Playing With Fire

$DGL.AX, Mikro Kap Watchlist #3

Hello,

Welcome to the third edition of the Mikro Kap Wathclist, a series in which I go deeper into unique opportunities from my watchlist that, IMO, are worth monitoring closely. This way, you can act decisively when the moment comes, rather than spending weeks on initial research.

These kinds of stocks would probably be a part of my portfolio if I were older, more diversified, or both.

After delving into the UK luxury interior furnishing industry in the first two editions, it’s time to move on to something very different: Australia’s chemicals and hazardous goods logistics. (I promise it’s more interesting than it sounds, but I understand if you want to stop reading).

Long-time readers may recall my video interview with Simon Henry, the founder-CEO, and Frank Izzo, the CFO. While I shared the interview, I didn't go into my takeaways—what piqued my interest and why I believe now is a good time to follow up on $DGL.AX

DGL Group

DGL Group, formerly known as Dangerous Goods Logistics, is a vertically integrated company that serves the (specialty) chemicals and hazardous goods industry in Australia and New Zealand.

Taking this vertically integrated "one-stop-shop" approach enabled DGL to attract major multinational chemical companies. This means that international manufacturers entering the Australian or NZ market often rely on DGL's formulations to launch their products. So if an international manufacturer wished to enter these two markets and introduce its products, they will most likely base their product development on the back of DGL’s formulations.

In addition to formulation, DGL offers a variety of other services to its customers. They do procurement of raw materials from Asia, leveraging its scale to secure lower input costs needed for chemical manufacturing. They also offer custom formulation packaging, licensed warehousing with specialized storage, and efficient nation-wide distribution. The final aspect of DGL's offering to customers is managing waste disposal or recycling it in conformity with Australian law.

DGL views itself as a unified platform rather than separate segments. However, here's a visual from their prospectus highlighting three key areas of their business to help illustrate the breadth of their offerings.

The first thing that comes to mind is why a company would outsource all of these activities to DGL rather than doing it themselves?

There are three reasons why. First and foremost, neither contract manufacturing nor logistics are regarded as a “core activity” in the eyes of their customers. Instead, DGL’s customers focus on innovation and development of various customized formulations for niche applications as well as marketing their complex technical features to end-users.

Second, and more importantly, contract manufacturing and distribution of chemicals is an extremely challenging business. It’s not only that it’s asset-heavy, requiring numerous plants, facilities, and trucks; it also involves strict regulations. Specialized licenses and accreditations are needed to produce, store, transport, and dispose of chemical products. In other words, expertise alone is not enough, you also need to comply with the regulation.

Just take a look at the list of licenses DGL has obtained over the years to in order to do business.

For anyone looking to operate in Australia, establishing what DGL does in-house would take significant amount of time and money. You’d have to comply with strict state-by-state regulations to transport chemicals across the whole territory, making it impossible to rely on a typical local distributor instead of DGL.

Moreover, it’s not like this regulation is getting any looser. On the contrary, on the recent AGM call, Simon explained how because of the new compliance and regulatory overview, new activities in the industry now take years rather than months.

As regulations tighten year after year and penalties for non-compliance grow, I like to describe DGL’s industry as:

“Show me the chemical, and I’ll show you the regulation.”

The eventual result is, of course, higher compliance costs for DGL but also increased barriers to entry as smaller players become frustrated and exit the industry. As a result, international chemical companies naturally seek to outsource as much of this work as possible to larger companies like DGL.

The third reason DGL has an advantage over its competitors is its unique position as the only one-stop-shop solution on the market. While other companies may specialize in areas like logistics, formulation, or water treatment, no one else offers all these services together, on a single platform. This makes DGL the obvious choice for supply chain managers who want to reduce suppliers, as it provides a complete solution with national coverage, servicing them differently in different states with all the necessary permits from multiple authorities.

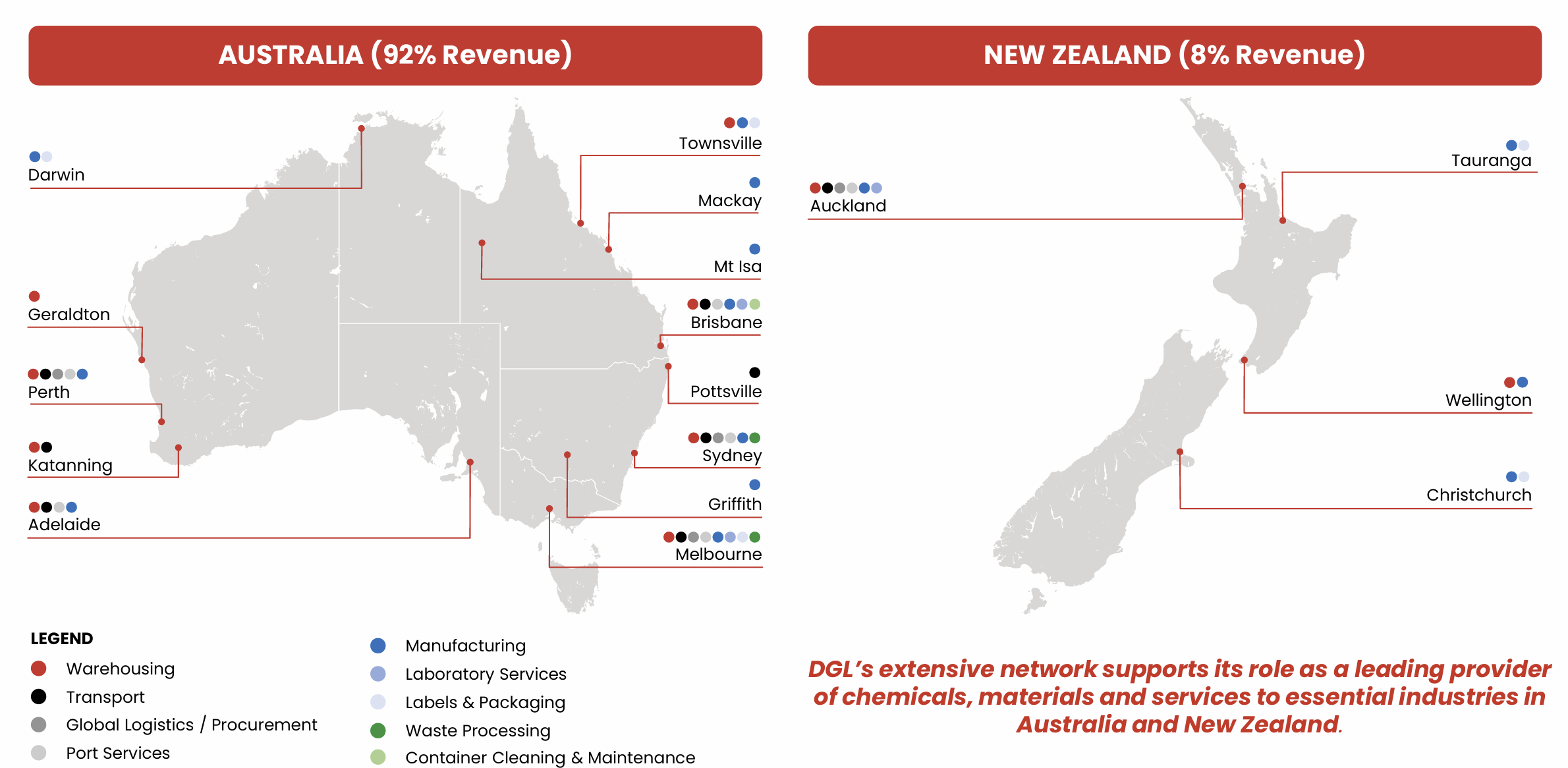

To be more precise, as of FY 2024, DGL serves over 5,000 customers, with 205,000 tonnes of chemical storage capacity and 85 strategically located sites across Australia and New Zealand.

Most of these licensed facilities, owned outright by DGL, are truly irreplaceable assets. For instance, one hazardous facility holds a license to store all of Auckland's chlorine gas.

Another highlight of DGL’s business model is its deep integration into customer processes. Like their in-house stock management system, which is tailored to customer needs, offering full or partial integration with customers’ supply chains.

Here are some more reasons, first highlighted in DGL’s prospectus, why customers are unlikely to switch:

Once you’re on DGL’s platform it’s tough to get out.

Additionally, despite selling somewhat commoditized products such as chemicals, DGL retains a decent amount of pricing power through its “order-driven” approach. Or simply said, rather than purchasing chemical inventory upfront and praying somebody will buy it, DGL waits for customer orders and therefore pass on costs effectively.

And when DGL is formulating specialty or performance chemicals for third parties, customers prioritize its capabilities and technical know-how over price. While the absence of transparent or comparable pricing in the sector further helps DGL to maintain healthy margins.

To conclude, DGL is an asset-heavy business with a unique platform for chemical distribution, benefiting from high barriers to entry thanks to strict regulation and high switching costs.

And while I consider DGL an above-average business, there’s always a catch—and no, it’s not valuation.

The cycle

The catch is that during the supply chain-related disruptions caused by COVID, DGL’s customers decided to overstock heavily. This resulted in DGL reporting above-normal profitability in FY 2021 and FY 2022.

And - as we all know - when you’re an asset-heavy business, operating leverage works both ways.

So in FY 2023 and 2024, when customers concluded that the “worst is behind them,” reduced their demand, and opted to normalize their inventory, DGL suffered greatly. The fact that DGL mostly serves cyclical and industrial sectors such as manufacturing, agriculture, automotive, mining, and infrastructure did not help matters.

Exacerbated by lower chemical prices, underlying EBIT margins plummeted from 12.8% in 2022 to 6.8% in the last fiscal year.

As a result, the same investors who were extrapolating above-average margins and rapid growth into the future, willing to pay over a 50x EV/EBIT multiple and more than 6x P/TB in 2022, are now expecting 0 growth and discounting DGL a 10x EV/EBIT multiple on depressed earnings and a 0.8x P/TB valuation.

Yes, you guessed it: the stock is down more than 85% from its 2022 highs of 4 AUD to 57 cents.

While one could argue that 10X EV/EBIT or 11x P/E multiple is not particularly cheap for a company distributing chemicals, I think this would be overlooking the bigger picture. Let me explain.

Organic growth

First, while cyclical, DGL is not your typical cyclical company that only grows during favorable cycles. On the contrary, the specialty chemicals distribution industry is young and benefiting from multiple tailwinds. In capitalist societies, both consumers and businesses have limitless demands, driving companies to offer more niche, complex products and services or adopt specialized ways of doing business.

Chemical companies therefore innovate to create new formulations used as inputs for complex products and/or business models, driving natural demand for DGL’s offering. For example, Australian farmers use DGL’s chemicals to improve crop yields, mining companies use DGL’s specialty chemicals to treat water discharged from mine sites, and building contractors use admixtures, specialty chemicals added to traditional concrete, to enhance performance and improve efficiency in infrastructure projects.

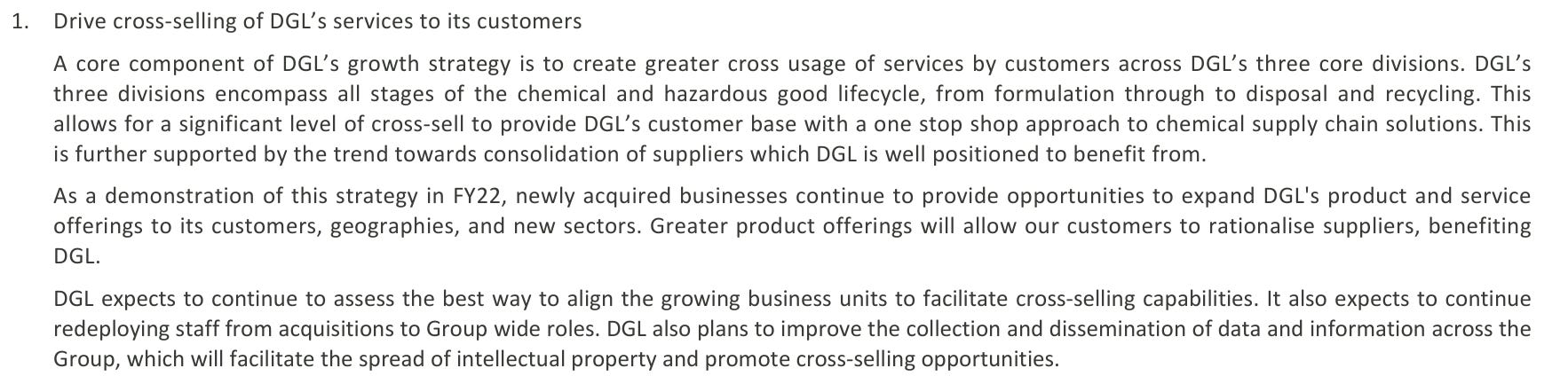

Additionally, serving large multinational companies provides DGL with numerous cross-selling opportunities, which management believes will be a key driver of organic growth moving forward.

This is why Simon often says, “we don’t have to look for work.”

Furthermore, the increasingly complex regulations have brought pain to smaller industry participants, leading to consolidation. Big companies, skilled at adapting to stricter compliance, get bigger, while smaller players get less competitive and fall behind.

This ability to cross-sell, combined with the natural need for industry consolidation, has prompted large chemical distributors to focus on one thing: acquisitions.

Inorganic growth

“People are leaving the industry out of frustration or due to a lack of capital to invest in their sites to make them compliant or, as often, the case across Australia and NZ, the founders are retiring and there’s no family to take them over and they’re looking for their businesses to be sold” ~ AGM 2024

Since its 2021 IPO, DGL has pursued an aggressive acquisition strategy, acquiring around 30 small(er) businesses.

During the 2021-2023 period, I considered this strategy risky, leading me to question whether Simon was more focused on "building an empire" rather than creating shareholder value. He boasted about not having an M&A team while acquiring 24 businesses in 24 months. While I don’t believe Simon is a bad capital allocator—quite the opposite—such rapid acquisitions usually work until they don’t (unless your name is Mark Leonard). Personally, I find it difficult to get comfortable with that kind of acquisition strategy.

Recently, however, Simon has slowed down, shifting focus more towards organic growth and becoming much more selective with acquisitions.

“In future years, our focus will be more on organic growth than growth through buying companies. We have agglomerated an extensive integrated train of assets stretching across Australia and New Zealand, over 90 plants, over 400 trucks. We are learning how to use these assets better, and having them work together more efficiently and gaining better utilization and return out of them”

He is now prioritizing only deals with high strategic importance for the wider Group. He’s not interested in “spending a dollar to make a dollar.” Instead, he seeks acquisitions with specific licenses, customer relationships, sales teams, or territorial coverage that can be integrated and expanded within DGL’s existing business, ensuring that the benefits of the acquisitions far outweigh the cost. He also likes to acquire where it would be more expensive to build organically.

The "roll-up" strategy appears to be heading in the right direction. The management team has gotten better at centralizing back-office functions from acquired companies and is placing a stronger focus on quick integration. Moreover, the broader the range of services DGL can offer, the more appealing their one-stop solution becomes to their customers.

And although DGL still doesn’t have a rigid hurdle rate for acquisitions, 2024 has indeed shown that Simon remains committed to not overpaying for acquisitions and prefers buying stuff “on the cheap”.

For instance, the last two “significant” acquisitions were made at 3.7x and 2.5x EBITDA multiple.

I prefer this more "muted" pace of bolt-on acquisitions in 2024, with only 5 companies acquired, over the high-risk, high-reward strategy pursued after the IPO.

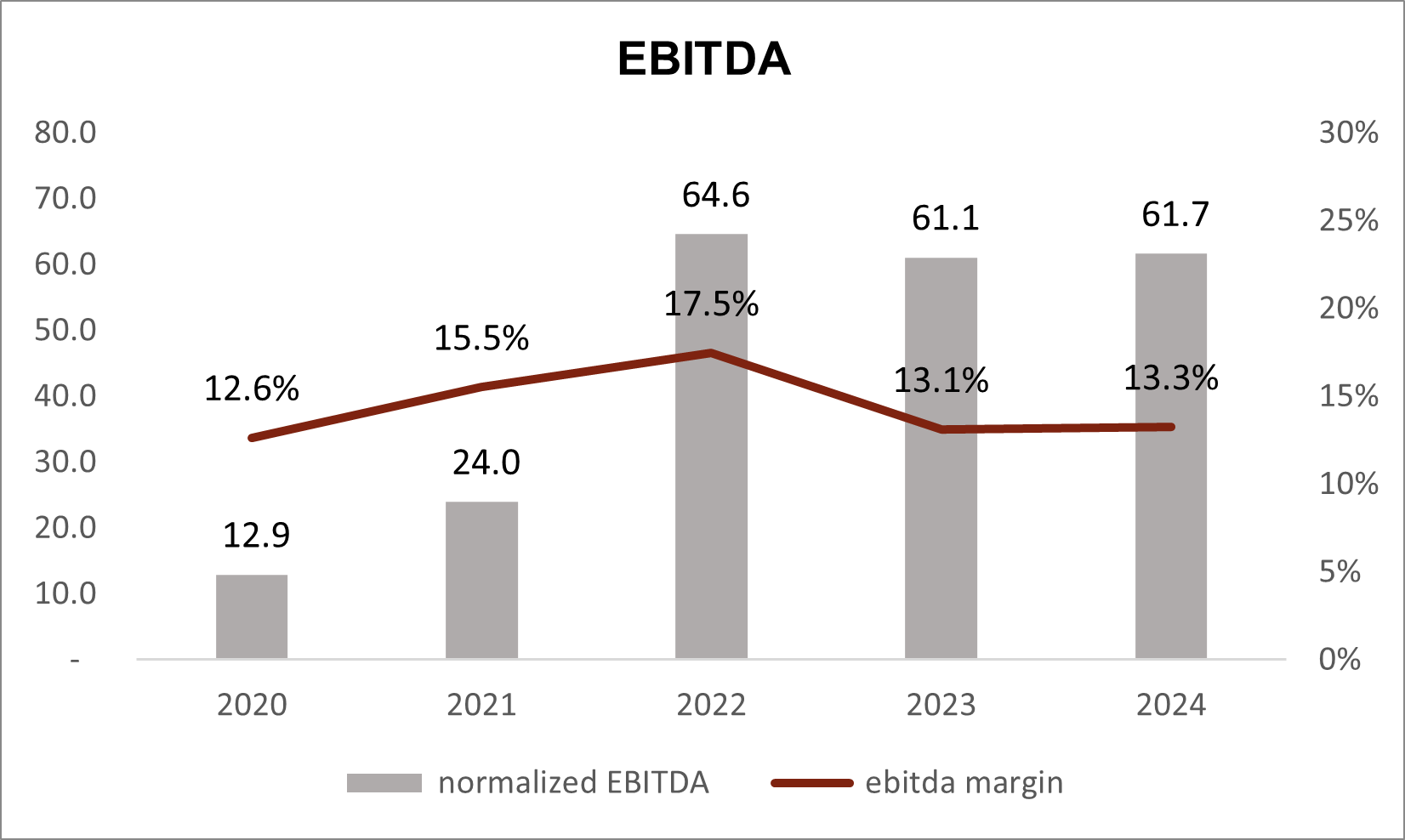

Continuing this inorganic growth strategy should lead to even faster growth in an industry already outpacing the growth of nominal GDP. So, it’s no surprise when Simon says (pun intended) DGL has grown 20% annually since its inception in 1999, or when you notice a revenue increase from 102M in 2020 to 465M in 2024, with normalized EBITDA rising from 12.9M in 2020 to 61.7M LTM.

“I predict that we're going to see some current competitors in the chemical logistics in Australia exiting the market. I talked about the significant expansion that we have carried out in the first half of some 40,000 square meters of space and hardstand and we are going to look to mop up business that's abandoned, you might say, by competitors, so strong growth there.” ~H1 2024

By now, you understand why I expect revenue and profitability to keep growing in the future, regardless of how ugly or not ugly the short-term might be. However, I have another reason to believe that a 10x EV/EBIT multiple appears more expensive than it should be.

Short-term vs Long-term

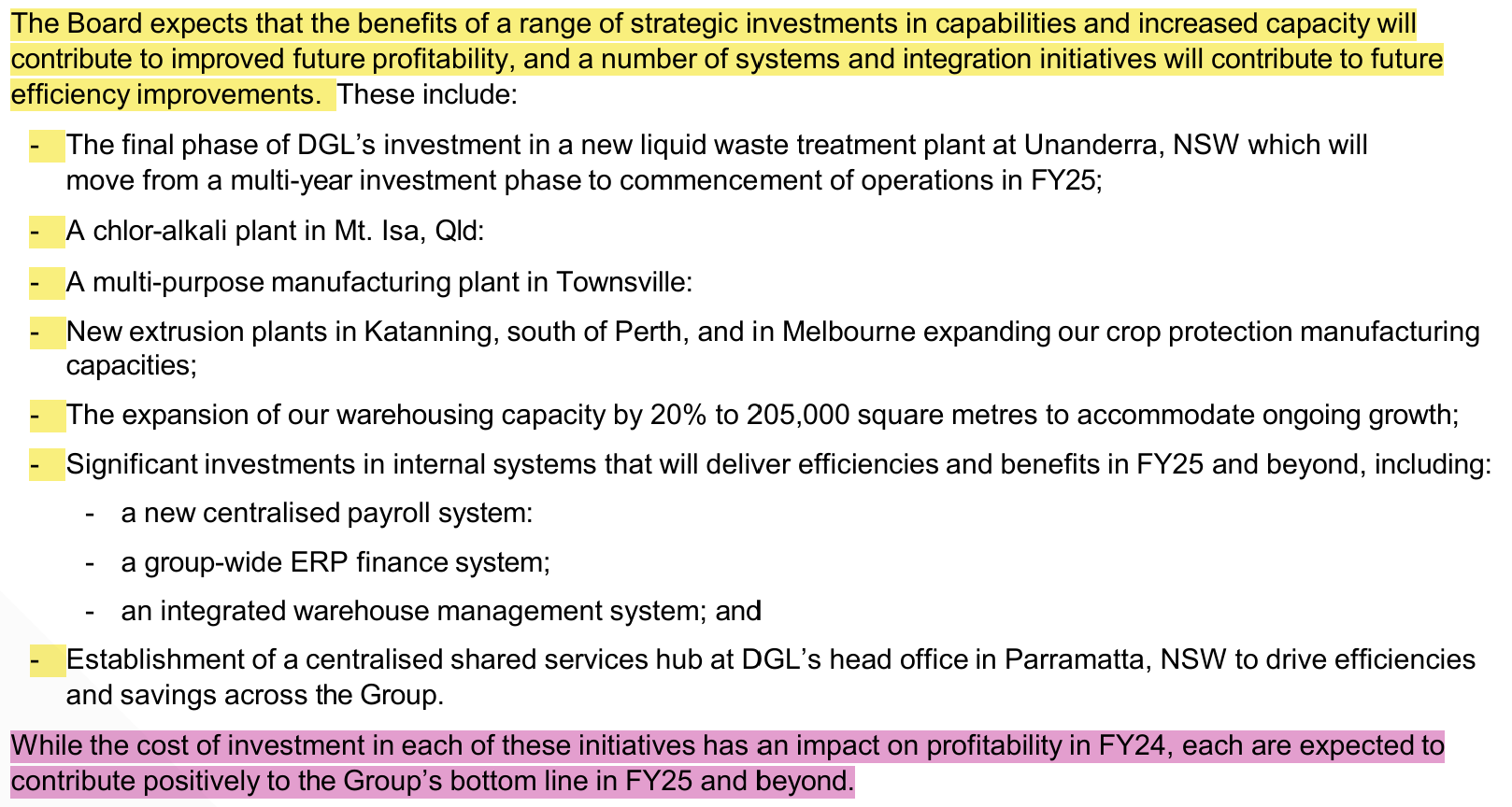

An interesting paragraph was added to this year’s annual report:

In addition to the unfavorable chemicals cycle affecting DGL, last year saw an unusually high growth capex spend. As noted in the 10-K, DGL expanded its warehousing capacity by 35,000 square meters and invested significantly in new waste-treatment, chlor-alkali, extrusion, and manufacturing plants. Additionally, to improve efficiencies from previously acquired businesses and better integrate future acquisitions, DGL also invested in a new centralized payroll system, group-wide ERP and warehouse management systems, as well as established a new head office in Sydney to centralize finance, HR, and legal support for the entire group.

Indeed, it has been "a year of investments."

Furthermore, 2024 marked the arrival of several new hires, including a new CFO, COO, financial controller, and company secretary.

Finally, the HOT labor market caused Australia’s unemployment rate to hit a record low, even dipping below 4% during certain months in DGL’s FY 2024.

As a result of the factors mentioned, despite volume growth, flat revenue year-over-year, and solid gross profit growth, DGL's normalized EBIT dropped 19%, and net income declined 36% in fiscal 2024 compared to the previous year.

If words fail to capture just how "unusual" 2024's cost structure truly is, the financials might do it.

Operating expenses grew by more than 25M YoY and are clearly "off trend" by a wide margin. What was previously an average SG&A margin of 21.1% has risen to 27.3% in 2024.

( I’ll leave it to you to calculate the impact on valuation if SG&A returns anywhere near its historical average. Hint: it’s a big difference)

Also, the significant upfront investments in transport fleet, warehousing, and manufacturing capacity are evident in the D&A impact. This is reflected in the disparity between the normalized EBIT margin contracting from 8.3% to 6.8%, even as the EBITDA margin slightly improved from 13.1% to 13.3%.

While I don’t believe all these costs are a “one-off,” it’s clear to me that LTM net and EBIT margins are significantly lower than they would be under normal operating conditions. While for investors who haven’t “dug deeper,” this creates the impression that DGL is more expensive on valuation screens than it actually is and gives the false perception of being more cyclical than it truly is.

With inventory returning to pre-COVID levels, recent organic and inorganic acquisitions bearing fruit, and most short-term investments now behind DGL, I anticipate higher earnings and improved net margins beginning in the second half of FY 2025.

“We are incurring heavier costs at the present time than they expect to in the next year or 2.” ~ AGM 2024

How much higher? I really don’t know. And don’t think anyone can say for sure.

However, there are some “writings on the wall” suggesting that management is quite confident last years’ earnings decline is just a short-term setback rather than a structural issue. This confidence is also why I chose to write about DGL now instead of earlier this year.

Simon says…DGL is a buy

First, at last month’s AGM, DGL introduced its first-ever employee incentive plan. Under the plan, all employees can purchase up to 10K worth of shares at a 10% discount to market value. More importantly, this plan also grants DGL's C-suite executives up to 50% of their base salary in shares, contingent on achieving EPS growth and share price performance targets.

To be more specific, these performance rights vest over a 3-year period, and for management to be “fully rewarded,” they must achieve an EPS CAGR of 15% over the next three years and deliver total shareholder returns ranking in the top 25% of all industrial companies in the ASX 300 index.

Second, during the same AGM call, there were some subtle hints about what the Board might think about DGL’s current valuation when it unusually stated that the "share price is not where we want it to be" and expressed their intention to reinstate the buyback.

Third, and most importantly, Simon Henry, the CEO, who already owns 53% of the business, has recently purchased significant amounts of shares on the open market. In late October, he bought 1.06 million shares at an average price of 60 cents per share. And just as I’m writing this piece, he has bought an additional 276K shares at an average price of 56 cents.

This is IMO a big sign of confidence, indicating that management expects high earnings growth in the medium term and/or believes the stock is undervalued.

That said, my only concerns about DGL’s setup at the current valuation are as follows:

Risks to the thesis

DGL operates across three segments, serving various industries. While this diversification reduces single-industry risks, it also makes the business too unpredictable to value accurately.

The lack of granular reporting on their customer base as well as cyclical industry exposure further hinders my ability to confidently say what normalized earnings really look like.

…I thought about breaking down the business by segments, but quickly realized it would result in myopia and do more harm than good due to the many uncorrelated components required to approximately estimate steady-state cash flows and, ultimately, rough intrinsic value.

For instance, DGL’s Lead Acid Battery operations have faced intense competition in 2024, affecting pricing, volumes, and profitability.

Some might argue that the numerous moving parts represent uncertainty rather than risk. However, with my concentrated portfolio approach, I prefer investing in businesses where I have a firm understanding of a few key KPIs that will make or break my thesis, rather than wrapping my head around numerous factors that are “all over the place.”

Secondly, the high turnover among senior team members makes me question whether there are any potential cultural issues that I’m not aware of from behind the computer. Additionally, since DGL isn't a "bureaucratic" organization, employees from acquired companies may take longer to adapt to its way of doing business.

If I managed a diversified portfolio with 20-25 positions at 4-5% each, I’d likely own DGL. For now, though, I prefer to monitor it closely from the sidelines and see how my confidence evolves.

IMO no one can predict exactly when the cycle will turn, so the market may still offer me a good opportunity to own this one in size. Even after considering the uncertainties surrounding specific divisions or industries.

That said, if I were to value DGL, I’d take the following approach:

Quick and dirty

Private market value

First, my friend

, who has been closely following the specialty chemicals industry far longer than I have and introduced me to DGL earlier this year, noted that major players like IMCD, Redox, and Brenntag often report that acquisitions of "platforms" like DGL typically occur at high single-digit to low double-digit EBITDA multiples.Which means that the "private market value" of DGL, in an industry known for its acquisition activity, is likely around double DGL’s current valuation of under 5x EV/EBITDA, providing investors with a large margin of safety.

Asset approach

Second, due to DGL’s asset-heavy nature, the P/TB approach is also applicable, with the current P/TB standing at 0.8x. And even if you decide to discount DGL’s asset revaluation reserve to zero, the price to tangible book multiple remains a modest 1.1x.

Recent transactions support its tangible book value, as Simon has been selling non-core assets (basic properties without licenses or accreditations) and reinvesting in more strategic ones. Since the IPO, 6 out of 7 properties were sold at a premium to book value. Moreover, as already mentioned, most of the remaining assets are truly unique.

“So primarily. It will be extracting full value out of our licenses and facilities that we have established already. There is room for organic growth from these assets. It’s really about us getting in front of our customers and offering them more services in the network of assets.” ~ AGM 2024 Simon talking about greatest opportunities for growth in the next 3-5 years

Likely earnings inflection in the medium-term

The third approach is simply applying some "common sense" to semi-cyclical companies.

Paying barely a 10x LTM EV/normalized EBIT multiple or 11x P/E for depressed earnings of a dominant company in a growing industry—while analysts focus on short-term cycle headwinds, cost pressures and next half’s earnings or fear that the “stock might continue to fall”—tends to work wonders for patient investors in the medium term.

That’s it. This is why I believe DGL is a worthy Mikro Kap Watchlist candidate. And an idea worth closely following or potentially buying.

Thanks for reading! And if you’d like to support this kind of work, consider becoming a free or paid subscriber.

The Mikro Kap uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. Consult your financial adviser to understand whether any investment is suitable for your specific needs.

I may, from time to time, have positions in the securities covered in the articles on this website and reserve the right to buy or sell any securities mentioned in this article at any time, without prior notice.

This is not a recommendation to buy or sell stocks. Do your own due diligence.

The pre-tax return on unlevered net tangible assets is below 10%. Do you think the return on incremental capital is better than this? If not, I'd struggle to see this as anything other than a multiple re-rating play with relatively mediocre upside.

Also, just looking at Yahoo finance, it looks like the share count more than quadrupled in FY22 - is this an error? Or if not why was this?

Thanks for the write-up. I might spend some time following and doing periodic DD.

The EBITDA margin looks slightly lower than some North American transportation companies. I assume that it would have to do with the chemical aspect compared to normal road freight.

Do you have any idea what their insurance claims look like in the event of any accidents? It seems like damage to reputation or accident claims could be a potential risk.