

The reason why most Japanese net nets end up as lousy investments are

1) cash on the balance sheet is unlikely to ever be distributed; hence EV should not be used as a numerator

2) cash generated is reinvested at low rates of ROIC, so it should not be valued on a FCF basis, and P/B is unlikely to rerate

3) businesses are still expensive in terms of earnings or dividend valuation

Sometimes some investors get lucky and their stocks revalue e.g. from 0.3x book to 0.45x book, but that requires exceptional timing and the courage to buy a business that is so terrible that investors are valuing it at 0.3x book. So...more often than not, if the capital allocation doesn't suddenly improve, your total return, in the long run, will be equal to the dividend yield.

Nisshin Group was exactly that type of company—that type of value trap. Although it did reinvest some of its earnings at a decent ROE, this was insufficient to pique investors' attention.

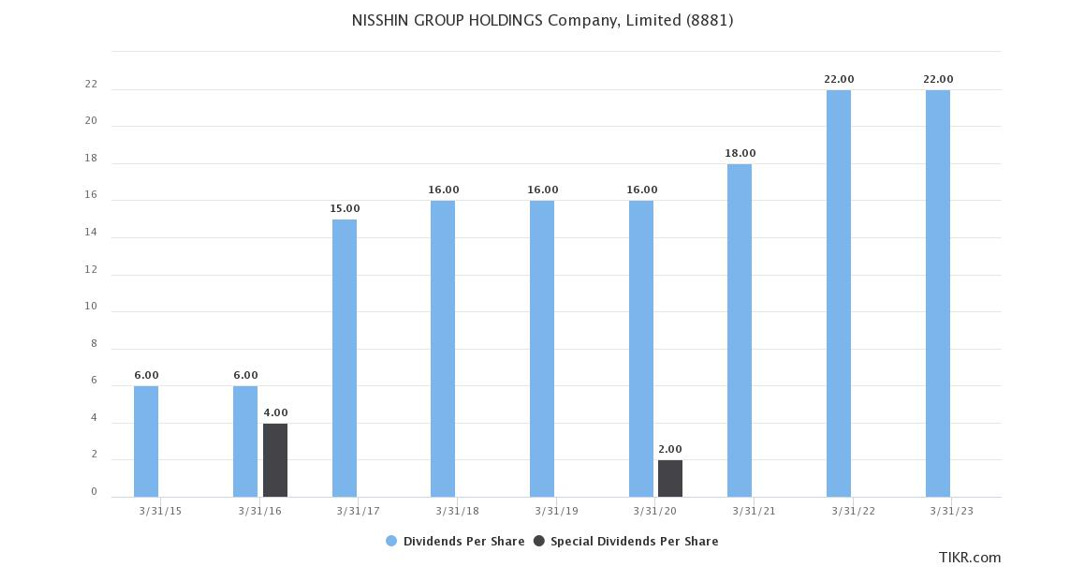

Things began to change in 2016 when management started to prioritize shareholders and capital allocation. The payout ratio has consistently increased from a meager 7% in 2016 to 37% LTM. Moreover, Nisshin paid special dividends in 2016 and 2020, and its dividend has almost quadrupled since, rising from 6 yen in 2015 (1.5% yield at the time) to 22 yen per share LTM (a 4.5% yield on the current share price).

Further, this section was added to the latest annual filing, which came out around a month and a half ago.

This is, without a doubt, the most important section of the annual report. The section that IMO will make a difference between a classic Japanese value trap and potentially dirt-cheap investment.

For starters, this was the first time in history they ever used terms like COC, ROC in their filings or showed concern about stock price performance.

Secondly, the dividend payout ratio was dramatically increased again, from „at least 30% policy" in 2022 to „at least 50% payout" in 2023.

Now let's do some math on the dividend yield going forward. First, let's conservatively assume that, due to an aging population and declining birth rates, the population of Tokyo won't grow as it has in the past, and Nisshin's expansion into other business lines/segments/geographies won't be able to compensate for the slow decline in RE buy-build-sell business.

In this situation, Nisshin's next 10 years will be the same as the previous 10 years, and the average earnings Nisshin can generate are 3.8B yen.

The current market cap is 23 billion yen (165 million USD). Therefore, the normalized earnings yield is 16.5%, and the average dividend yield that investors may expect on a 50% payout ratio is at least 8.25%.

During my adventures in Japan's micro-cap land, I noticed that the majority of Japanese companies either don't pay a dividend or offer a dividend yield of only 2-3%.

I believe that once investors realize that Nisshin could/will pay them an 8%+ dividend at cost vs a historical mean of 2.5%. They won't be able to „ignore“ it any further and will rerate the stock to a more appropriate multiple. (more on this later)

Show me the incentive and I’ll show you the outcome

Another factor supporting Nisshin's readiness for revaluation is recent changes in remuneration and retirement benefits policy for managers, which now provide management with shareholder-aligned incentives for unlocking the value of the business:

(quote)

At the 47th Ordinary General Meeting of Shareholders to be held on June 25, 2021, the Company will abolish the retirement benefits system for directors, clarify the linkage between director remuneration and stock value, and allow eligible directors to receive benefits from rising stock prices. In addition, by sharing with our shareholders the risk of stock price declines, we have established a stock compensation plan for directors, which aims to raise awareness of contributing to improving medium- to long-term business performance and increasing corporate value.

Based on the resolution of the 47th Ordinary General Meeting of Shareholders held on June 25, 2021, the Company will provide directors (excluding outside directors) by clarifying the linkage between remuneration and stock value, and by having eligible officers share with shareholders not only the benefits of rising stock prices but also the risks of falling stock prices, we will improve medium- to long-term business performance and increase corporate value.

Valuation scenarios:

In the bear case, the company is hit by an economic slump or below-average industry trends in the construction of condos persist for an extended period of time. The stock drops or moves nowhere until the "normal environment" comes along. In this case, the dividend yield serves as a margin of safety, and I'm paid to wait. This also gives zero credit to potential reinvestment opportunities or the fact that the company is selling for 0.35x book value while achieving 10-yr and 20-yr median ROE of 8%.

Or that its cash + accounts receivables – total liabilities are worth more than the current market cap.

IMO, net nets are best valued using the combination of dividend yield (or ROE, in some obscure cases) and NCAV/book multiple. However, another way to handicap the downside can be achieved using the standard earnings valuation. To make sure that the company is too cheap, regardless of the metric:

Calculation: In most years, the RE segment can generate at least 2B in EBIT. The construction segment comfortably did 3-3.5B before COVID, but due to the cyclical nature of the company, let's cut it to half of that and assume it can only make half of the lower range, or 1.5B in EBIT moving forward. The RE management segment is the most resilient one, and I would be surprised if they reported anything less than 1.2B in the future.

That brings us to 4.7B in EBIT in a below-average lousy environment. At the current price, you'd be paying only 5x P/EBIT for such financials. And - yes, I'm giving zero credit to the cash, otherwise, EV/EBIT ratio would be negative.

In the base case scenario, the business will remain stable and generate at least 7% historical EBIT margins on this revenue base going forward, and if you slap a conservative 8XEBIT multiple on that price, it's double from this share price.

When looking at net nets in Japan, I also like to see if the company has ever traded above 1xP/NCAV. If it did, it gives me more confidence that it will do so again. Especially if the capital allocation is better than it has been in the past, as it is in this case. Nisshin did trade around 1-1.2xP/NCAV multiple in the 2017–2018 period. And around 0.9–1 Xncav in 2013–2014. The current valuation is only 0.45x NCAV. It'll be an easy double just on sentiment once investors notice the high dividend or industry trends return to normal.

Bull case: management executes its medium-term plan, the population influx continues, and Nisshin continues with the successful expansion of its offering (you can learn more about the specifics in the investor presentation). Nisshin hits its goal of being a company that generates sales of more than 100 billion yen in a stable manner by 2027. If we assume 8%–10% margins on that revenue base. And slap a 10 to 12 P/EBIT multiple (again giving zero credit to a significant net cash position). The stock will do 350–500%. IMO, this scenario is not a stretch.

Why does this opportunity exist:

-low institutional ownership, no analyst coverage since 2010, and only one mention on social media (that I'm aware of)

-risks of an economic downturn

Virtually everything connected to construction or real estate is currently out of favor with investors. However, even if 2009 were to happen again, the company wouldn't go under due to its balance sheet strength, which has improved since the 2008/09 period and now has less RE inventory and more cash. A quick glance at 60B in cash and 18B in receivables compared to 55B in total liabilities makes me sleep well at night.

-the number of condominium construction starts, including condominium development, has been sluggish since 2017, which affected Nisshin's construction segment and part of the RE segment. This is a serious risk and could be structural in nature. Most likely, they'll have to diversify away from the Tokyo Metropolitan area or from mostly condo construction in the long term. I’ll monitor.

-otherwise stable gross margins fell in 2023 as a result of increased raw and building material costs, as well as labor costs in construction. I don't believe this to be structural, and the GM trend is perfectly explainable

-the long-term risk of an aging population and falling birth rates. Another valid risk. However, since demographics change slowly, Nisshin has more than enough time to adapt to the „new environment" and expand into other parts of Japan or focus their attention on more recurring parts of their business. Also, some common sense tells me that Tokyo is one of the few cities in the world that “won't go out of style.”

-guiding only 3.7B in EBIT and 2.1B in net income next year (only a short-term hurdle)

Conclusion: I expect a 2–5x return over the next 2-4 years, with a large margin of safety due to the extremely conservative balance sheet and the combination of dirt-cheap valuation and a positive change in capital allocation.

Disc: long (7% position at 497 yen per share)

This is NOT investment advice. All content on this website is for informational and educational purposes only and should not be considered to be advice of any nature. Due your own due diligence.

Good write up on a very cheap name! Also long :)

Really enjoyed this one - thanks