The Holy Trinity of Banking

betting on men of culture

This write-up is not something you would normally (or ever) expect from me.

It's about a bank. To be more specific, it is about a one-branch community bank out of Fort Worth, Texas.

Despite sounding unimpressive at first, probably enticing you to stop reading the article immediately, this bank has managed to outperform both the SPY and every other bank ETF that you can think of since going public in late 2003.

All despite currently selling at one of the lowest valuations in history.

Despite $TYBT stock’s impressive historical performance and seemingly reasonable valuation, I was still hesitant to dive deeper into it. After all, "I don't do banks."

Luckily, a friend of mine, who first introduced me to Trinity (the name of this bank), suggested that I at least read its CEO’s letters to shareholders, which he believes are the “best way to learn about banking.”

“Sure, I’ll do it.”

I must say that he couldn't be more right, and I devoured those letters.

I liked them so much that I decided to embark on a PDF merging spree so I could CTRL+F anything later.

You can download all publicly available letters here.

A man of culture

The genius behind the letters and the business is Mr. Jeff Harp.

Harp was let go from his post as President at Summit Bank in 2001 for being overly conservative. He chilled for about a year, waiting for his non-compete clause to expire, before deciding to start Trinity. A bank that could and would best reflect his nature and his way of doing business.

At the time, in the spring of 2003, it appears that he already had a number of “followers” who trusted, liked, and believed in him, as he was able to raise more than 11 million dollars from 258 different investors. Raising this amount of money was unprecedented for a North Texas’ community bank.

Fast forward to now, and the early investors' belief in Harp has been more than rewarded.

Harp and his small team organically compounded book value at 9% CAGR till FY 2023, EPS at a 17% CAGR, and investors now have nine times more money than they did when they first invested in Trinity in 2003. (including dividends)

And all of this was accomplished in a conservative manner, through the dark period of the GFC, the even darker period of ZIRP, and, of course, through the pandemic.

So, what is the recipe behind Trinity’s success?

If I were to summarize it in one sentence, it would be, “Harp nailed the culture right.”

Secret sauce

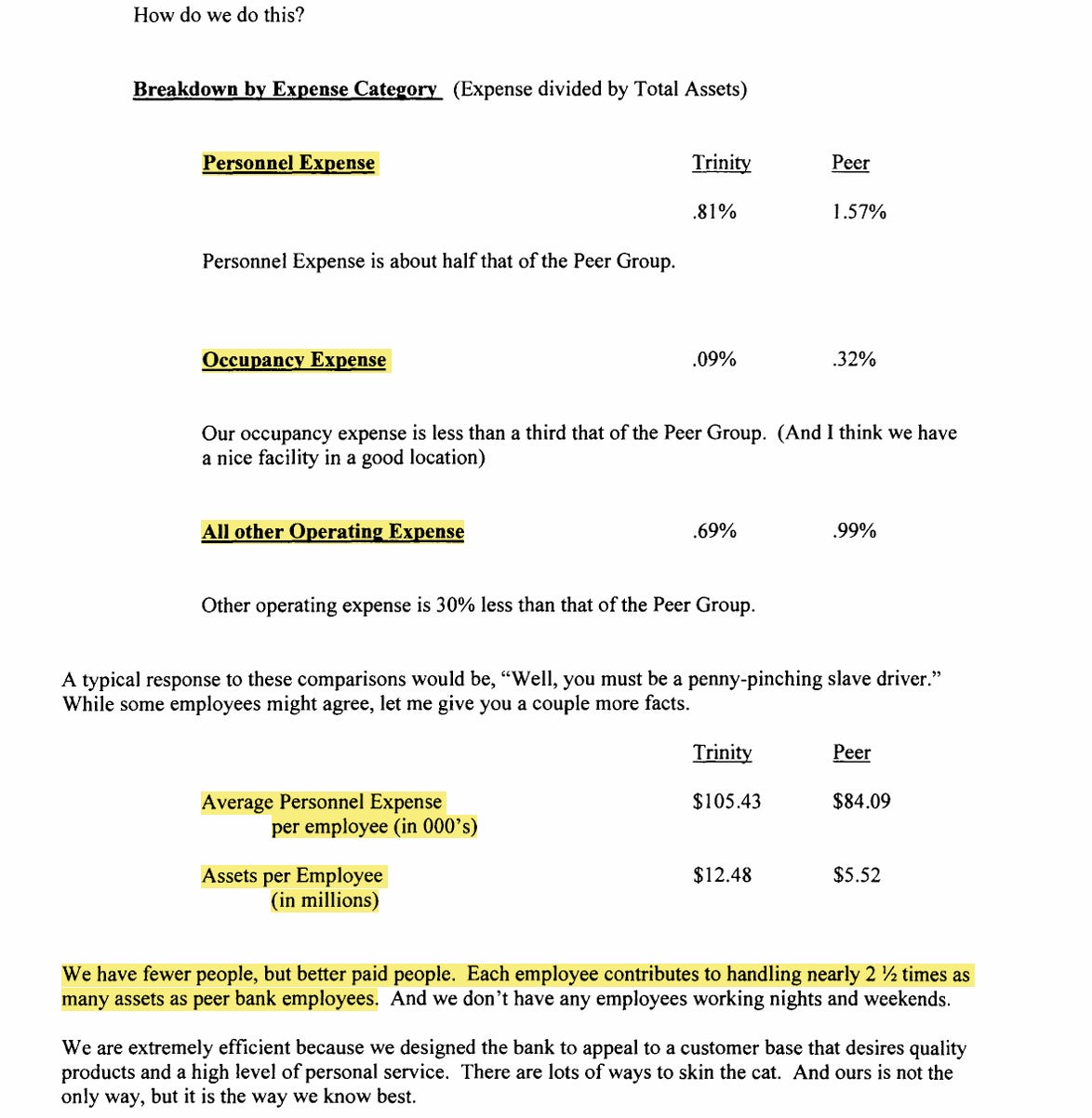

Efficiency

The first theme of Harp’s leadership is his emphasis on efficiency. The efficiency ratio is a standard way to quantify it, calculating how many dollars of OpEx are required to generate one dollar of revenue. The lower the better, of course.

As shown in the chart above, there was no year after 2009 when Trinity needed more than 50 cents to earn 1 dollar in revenue. Smart banking analysts are already aware how impressive this is; however, Harp has placed this into context over the years by comparing it to other banking peers operating in Dallas and Tarrant County, as well as to other US banks of similar size and with branches in major metropolitan markets.

How did Trinity manage its operating expenses so well? Harp explained it well in his Q3 2013 letter.

Trinity’s low occupancy expense stems from the fact that Harp is not “in the business of opening branches,” and he often says that he’d never sacrifice profitability in order to gain market share.

Trinity continues to operate as a one-branch bank to this day. They’ve never tried to acquire a rival bank or open new locations “just to get bigger.” And the one branch that they do have is actually a converted out-of-business hardware store. A converted hardware store with more than $480 million in total assets as of Q3 2024.

It’s safe to say that Harp has a cost-conscious personality and will look for ways to save money that other bankers would deem “beneath them.” Like pulling paper clips out of the trash.

However, one thing Harp doesn’t skimp on is their personnel. Trinity’s employees can be paid well without jeopardizing profitability because they are skilled bankers (lenders), handling only high-impact transactions.

For example, in 2015, Trinity’s employees averaged 22 years of banking experience, with the management boasting over 30 years. Rather than handling small transactions from poor retail, Trinity’s lenders focus on underwriting large loans for select clients, minimizing redundant administrative/support tasks and therefore boosting productivity. As a result, Trinity now manages ~$18M in assets per employee.

Throughout its existence, Trinity has been extremely hesitant to hire new employees, only reserving spots for the most qualified bankers and hiring them when they “just cannot do much more without adding more people.” Trinity, for example, began with 13 employees in 2003, hired only a single employee over the next 12 years. However, after plateauing in 2015, Trinity accelerated hiring and now has 27 employees.

“As I have mentioned in previous letters, the lenders we want to hire are usually not looking for a new position. They are productive and well thought of by their current employers. We have to identify them and then convince them to look at the opportunity that Trinity Bank offers” ~Jeff Harp, Q2 2012

The second ingredient of Trinity's secret sauce is…

Quality relationships with quality clients

“Many have the impression that a small community bank cannot provide products that compete with the large banks. I believe our history will show we have competitive products that many times outperform the large banks and are backed by outstanding customer service. A number of new customers comment to me that our products are more user friendly and offer more feature and function than the large bank that they are leaving. Last month a new customer commented that we visited his office and installed a product for them within 24 hours, and they had been trying to get his previous large bank to return a phone call for 8 days.” ~ current COO Richard Burt, Q2 2016

Trinity takes pride in developing long-term relationships. It claims to know every customer by name and offers top-tier customer service with products tailored to their unique needs:

“And we are very fortunate in that we have a great customer base that is aware that price and terms are an important part of value, but they are not the only components of value. Responsiveness, flexibility, and financial counsel (i.e. “Can I do this?” versus “Should I do this?” “What is the risk/reward ratio?”) are significant components of value as well.” ~Jeff Harp, Q2 2019

By prioritizing exceptional personal service and quick responses over underpricing competitors, Trinity ensures customer loyalty.

Which means customers are unlikely to switch for a slight rate difference, such as another bank offering them 4.1% on cash instead of 4%, ensuring Trinity’s 440M deposit base is sticky, no matter the competition, and decreasing its risk.

This emphasis on person-to-person long-term relationships was best exemplified in Q3 2010, when Trinity literally refused to solicit new deposits “unless it is with people that they can develop a full relationship with.”

Who are these "quality" people, and why does Trinity desire a full relationship with them?

Low-risk lending

Loan portfolio

Trinity bank is primarily a Commercial & Industrial lender, focusing on SMEs rather than transactional RE loans. The largest portion of their loan portfolio consists of safe debt, such as working capital lines, equipment financing, owner-occupied real estate, and interim-construction loans for the commercial market. Most of these loans are of a recurring nature and secured by the borrower’s current assets (WC) or by equipment/RE.

Moreover, fixed-rate loans currently account for only half of the loan portfolio and typically include three to five-year adjustment clauses or are structured as balloon notes that must be refinanced every 5 to 10 years. This greatly de-risks the loan book in the event of an interest rate spike.

Harp’s lending mantra is this: “The key is not to have no problem loans. The key is how much of your money you get back when you do have a problem loan.”

Judging by Trinity’s past performance, this is completely true.

I’ll give you two highlights:

First, Trinity went from 2003 to Q3 2010 without a single NPL and till Q3 2012 without a single loan loss. Yes, that includes the GFC period.

Second, “Since inception (May 28, 2017, will be our 14th anniversary), our loan losses net of recoveries is less than $300,000. I seriously doubt if one can find a financial institution with an equal or better record.”

Trinity really walks what Harp talks. And this conservative approach works wonders, especially when the economy or banking industry is struggling, allowing Trinity to be aggressive when they see “the right deal” and steal market share from banks with higher loan-to-deposit ratios who are forced to freeze lending.

Securities portfolio

“To repeat my earlier comment, we are in the business of lending money. But when we can't find loan volume with an acceptable risk/reward ratio, the excess funds go into our securities portfolio. You need to know our philosophy on investing.” ~Jeff Harp, Q2 2014

As noted, Trinity’s attractive loan portfolio is supplemented with securities portfolio.

The current split between the two is ~ 60:40 in favor of loans. Trinity historically owned corporate bonds, tax-exempt Texas school bonds, and treasuries, but its current portfolio consists of AAA-rated municipal bonds issued by the State of Texas and its counties and cities. This high mix of municipal bonds in total assets reduces net interest margins to what they could be, if Trinity chose to lend more, but it also makes the balance sheet stronger.

Having a large bond portfolio is not something Trinity was forced to do but a deliberate choice in order to maintain a resilient loan portfolio while minimizing risk.

“Parenthetically, let me add here that I have been a commercial lender my whole career. The first thirty plus years of my career, I spent hustling deposits to fund the loans I had made previously. However, as I have told you in numerous shareholder letters over the years, since we opened Trinity we have struggled to generate sufficient loan volume. Therefore, I have been forced to rely more on the investment portfolio to generate returns on your investment. Sometimes, I felt like I was running a leveraged bond fund instead of a bank, and I had neither the training nor the experience. With the recent increase in economic activity and loan demand, hopefully we will see less reliance on the investment portfolio to produce returns.” ~Jeff Harp, Q2 2014

So, what was the outcome of this of sticky deposits + high operating efficiency + low-risk lending/investing strategy? (which I like to call the holy trinity of banking)

Damn impressive.

achieved 57 consecutive quarters of net income growth, which was halted in 2015 only due to increased hiring

grew EPS by 32.2% in 2008 and 17.6% in 2009, without any NPLs, while other banks got wrecked

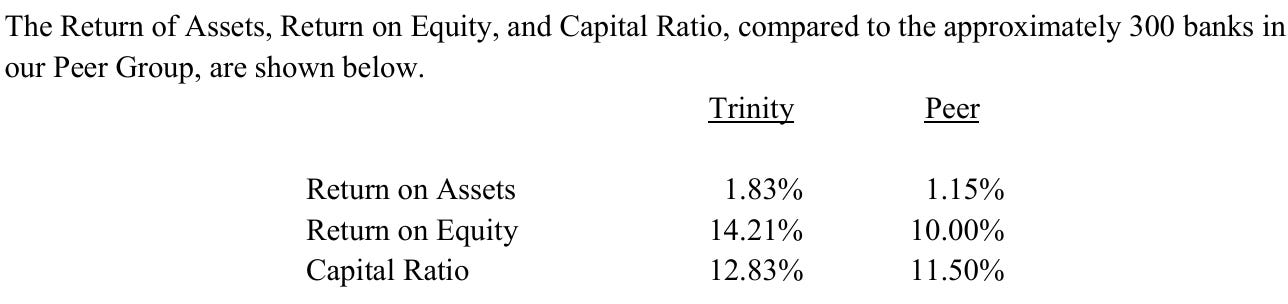

high and consistently improving ROA and ROE, surpassing local, state and national peers

compounded EPS at 17%+ CAGR over 20+ years without dilution, without taking acquisition-risk and while paying out dividends since 2012

FORT WORTH, Texas, January 10, 2011 – According to a recent SNL Financial report, Trinity Bank in Fort Worth is among only 20 banks in the nation, with assets of more than $100 million, which were able to increase earnings every year from 2005 through 2010. The report took into consideration more than 1,150 institutions and included earnings from 2005 through estimated earnings for the year 2010.

And this was accomplished in spite of:

lowest interest rate environment in history during the 2010s

a recession literally named after Trinity’s sector (GFC) and the subsequent regulation

fastest pace of interest rate increases in history following COVID

high securities-to-loans ratio

significantly lower loan-to-deposits and greater equity- to-assets ratio than a your typical bank

not hesitating to “pay” depositors fairly

It’s no surprise that Jeff Harp likes to quote Bear Grylls and says that Trinity is set up in a way to ADAPT, IMPROVISE, and OVERCOME any adversity and sail smoothly through difficult times. I dislike using the term, but I think this is about as “antifragile” as it gets for a bank that isn’t considered “too big to fail.”

Okay – now that you see just how wonderfully Trinity bank is operated, I don’t think there’s any need for me to further bias you or myself. And if you wish to learn more about it, you can read the shareholder letters from start to finish.

But, now, let’s switch to “less good” news.

Passing the torch

In addition to the shift to a higher-rate environment in the last couple of years, Trinity also underwent one significant internal change this year with the retirement of Jeff Harp.

What? Why?

Harp, who is now more than 70 years old, had been contemplating retirement for years. In 2018, he recruited Matt Opitz, a younger guy from Frost, who became CEO just 18 months later, while Harp stayed on as Chairman. Harp continued to be involved in day-to-day activities, focusing on preserving the unique culture that he had built over the years. And trying to pass the torch down effectively.

The real “test” came in late 2023, when Harp took a two-month sabbatical for the first time ever. Seeing the business run smoothly even without him around, he decided it was time to retire.

Obviously, filling the shoes of someone like Harp, who fondly refers to Trinity as “your bank,” is no easy feat—if it’s even possible. However, I’m confident the current management team has what it takes to continue delivering strong results, as they did under Harp’s leadership.

For instance, Matt Opitz seems like a super impressive guy. After joining Frost in 2009—a bank widely regarded as one of the strongest U.S. regional banks—he rose to VP in just two years and became SVP by 2013. Achieving this level of advancement in just four years, with no prior banking experience, is not something you see every day.

Co-Chairman Barney Wiley and COO Richard Burt, both founding members of Trinity, are still here today to further support Opitz’s leadership.

In fact, despite Wiley and Burt being with Trinity far longer than Opitz, they were the ones who recruited him for the CEO role, demonstrating their trust in his abilities and their commitment to shared leadership. Even without Harp around, I have no reason to doubt this talented trio.

If I had to guess how Trinity will evolve from here, I’d expect operating expenses to rise slightly under Opitz, but loan activity to increase as well. And, in my opinion, that slower loan growth under Harp—who was frequently (too) cautious about the economy—was the main factor limiting Trinity’s ability to grow even faster.

Unfortunately, this also explains why Harp never reached his original goal of a 2% ROA and 20% ROE.

I’ll continue to monitor how Trinity’s culture develops through a set of KPIs to ensure it retains the uniqueness it had under Harp. While this may not be a popular thing to say among deep-value investors, I do believe Trinity’s culture provides significant downside protection.

And that brings us to valuation. (no, I’m not using P/culture)

Risk-reward

(always remember, these are just rough estimates.)

Bear case

If loan growth under Matt's leadership doesn't pick up, interest rates fall below 3%, and the efficiency ratio remains “elevated”, we could see a lower ROA than today as well as P/B multiple staying at these historically low levels

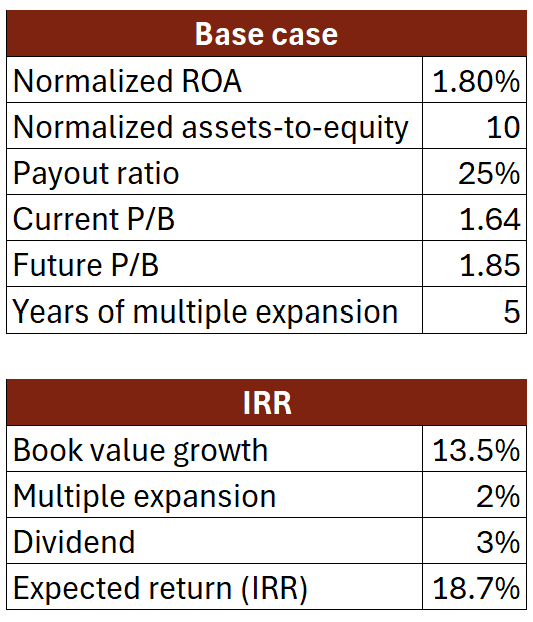

Base case

If interest rates stay lower than today but no above 3%, and loan growth picks up under Opitz, we could see satisfactory net income growth, higher ROA, and a return to the historical P/B multiple mean within 5 years.

“Loan volume (reflective of loan demand) is extremely important to us. A little increase in loans, combined with our efficiency, produces a lot of operating leverage.” Q1 2010

Bull case

If rates remain stable and loan growth accelerates enough for Opitz to achieve Harp’s original goal of 2% ROA and 20% ROE, we could see the multiple expand to at least 2xP/B within 3 years. This scenario seems plausible given the significantly higher rate of hiring over the past 5 years, along with one-off investments in software and other technological upgrades. Going forward, Trinity won’t need to hire (extensively) to “handle” growth, enabling significant operating leverage if loan growth increases. Trump’s recent victory could or should also support this, as was the case in his first term.

“The reduction in corporate tax rates as well as the prospect of less government regulation and interference have generated a much more positive outlook for our customer base.” Q2 2018 (Trump environment)

If you ask me, I’ll gladly accept a low-teens to mid-20s IRR for a bank as antifragile as Trinity. After all, these types of businesses have a tendency to surprise on the upside.

Moreover, management also appears to be cognizant of Trinity’s undervaluation at current prices. They sought to buy back stock earlier this year but were unable to obtain the necessary 2/3 of outstanding shares vote to be approved.

Risks & Illiquidity

As indicated earlier, I think the only major risk to this investment thesis is that the culture deteriorates, reducing Trinity to “just another bank.” This scenario would undoubtedly lead to some multiple contraction, making $TYBT a below-average investment. A poorly executed acquisition or unexpected branch openings would be immediate red flags for me to exit.

I believe the main reason why this opportunity exists is the significant illiquidity of $TYBT stock, best evidenced by its low beta and minimal share turnover. Or the fact that weeks can pass without a single share changing hands.

Even savvy banking analysts I’ve spoken to hadn’t heard of Trinity before I mentioned it, further reinforcing my view that it’s flying under the radar. Its 1.6x book valuation also makes it less likely to stand out on screens.

The second factor that may make investors hesitant is uncertainty about future interest rates. However, I don’t see this as a concern, given that only about 30% of Trinity’s deposits are non-interest-bearing. Additionally, Trinity has shown it can achieve strong NIM margins, ROA and ROE even during ZIRP, indicating its current profitability is not a one-time anomaly.

The third reason investors may be reluctant to buy the stock is concerns about Harp’s departure. Or the recent slowdown in loan demand during this pre-election uncertainty in the past few quarters.

And that’s it. That’s the story of why I decided to invest in a bank for the first time ever.

Before I go, I’ll leave you with one last highlight from shareholder letters:

“I have attached to this letter a copy of an email from one of the bank rating agencies. We are pleased to report that Trinity Bank was rated #1 in Texas and #3 in the U.S. out of all 6,500 banks (based on earnings, asset quality, capitalization, growth, and liquidity). This performance is proof that our results are superior. We will do everything within reason to continue this level of achievement.”

Thanks for reading! And if you wish to support this kind of work, consider becoming a free or paid subscriber.

disc: I have a close to 5% position and will probably continue buying in the future

The Mikro Kap uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers.

Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks. Due your own due diligence. The author reserves the right to buy or sell any securities mentioned in this article at any time, without prior notice.

This is quickly becoming my favourite Substack. Looking forward to diving into those letters. Thanks!

How do you actually buy the stock? On IB it comes up as No Opening Trades: DTC Chilled or Ineligible.