Given that it has already been 6 months since I first bought Card Factory and the stock is currently trading only slightly above my average purchase price, I decided to send you guys a short and sweet thesis on why I believe $CARD.L is an attractive opportunity.

The habit

Card Factory is a greeting card and other “celebration essentials” retailer operating primarily in the UK. What is unique about the Northern Europeans, particularly the British, is their habit of buying greeting cards. It is ingrained in their culture. Much like 5 PM tea, greeting cards and Brits go hand in hand. For instance, in FY2023, 80% of the adults in the UK bought a greeting card. And this is even greater than the 76% pre-pandemic figure. If I had to guess, individuals in the remaining 20% are either the ones who are too lazy to do their greeting card shopping for themselves or the ones who regrettably have no friends or family to share them with.

Moreover, the average number of cards bought per UK adult during the year was 20. They essentially purchase them for each and every occasion for their loved ones. Even when you get a new dog, or switch jobs, people give you cards. The culture is also popular among the younger folks who bought 24 cards on average throughout the last fiscal year and drove market growth in recent years. It feels personal to them and is a nice way to connect with others.

Biz model

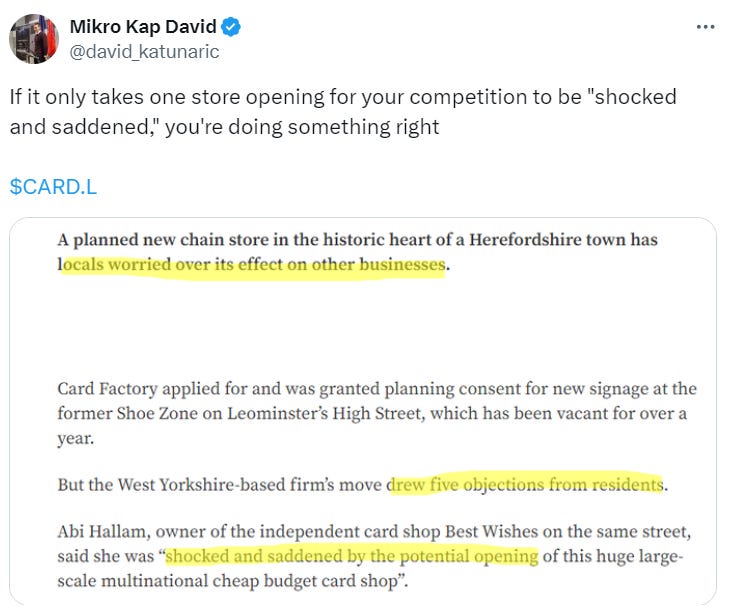

Card Factory is the largest retailer of cards in the UK, cornering around a third of the market. Their advantage stems from vertical integration, which means they design and print around 80% of their cards in-house, whereas their competitors are primarily supplied mostly by two suppliers, Hallmark and American Greetings. “The Big 2” suppliers have a strategy of holding a small amount of shelf space but in a variety of places, like grocery stores. Of course, they always price their cards high due to the limited volume of cards purchased by their customers, taking a huge cut (analysts who have done scuttlebutt research claim as high as 40%).

Moreover, with the industry in a “slow decline mode” and experiencing major challenges during COVID, CARD’s pure-play competitors were closing stores or going bust. Hence the only thing American Greetings and Hallmark could do to maintain the same level of profits is to squeeze them even more and hike prices, further entrenching CARD‘s position as by far the lowest-cost player in the industry.

This kind of model enabled Card Factory to gain considerable market share and vacant space from its competitors over the years thanks to its low-cost advantage, with prices being as low as half of the main rival’s prices.

Owned production also allows them to have the widest card selection in town and to respond to changes in customer preferences faster than competitors.

Another appealing aspect of this model is that it is essentially capex-free. They lease out all their stores and are in high demand among tenants, with only 1% of their locations losing money. CARD targets a 3-year break clause for their leases, so they are flexible, and if the high-street footfall changes and the stores begin to underperform, they can quickly move or even demand rent reduction.

Furthermore, its inventory is financed by its suppliers resulting in a negative working capital cycle. The only large fixed asset they own is the production plant for designing the cards which has allowed them to generate extremely high returns on invested capital over the years.

In theory, tangible equity being negative in the past means that the returns up to this point have been infinite because new store openings didn’t require further capital to be deployed. Hence new growth is welcomed.

Future expectations

Going forward, Card Factory aims to open 90 new locations by 2027. (they currently operate 1043). Moreover, following the success of their large retail partnership with Aldi, they are actively expanding a new, comparable one with Matalan, available across their entire UK estate of 223 stores. CARD is also expanding franchise agreements in the Middle East and wholesaling arrangements in South Africa. These deals recorded 23.5% revenue growth in H12024 and should be a low-risk approach for CARD going forward because they don’t require additional capital to be employed while allowing them to utilize the unused capacity in their Yorkshire facility.

As printing quantities increase, they do not have to create additional designs for each new card, resulting in a lower incremental cost for each new card. Or, simply put, you may spread fixed design and printing costs over a much larger base.

In the following years, Card Factory aims to increase the average basket size by becoming a one-stop shop for the broader celebration events market and has recently started adding new categories to their offering, such as flowers, booze, chocolate, books and balloons. This plan makes a lot of sense IMO because 70% of gifts are bought with the card, however, it does run the danger of the business model becoming more seasonal and inventory-heavy.

Catalyst

Debt covenants during COVID barred them from paying dividends. This expired in January of this year, and I expect them to announce a dividend when the FY2024 results are out later this month. And based on their dividend cover policies, we should get between a 5–8% dividend yield at the current price. I also expect dividends to grow over time now that increased capex connected to store refurbishments, IT infrastructure and ERP capex is coming to an end.

Valuation

At the current price of 94 GBX, Card Factory is trading between 4-6x EV to normalized owner earnings I expect them to generate annually (on average) in the foreseeable future. A beautiful 17-25 % FCF yield. I believe this multiple is far too low given its market power, low-cost base, sticky habit and the fact that I don’t think gross profits will fall in the medium to long run. For instance, Card Factory has generated the highest revenues and gross profits in its history this FY, with a 10% increase in revenue over the previous year. To top it all off, buying low-price greeting cards is a recession-proof purchase and current earnings power is not a result of cyclicality.

Why does the opportunity exist?

First, if you only mention the word greeting card to Wall Street, they will immediately assume it is a business model of the past and that the stock is cheap for a reason. To be honest, I used to think the very same thing because we don’t have this type of greeting card culture in Croatia. Foreigners underestimate the power of culture and are irrational about the industry volume declines, which are only falling 1-2% per year. And that’s including COVID, while competition and their shelf space are declining even quicker.

Simply put, the industry decline is harming competitors considerably more while allowing CARD to take market share in an industry with tighter supply.

Example of two sides…

…of the same coin

Second, the company was operated by a different management team before COVID, who ran it as a public LBO and paid out 100%+ of net profits as dividends. This approach worked well until the pandemic shut-down hit and CARD nearly went bankrupt. CEO Darcy Willson-Rymer and the new management team took control, squeezed the suppliers to prevent a highly dilutive equity raise, and turned the situation around. Nonetheless, since before the pandemic, shareholders have not seen any capital returned, which is why they may no longer want to own CARD. Now the company has met its leverage target (lowest leverage levels in a decade btw) allowing it to pay dividends (or even do buybacks) in the future.

The third concern for investors is the online competition. They do have a disadvantage there compared to their main competitor, Moonpig. However, online shopping caters to a different type of customer. Customers who are too lazy to walk to the store, who don’t mind if postage costs more than the card itself, and who want to find a “perfect” greeting card online ahead of time. On the other hand, retail shoppers frequently shop last minute, while touching and comparing cards to one another. Moreover, it appears that the only reason why Moonpig has made their economics work is that they packaged cards and gifts together.

To combat online pressures, Card Factory has implemented a click-and-collect strategy and leveraged its 1000-store retail footprint with a new ERP and data systems. However, this strategy has yet to fully prove itself.

That’s it. I believe my investment in $CARD.L will result in a 20%+ CAGR for my money. Is this what they call paper profits?

Thank you for reading!

PS

disc: ~8% position

This is NOT investment advice. All content on this website is for informational and educational purposes only and should not be considered to be advice of any nature. Due your own due diligence.

Hi David, just curious as to how you’re getting to the 17-25% FCF yield? I know they had some one-off lease repayments which are due to fall away, but even after adjusting for those i don’t get to 17-25%. Cheers, Fred

Hi, first of all, thanks for the article! :-)

In reading the following two statements...

"Their advantage stems from vertical integration, which means they design and print around 80% of their cards in-house, whereas their competitors are primarily supplied mostly by two suppliers, Hallmark and American Greetings"

and

"Furthermore, its inventory is financed by its suppliers resulting in a negative working capital cycle."

... I'm not sure how to add them up correctly.

If they make 80% of their inventory - the cards - in-house, how is their inventory financed by their suppliers?