Chaos Is A Ladder

turning risk into reward with $CRMZ

After reading my most recent piece, you've probably noticed that I’m fascinated by credit bureau business models. It's one of the few models for which I'd be willing to pay a market or even an above-market FCF multiple. So, when one of this blog’s readers shared a micro-cap company with a business model that is quite similar to CBA ($TCU.SI), I immediately took a closer look.

The model is very comparable to CBA’s non-FI data segment but of lower quality. However, I find the operators more trustworthy, the valuation much cheaper, and the risk-reward as asymmetric.

Introducing CreditRiskMonitor.com, ticker $CRMZ.

In the previous write-up, I mentioned that CBA operates a JV with Dun&Bradstreet, which collects its extensive data and later sells it to Singapore customers. CRMZ, on the other hand, is D&B’s competitor rather than a partner.

If you’ve worked in a large multinational corporation or studied D&B’s business model, you must know how tough it is to go around Dun & Bradstreet. The company has been collecting trade receivables data since 1841. It was the first company to persuade their customers, private companies, to give them their internal data on receivables (trade credit). Over time, D&B was able to build significant barriers to entry as a result of their longest record of transactions, their most extensive private company data coverage, and the complex infrastructure to handle it. Many companies tried to compete with it but failed, and D&B now holds above 80% market share, and its PAYDEX credit score has become almost as much of a standard for large corporations as FICO is to lenders in the US. Or, as the current Chairman of CRMZ, Jerry Flum, likes to put it: „no one ever gets fired for using D&B. “

So you must be wondering how CRMZ, a 19M in revenue micro-cap business, can compete with D&B, a nearly 200-year-old behemoth with more than 2B in revenue.

The obvious answer is that they can't. But what they can do is coexist, as they have consistently demonstrated since the company's inception in 1999. According to management, they currently share between 80-90% of their subscriber base with D&B.

Here's how CRMZ fits into the puzzle:

For starters, it's worth noting that both CRMZ and D&B solve the same problem for their customers, which is assessing the creditworthiness of your customers or suppliers and assuring that a counterparty will be able to pay their debts back to you on time. Commercial credit bureaus solving this huge problem was a big deal to society since credit is used in most B2B transactions. And trade credit accounts for around a quarter of total corporate debt and is approximately 3x the size of total bank loans.

Here's an example of a typical transaction from CRMZ's annual report:

As mentioned, D&B’s access and advantage of data on private companies is impossible to replicate; however, CRMZ has found an angle to take a piece of the pie and started analyzing trade credit and working capital of public companies. It has since grown its coverage from about 300 to more than 30 million businesses worldwide.

As most of you are aware, private companies in the US are not required by law to publicly disclose their financials, unlike most European countries. That makes D&B’s service so valuable, and their key advantage is the breadth of coverage of private businesses. On the other hand, CRMZ’s main advantage comes from accuracy. They prioritize accuracy above coverage of as many companies as possible.

The best illustration of accuracy is their FRISK score, which is a CRMZ-patented model that can predict bankruptcy risk of a public company with 96% accuracy. The score incorporates numerous external inputs, such as the Merton model, Altman Z score, and credit agency ratings, as well as one internal input. This internal input was introduced in 2013, and is calculated by using the daily sentiment of CRMZ’s clients. Or simply put, CRMZ monitors its clients’ behavior patterns on its website, such as what industries they click on and what companies they monitor, for how long, and how those change over time, in order to determine what companies might be at risk. This crowdsourcing analytical component is one of a kind in the industry and was trained exclusively on CRMZ’s proprietary data, which makes it a highly valuable intangible asset.

They also focus on big transactions. Because public companies are typically many times larger than private ones, more than half of the “money at risk” their subscribers face comes from the trade credit provided to public customers.

Just think about it, let’s say you’re selling your own local bottled beer. You supply it to both mom-and-pop tobacco shops but also sell it to large retail chains, and they pay you later, when the beer is sold. So, if a single or a few mom-and-pops suddenly go bust and fail to repay their debts, you can still survive and thrive. However, if a large grocery chain like Walmart fails to pay timely what they owe you, you run the risk of not getting paid big bucks or going out of business. Over night.

Another thing CRMZ does differently than D&B is offering good customer service and a low price. Because D&B had been so dominant for so long, they obviously started abusing their monopolistic position and overcharging while providing subpar customer service. So, to compete more effectively, CRMZ assigns a dedicated customer service rep to each of their clients, as well as charges a lower fee for their subscriptions. Obviously, D&B doesn’t care enough about a small company that accounts for only around 1% of the entire market to lower/match their pricing. And they also charge per use, per each report/score they sell, whereas CRMZ gives unrestricted access to their subscribers for almost all features.

For example, from the perspective of a corporate credit risk analyst/procurement specialist who is working for a large corporation, I think this is what decision-making looks like when considering a new client:

You subscribe to both D&B and CRMZ. You use CRMZ as an initial low-cost filter. You figure out how financially sound your potential counterparty is. If you find them financially strong, you can purchase a more expensive, comprehensive, and widely respected report from D&B.

Therefore, CRMZ is not directly competing with D&B but rather adding to the due-diligence process while lowering the costs for customers shared by both of you. By using CRMZ, they avoid spending money evaluating prospects that aren’t worth evaluating and can save time by quickly crossing prospects off the list.

Nonetheless, I do think that the ambition in the long term is being able to compete with D&B on private company coverage as well.

For example, over time CRMZ has been able to convince hundreds of their subscribers to share with them their internal trade receivables data, and they now collect more than $3 trillion worth of transaction data each year. Although this is nowhere near D&B, which collects roughly 10x that much, it is more than a decent start. CRMZ trained this trade receivables data, allowing it to develop another proprietary score, this time for predicting bankruptcy risk of private companies. PAYCE score still needs work because it is “only” 80% accurate, but it already covers more than 300K private enterprises or more than 90% of NA companies with >5M in revenue.

With D&B section out of the way, it’s time to further explain the attractiveness of the business model and show how it has evolved over the years.

The five pillars

CRMZ was built by Jerry Flum, a former hedge fund manager who spent the late twentieth century investing in small businesses. Due to the illiquid nature of these micro-cap stocks, preventing him from entering or exiting his positions fast, there was one variable he valued above others. Durability.

In 1999, Jerry returned money to his LPs and began running CRMZ, which he saw as the ideal example of a company where he would be comfortable putting his money long-term. He essentially built CRMZ on the core pillars of the investing strategy he was previously pursuing.

He considers durability as a key to success in micro-cap investing and these five pillars as a key to achieving that durability. I’ll try to profile CRMZ through the lens of these 5 pillars.

Recurring Streams of Income

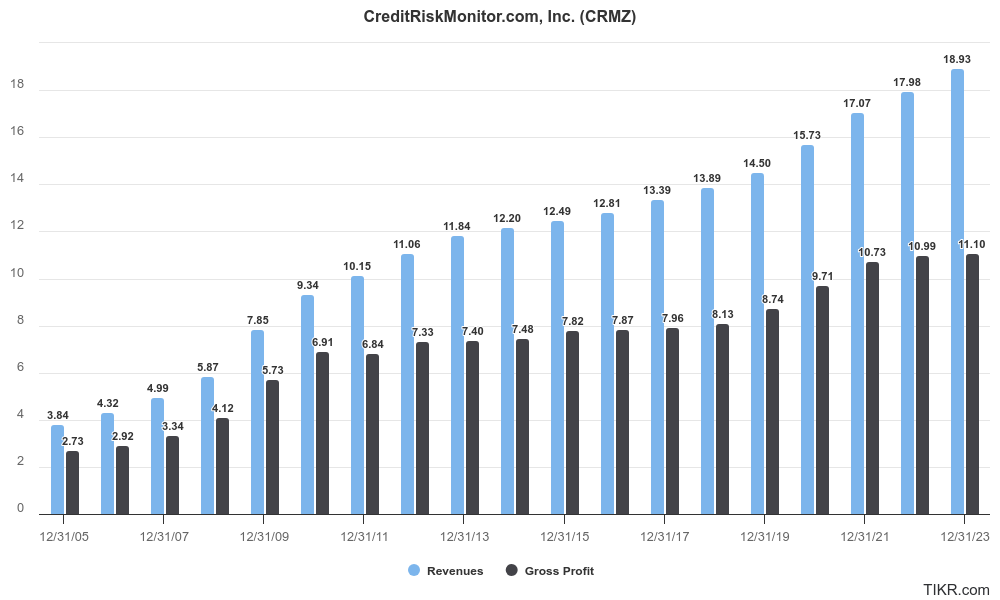

CRMZ generates 99% of its revenue from annual subscriptions that are paid at the beginning of the term. They service nearly 40% of Fortune 1000 companies, with retention rates above 90% and no single customer accounting for more than 1% of revenue. This makes the business model very predictable and working capital negative (which is positive, of course). Steady and consistent growth of the business can be clearly noticed while looking at a long-term chart of revenue and gross profit growth.

In the last 20-year period, the business has organically compounded sales at an 8.3% CAGR and gross profits at a 7.3%. Without a single YoY decline in revenue and only a single decline in gross profits, which happened in 2011, declining 1% YoY. Find me a business that can do that.

CRMZ was able to achieve this growth through prepaid annual subscriptions rather than having to retain earnings to grow. Meaning, as was the case with CBA, this business doesn’t have to employ any incremental capital to achieve growth, making its economics incredibly attractive. The asset-light nature can be noticed by looking at invested capital or equity adjusted for cash. Both negative.

While attractive economics can be observed by calculating how much FCF or even gross profits CRMZ can generate from its asset base (adjusted for cash, of course).

A true SaaS.

Countercyclicality is the second pillar, and another factor contributing to CRMZ's stability and durability

CRMZ thrives in recessionary environments because the “risk department” and role of credit analysts become more vital to the organization and its role more complex during downturns. When cash is tight, bankruptcies are high, new bank loans are nonexistent, and reacting to counterparty risks needs to be done faster and more accurately than usual, a lot more companies sign up for CRMZ solutions. Handling and monitoring credit risk efficiently becomes the primary concern for most businesses, resulting in more demand from CRMZ’s existing clients spending more on product add-ons or adding extra seats to their subscription. Another feature making the service relatively more appealing is the previously mentioned cheaper pricing compared to D&B; therefore, CRMZ gains a greater share of the wallet during downturns.

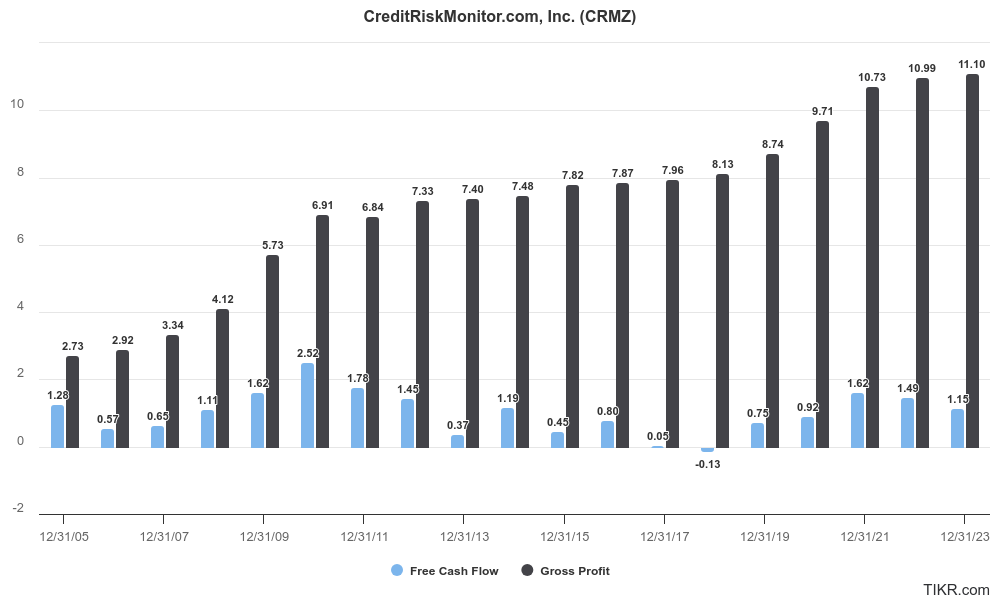

This countercyclical aspect is most noticeable during GFC or during COVID years. In GFC, when bankruptcies were sky high, CRMZ revenue growth accelerated to more than 30%, and operating leverage took care of the FCF generation.

For example, CRMZ’s revenues nearly doubled in the 3-year period from 2007 to 2011, while FCF went from 650K to 2.5M. (I know you have some further questions now; I’ll address them later.) Moreover, throughout the last 20 years the business has only had one year of negative FCF, demonstrating its ability to operate in any environment.

Jerry believe the third pillar of durability is an…

Overly strong balance sheet.

At the time I’m writing this, CRMZ carries ~16M in cash and treasuries on the balance sheet, only 1.7M in lease liabilities, and 0 dollars of debt. That represents a net cash position covering about 60% of the current market cap. And to make matters better (or worse), due to the prepaid subscription nature of the business, 11.4 million of the 15.6 million in total liabilities as of Q2 2024 are deferred revenue. I don’t want to get into theoretical debates about this, but I think all accountants will agree with me if I say this is the “best liability to have” for a growing company. And most of them would probably not consider it a “real” liability for this business.

The main component of current liabilities at June 30, 2024 was unexpired subscription revenue of approximately $11.4 million, which should not require significant future cash outlay, as this is annual reoccurring revenue, other than the cost of preparation and delivery of the applicable commercial credit reports, which cost much less than the unexpired subscription revenue shown. Unexpired subscription revenue is recognized as income over the subscription term, which approximates 12 months. ~Q2 2024 quarterly report

It's safe to assume that Jerry doesn’t like debt and prefers to finance growth internally. However, I find this strategy a step too far and one of the main “risks” to the thesis, but more on that later.

A Big TAM

The fourth pillar is a big TAM, which is self-explanatory given the above mentioned facts around CRMZ’s Fortune 1000 client base, around the size of D&B and around CRMZ’s only 1% market share.

The fifth and final pillar is…

Honest Skin-In-The-Game Management

Skin in the game aspect becomes obvious once you learn that the Flum family is a controlling owner and insiders own 58.6% of the company, and most of the senior leadership team has been with the company for more than a decade.

The “honesty” aspect becomes apparent once you listen to their interviews or read their MD&A sections over the years. The clearest example of this that I can provide is that while building their new product, saving data, doing R&D, or maintaining their existing infrastructure, no software development costs were capitalized. All salaries, expensed straight through the P&L. As a result, the data on more than 60K public companies and more than 300K private ones, which I consider their most valuable assets, is not shown on the balance sheet. I can’t recall the last time I analyzed a micro-cap that’s expensing everything and is optimized for FCF rather than EPS or net income margins.

"There is no line item on our balance sheet to reflect the value of our collecting and processing approximately $2 TRILLION of trade receivable data on an annualized basis on both public and private companies which allows us to extend our company coverage and maintain our commitment of having the most accurate risk scores available. Over 35% of the Fortune 1000 and over 1,000 other large companies worldwide depend on CreditRiskMonitor's timely news alerts and reports featuring detailed analyses of financial statements, ratio analysis and trend reports, bond rating agencies, crowd sourcing in real-time of thousands of risk professionals as well as our proprietary FRISK and PAYCE scores." ~ Jerry Flum

I think I have given information about the business for you to judge whether or not you like it, but let me now explain why I find this setup interesting.

Passing down the torch

Jerry’s son Michael joined the company in 2018. Since then, he’s held various positions at the company, and in May 2022, he took over the CEO throne from his father. Although I appreciate how honest and long-term-thinking Jerry is and how durable the business was able to build, I think the business will be better managed under Michael.

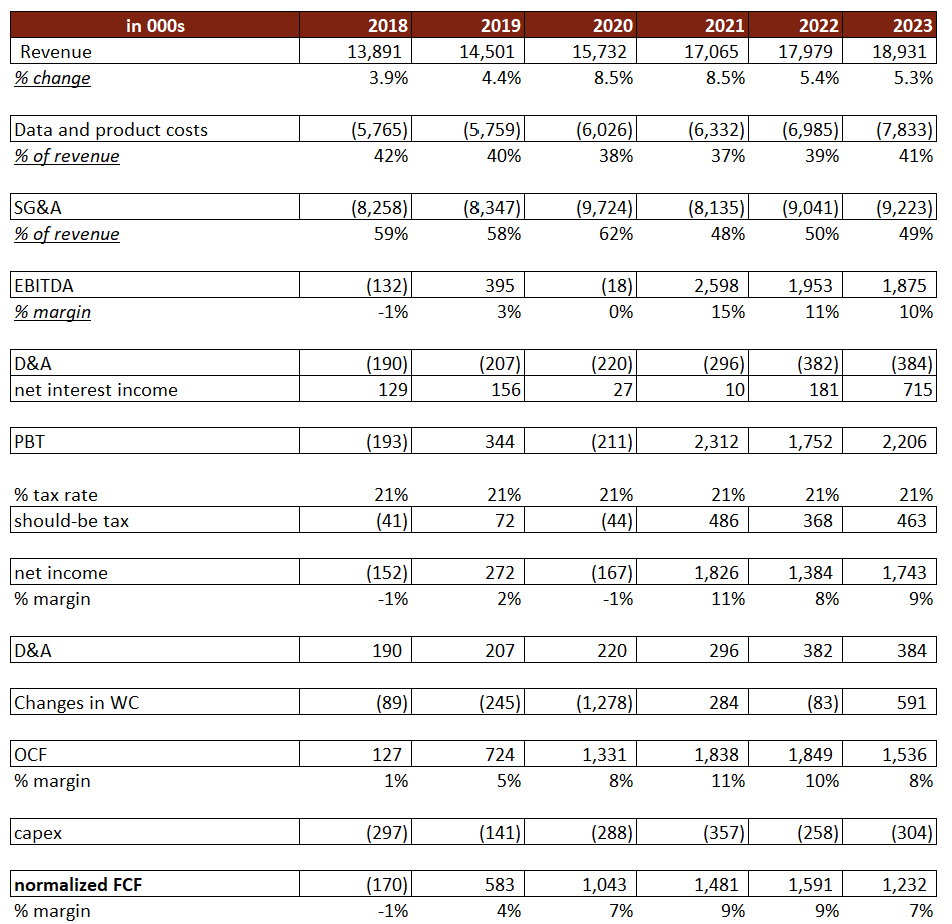

Although the business quality can be clearly noticed in the consistent gross profit growth over the last 20 years, unfortunately that GP growth hasn’t translated into consistent FCF growth, the most critical factor for creating value for shareholders.

While gross profits have 4x-ed in the last 20 years, FCF has moved nowhere. And while one would expect FCF margins of a growing float SaaS business would expand with scale, this was not the case. This bloated cost structure becomes evident once you compare CRMZ to CBA. In FY2023, CBA’s total wage expense was 23% of total revenue, whereas CRMZ spent 49% of total revenue only on SG&A expenses, which I presume, are mostly salaries and some marketing expense. That seems unreasonably high given the subscription model with churn below 10%. I can’t help but wonder how many new customers would still sign up and how many existing ones would re-subscribe if CRMZ completely discontinued cold-calling efforts and/or cut marketing spend.

IMO the main reason preventing operating leverage from occurring is that the company relied too much on people and not enough on technology. As stated earlier, each CRMZ subscriber gets a personal account manager who is ready to address any questions they have, within hours. This is a heavy load to bear for CRMZ’s cost structure. In my non-expert opinion, a close relationship with customers does make sense. However, I think both low(er) prices and high “maintenance costs” of their customer base don’t make much sense together. I’d rather see them increase pricing and keep delivering the same “best-in-breed” kind of customer service or keep the prices while investing in technology and making it as simple as possible to use it. So you don’t have to hire as many customer service reps per x number of customers, and your business model becomes more scalable.

The latter solution is where I believe Michael fits in well. He’s got an engineering background and is highly involved in software development, and the UI/UX of the company has steadily improved since he joined the company. Furthermore, he has stated multiple times that he wants to minimize further staffing costs and instead make technology perform more interventions and solve more problems.

For example, one of his responsibilities was to further increase the capacity of their infrastructure. During GFC, the finest environment CRMZ has ever experienced, the company was unable to meet all the additional demand and was forced to staff heavily.

Overall, I think that passing down the torch from an 80-year-old former hedge fund manager to a 37-year-old engineer should be a step in the right direction and will make the company less conservative, more tech savvy and faster to execute. Without losing access to Jerry’s valuable long-term strategic counsel.

Also, Michael, as CEO, is not the highest-paid person in the company and has stated he’d rather have more equity than take a higher salary.

Another step in the right direction is the creation of a new product called...

SupplyChainMonitor

After three years of development, SCM was released in May 2022. SCM software solves a similar kind of problem but for a different department within an organization. Instead of serving small credit risk departments, they began selling to large purchasing departments. Instead of addressing the concern of “will the buyer of my products pay me (on time),” they are solving the problem of “how can I avoid and monitor disruptions in my supply chain” and “should I do business with this supplier.”

SCM offers more customizable reports that show granular data. Assume you’re an US company that now believes US-China political risk is far more probable than previously. By using SCM, you can find another similar supplier in Mexico who meets your requirements. SCM also provides a holistic breakdown of the supply chain by geography, industry, currency, etc.

SCM already accounts for around 20% of CRMZ’s total revenue, as companies (finally) grasped the need to diversify their supply-chains away from a few cheap communist Asian suppliers on which they relied previously. And that the trendy JIT system cannot function as effectively in a multipolar world fraught with geopolitical risk.

From the perspective of a purchase specialist or a procurement analyst assessing new potential suppliers, the key value proposition is the cost savings. Instead of sending workers overseas to evaluate all factories or manufacturers, you can avoid wasting resources on bunch of shitcos. When onboarding a supplier, the main objective is to analyze their financial health. SCM helps by filtering only reliable suppliers with competitive facilities that meet customer needs. Only after that you begin conducting further due diligence, costing you a lot of money, but well worth the price.

This product has the potential to grow faster than CRMZ’s flagship product during economic expansion because it is billed per 20 users rather than per seat, and it is experiencing significant tailwinds from nearshoring, de-globalization, and the need to find alternatives to Chinese suppliers and lengthen supply chains.

Here’s what I think the new CEO and this new product mean for the risk-reward.

Inflection?

There are a few reasons why I think margins should expand and FCF should accelerate in the medium term. Firstly, throughout the pandemic years, CRMZ was burdened with high SCM development costs that have yet to be fully reflected in the financials. SaaS companies, such as CRMZ, typically have a long sales cycle, and salespeople earn significantly higher commissions for signing up a new customer than they do for the same customer renewing a subscription in year 3 or 4.

Additionally, these already mentioned software development costs were particularly high while launching SCM. It was their first API based software, after all, so the corresponding infrastructure to handle it needed to be built. Now everything is in place, it’s considerably cheaper to launch new products and enter new markets quickly. In the future, they plan to launch a Sales&Marketing product comparable to D&B’s, which you can read about in my previous blog. Again, this API infrastructure was expensed through P&L, which had an impact on historical margins but won’t in the future.

Further SCM growth while leveraging technology and better controlling personnel costs should also enable CRMZ to achieve better margins than historically. Additionally, it would make sense for COGS to decrease as % of revenue in the long term due to hardware, software, and telecommunications deflation.

I think a reasonable way to think about the medium-term profitability is 60-65% gross margins, and no more than 45% in SG&A expenses. Meaning that if CRMZ achieved these kinds of margins today, with the help of deferred revenue, this would translate into a 10-15% FCF margin or 2-3M in FCF on the current ARR base. When compared to their peer CBA, who reported 20% FCF margins last year and 44% PBT margins for their non-FI segment, this range doesn’t seem unreasonable. However, I think FCF generation will be closer to 1.5M and that margins will remain below 10% in the next year or so. As product, marketing and staff investments continue and the percentage interest earned on their cash pile decreases.

“The Company intends to continue to increase the size of its sales force and service staff as well as invest in product development, operating infrastructure, marketing and promotion. The Company believes that these expenditures will help it to sustain the revenue growth it has experienced over the last several years”

-“We anticipate that sales and marketing expenses will continue to increase in dollar amount and as a percentage of revenues into 2025 and future periods as the Company continues to expand its business on a worldwide basis. Further, the Company expects that product development expenses will also continue to increase in dollar amount and may increase as a percentage of revenues into 2025 and future periods because it expects to employ more development personnel on average compared to prior periods and build the infrastructure required to support the development of new and improved products and services.”

Nonetheless, once margins "stabilize," 3.5-5x normalized EV/FCF is extremely cheap for a company that has steadily compounded revenue at a >8% CAGR for 20 years.

Because FCF has been so lumpy over the years, I looked at one other metric here, EV/GP, which is much more consistent and demonstrates CRMZ’s profitability potential. (don’t kill me)

The current EV/GP is 0.9x

Before 2024, there were only three times CRMZ’s history when its valuation fell below 1X EV/GP and in each occasion shareholders profited handsomely in the subsequent 3-year period.

23/12/2008, the valuation bottomed at 0.86X EV/GP, and CRMZ stock was exactly 254% higher three years later, on 23/12/2021.

11 years later, on 12/6/2019, valuation went below 1x again and bottomed out at 0.98x EV/GP. The stock returned 80% to investors in the following 3-year period.

30/12/2021, the valuation bottomed out at 0.95x EV/GP, and shareholders that have been holding since are sitting on a 33% return. So, let’s hope there’s a Santa rally this December so this becomes a rule wink wink.

On May 28th of this year, the valuation reached its lowest level yet, or 0.74x EV/GP, and we have yet to see how the stock is going to treat spring 2024 shareholders.

(PS: none of these returns include dividends)

The business is good, the management is honest and the stock is cheap. But this setup, like any other, is not without its risks.

What can go wrong?

CRMZ, like all small companies, has a slew of little idiosyncratic issues that can never be avoided when stock picking.

We won’t focus on these. We’ll concentrate on the ones that could potentially jeopardize the risk-reward at this valuation.

The first and most obvious one is the unnecessarily large net cash-pile. It accounts for almost 60% of the current market cap and 75% of LTM revenue. As my friend

likes to say, this is something that belongs in Japan. If I saw this kind of cash pile mixed with family control, I would typically pass on the investment. However, after hearing the interviews, I kind of understand Jerry’s and Michael’s rationale for it. The first main reason behind it is that the cash on the balance sheet ensures Michael's smooth transition, preventing him from being forced into rash decisions, like cutting employees, due to cash shortages. This one makes sense to me as it lowers execution risk, especially with the new product out.However, they lost me on the second reason. Stating that they anticipate a severe downturn in the coming years and see potential opportunities for acquisitions or partnerships. And that they prefer to be overcapitalized in order to take advantage of these opportunities.

For starters, they had plenty of opportunities to do so during COVID, and secondly, there’s no way that they’ll be able to employ capital in a better way than buying back their stock at the current valuation. Or doing a large tender because the stock is too illiquid. You won’t find the SaaS model at 0.9x EV/GP anywhere else, no matter the downturn. Another reason why this decision doesn’t make sense is because the CRMZ is an incredibly stable business and performs better when conditions for other businesses are tough. So if you, as a CRMZ manager, foresee a recession, you shouldn’t be hoarding cash, because you know your business is going to perform best and throw off more cash in a downturn.

My conclusion is that the cash should be discounted, but not fully. After all, CRMZ has a history of paying out large dividends before they started focusing on SCM in 2019. They paid more than 6M in divvys during a 10-year period before SCM and recently authorized, but not exercised, a 1M buyback plan. I don’t believe the Flum family is “here to get us” or that the cash will be fully locked up on the balance sheet in the future. I anticipate a less conservative balance sheet and a dividend reinstatement in the medium term, when Michael gains more confidence at the helm of the business or if he cannot find a better way to reinvest the cash. Also, the Flums appreciate shareholders who are here for the long term, who won’t question them on quarterly lines of P&L.

In the worst-case scenario, if you discount all of the cash, you’d be paying 1.2x P/ARR multiple, which is hard to argue is expensive for CRMZ.

The second main risk stems from execution. As discussed above, CRMZ is not a stalwart with already established efficient processes but is still testing what works and what doesn’t. This means that if you’re thinking about investing in CRMZ for the long term, you should be comfortable with Michael testing new processes, exploring new verticals, building new products, signing new partnerships, and reinvesting FCF for you. At the time of writing, I am comfortable with him and would be surprised if he doesn’t generate adequate returns on reinvestment or create significant shareholder value in the future.

After all, with scale, there’s clearly room for improvement in their organizational processes.

The third risk, which may or may not be worth highlighting, is AI. I have no way of judging how advanced their data handling capabilities are, but perhaps a new entrant could be able to analyze the data as well as CRMZ currently does. Idk

I don’t worry about it much since they’re taking steps in the right direction by collecting subscribers’ trade receivables data and providing unique insights with proprietary FRISK and PAYCE scores. Also, 25 years’ worth of data and relationships at a low cost is not something that can be replicated that easily.

The final major risk that would stop CRMZ from being a great investment is that the SCM product doesn’t prove to be as durable or useful as their flagship product is. And if, at the same time, the world is heading back towards globalization or another prolonged ZIRP environment with too many shitcos not going bust. Such an environment would almost certainly reduce demand for CRMZ's product.

But let’s further discuss this risk, which may also function as an optionality to the thesis.

Antifragile

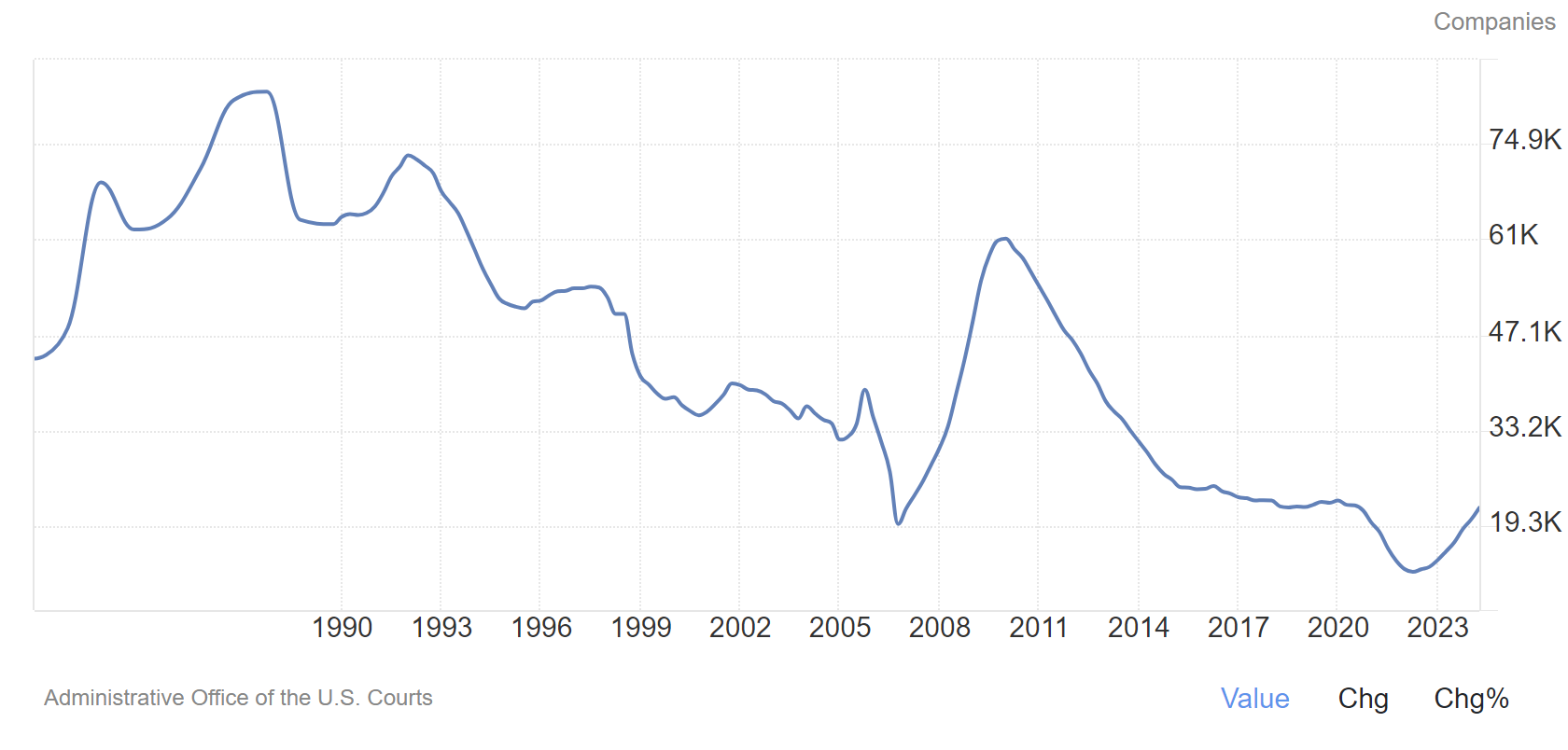

“Since the Great Recession, the world has been in an exceedingly easy credit regime supported by the central bank policies of very-low-to-zero interest rates and quantitative easing. These policies have made it exceedingly difficult for low-quality, non-profitable, businesses to go bankrupt since they’ve had consistent access to cheap, plentiful credit and can roll that financing over at each maturity. A fact reflected by the spectacular growth in the number of “zombie” companies, those that cannot effectively cover their interest expenses with their earnings, over this period.” ~Michael Flum @ CEOCFO magazine

As most of you are aware, investors couldn’t care less about debt or interest rate coverage from 2009 to early 2022. And as Jerry likes to remark, you don’t need a credit analyst to analyze if Walmart will be able to pay 2% interest on its debt. ZIRP made it impossible even for shitcos to go bankrupt.

Low interest rates have a clear positive impact on the number and value of bankruptcies.

With fewer companies going bankrupt, there’s a limited demand for CRMZ’s flagship product. And while I realize that you could probably make a case on why the next 15-years will be as structurally negative for CRMZ as the previous 15, I still believe CRMZ can serve as an attractive hedge against interest rates, recessions and volatility.

Let’s assume a recession as severe as the GFC is just around the corner. For CRMZ, this would mean instant 15-30% revenue growth and insane operating leverage. Doubling revenues from here would likely result in at least 25% FCF margins for the business, especially now, with tech infrastructure in place that wasn’t there before GFC. Or 10M in FCF compared to the current EV of 10M or a market cap of 24M.

I’m not saying this is a likely scenario, but if we were to trust economists who keep saying that due to constant central bank interventions, recessions have gotten less frequent and more intense, we can buy CRMZ under a 1X EV/FCF based on what FCF generation would look like during an intense recession. If the “doom and gloom” regarding the Western world’s debt crisis really comes to fruition (I hope not), this is a perfect hedge to have and is IMO probably worth a small bet, even if the thesis proves to be broken.

Why is the market offering me this opportunity?

One Tikr screenshot can give it away. There aren’t many eyes on this name. The ones who are interested but not as poor as your fellow Croat analyst could spend weeks or months accumulating a normal-sized position.

With development costs expensed through P&L and lots of deferred revenue, CRMZ screens badly, with an LTM P/E ratio of 20. (Btw use my Tikr link if you want)

Another reason why I might be one of the first investors to look into the name is that from the firm's inception in 1999 to the spring of 2023, CRMZ did not do any interviews, earnings calls, or speak with investors. It was hiding in plain sight until Michael took charge and they held their first roadshow in company’s history in April 2023, as well as a couple of interviews afterwards.

These interviews were great and helpful my diligence process and in understanding management’s motivation, but they didn’t receive much attention from the micro-cap community.

The final reason why investors may not be excited of this company is its significant relative underperformance over the last decade, while interest rates were low and SPY kept making high after high.

Although $CRMZ moved nowhere for 10 years, its 20-year track record looks to be much better. Owning CRMZ for the long term would provide shareholders with a better, albeit more volatile, ride than holding onto SPY, even before factoring in the dividends.

Now that I've covered everything I deem important, I’ll summarize why I believe $CRMZ is an asymmetric bet.

How I see the risk-reward

Worst-case scenario: ZIRP environment is back and remains in place for a long time in the future, the SCM product doesn’t bring any revenue acceleration, and the growth profile of the next ten years turns out to be as poor as the previous decade. Thus, revenue compounds at “only” 6.4%, the balance sheet remains overcapitalized, and no dividends are paid out to you. The future FCF margin remains at a 10-year median of 6%. And you’re paying a 1.2X P/ARR multiple, 1.3X tangible book adjusted for deferred revenue, 20X P/LTM FCF

Likely case: revenue growth accelerates as a result of SCM while tech initiatives optimize the cost structure, causing FCF margins to expand to 10-15% in the medium term. The majority of the cash on the balance sheet ends up in your pocket or reinvested. You’re paying 8.5x EV/LTM FCF, 7x EV/average FCF generated over the last 3 years, 9X EV/median FCF generated over the last 6 years, and 3.5-5x EV/FCF for CRMZ’s future cash-flowing ability, once growth picks up to the high-single digits or low-double digits. I’ll leave it up to you to decide how much you want to discount that cash-pile by and what metric you want to use.

Best-case scenario: the world and the stock market go to shit, but CRMZ’s profitability skyrockets. All the cash is given back to shareholders in one way or another, and you’re paying about 1x EV/recessionary FCF while holding an uncorrelated bet to the rest of the market.

This leads me to believe that the bet is mispriced which is why I allocated nearly 5% of portfolio to it. The risk-reward is favorable, and I feel comfortable with both the business and management.

That’s all from me today. If you’re still here, I want to thank you for reading the article. And if you wish to support this kind of work, consider becoming a free or paid subscriber.

The Mikro Kap uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks. Due your own due diligence.

Non pushback pushbacks: (1) The 40% Fortune 1000 number does not seem to have change for some time. (2) no one gets fired for hiring D&B which means there needs to be justification for using CRMZ which you already discussed. Given the quality of the product “risk assessment” is something hard to evaluate, it puts downward pressure on pricing I would think. (3) other bigger companies had tried to break into the space before without success and there is competition in the new supply chain business, (4) cash reserve - I agree with Jerry that’s needed to show customers the company itself is solid and I think for the company to grow it takes entrepreneur efforts in Mike’s part which needs cash financing. Overall I agree it’s a good company but yet to be proven IMO. Thanks!

epic. can't believe this substack is free.