Give Credit Where Credit Is Due

a deep report on Credit Bureau Asia, $TCU.SI

You've seen me analyze Italian newspaper companies, boring spare parts distributors, and Florida orange growers. You've also seen me research NYC office REITs, UK greeting card retailers, and Australian gold drillers. I bought very small companies, very cheaply, in industries that most investors would either find disgusting or never dare look at.

Fortunately, that approach has served me well in the past. And my preference for overlooked downside protection over predicting growth rates will undoubtedly continue in the future. However.

However, with this write-up, I’m putting my “strategy “on hold. At least for a little while. And I’ll explain why I was comfortable paying a double-digit (normalized) FCF multiple for a micro-cap. For the first time in my life.

Please don't call me a “compounder bro“and allow me to introduce:

Credit Bureau Asia

The company is headquartered in Singapore and listed under the ticker $TCU.SI

As the name implies, CBA is a credit bureau business that operates across Asia. It currently has operations in Singapore, Malaysia, Cambodia, and Myanmar, with plans to expand in China and Vietnam shortly. However, for the time being, the only important geography to consider and analyze is their operations in Singapore, which account for 96% of total revenues as of fiscal 2023.

FI data

Although credit bureaus may sound like something very complex and a business that could take months to understand, the model is actually pretty straightforward.

Credit bureaus, also known as the “FI data” segment for CBA, serve as data providers for financial institutions (FIs).

The simplest transaction looks like this:

You, as a bank or another FI, subscribe to CBA. Once subscribed, you give CBA credit and risk information data on your customers, and with it, you gain access to the numerous services CBA offers.

The main service CBA offers is a consumer credit report, which is mostly used when a banker is in the process of approving consumer loans. Credit reports include critical information for every bank and for every banker to assess how creditworthy an individual is. In other words, banks and other lenders want to know about your financial health and how likely you are to pay your bills on time, or in this case, your mortgage, your auto loan, or your credit card debt. Credit reports contain important information such as credit account status history, previous inquiries made by lenders, outstanding balance, monthly instalments, and so on.

The reason why a bank does not conduct this type of work in-house is a lack of necessary external data. If done in-house, the banker would be forced to approve a loan based entirely on the bank's own internal data and would lack the necessary insight into the into the individual's previous dealings with other lenders. They'd lack crucial, objective information to analyze a potential client's behavior and complete risk profile. And they would probably be too afraid that he or she is hiding something.

CBA sits in the middle of all loan-approving in Singapore. The seat so advantageous that you can take a cut almost anywhere you want. FIs pay to join your service, FIs then provide you the data for free, FIs then pay you an annual subscription; and, finally, FIs pay you for each credit report or any other service they need from you. Your main value add is in analyzing, organizing vast fields of data, and providing it back to lenders.

CBA began operations in 2002 and was a first mover in Singapore. It has since onboarded 200+ financial institutions as customers and all retail banks as credit bureau members. This first-mover’s advantage is critical in the credit bureau business since it leads to “winner takes all scenario” if you're early, or “winner takes most scenario” if a few of you are "early." Your data is extensive, ever-growing, and timely, making it difficult for new entrants to replicate it. They lack CBA’s 20+ years’ worth of data (500 million+ credit files, to be precise) and the necessary infrastructure to handle it. Just imagine how difficult it would be for a new entrant to persuade FI to onboard on a new and inferior service or give you their data for free. After all, banks are only willing to “give up” their data if that provides them with a consistent access to quality information, allowing them to make higher-quality decisions.

So, it’s no surprise that CBA has a 99.9% market share in Singapore and operates as an effective monopoly, capable of meeting all the needs of the market. The remaining 0.1% market share is held by Experian, one of the three major worldwide credit bureau companies. As of 2020 (the most recent available data), Experian has had only 4 FIs as members, providing them with a limited database, in contrast to CBA, which has onboarded all of Singapore’s 31 retail banks and has the largest database. This makes Experian’s position in Singapore quite weak.

This is just my guess, but I believe the reason why Experian is still “competing” in Singapore is because of the access to data, which allows them to bundle it with other services and offer it to their international customers. This is similar to what CBA is doing in Malaysia.

CBA also offers a variety of services that complement its core “sale of credit reports” business. The first add-on is credit scoring, which serves as another independent fact-check on the client’s creditworthiness. It is adopted by all CBA’s members and is comparable to FICO in the US, however not as entrenched.

Other add-ons include credit monitoring, which is used to track the behavior of existing customers after the loan is approved, as well as other data analytics, which is used to assess banks performance against the industry. CBA also provides various customized solutions and periodic reports to satisfy the individual needs of its subscribing members. Furthermore, I noted CBA’s main customers are large FIs and banks, but individuals can also obtain a personal credit report from CBA if they want to check and verify it before applying for a loan. Non-FI businesses are also customers, and they use credit reports for risk management, compliance, KYC checks, employee screenings, and other purposes.

Now that I have noted that this is a monopoly providing services to its members that they can’t really go without, it’s also worth noting that, despite the word “credit” in its name, this is not a business subject to the economic cycle.

In expansionary periods, CBA grows with credit activity and, with it, greater demand for credit reports. However, a slowdown in loan appetite during recessionary periods doesn’t result in a corresponding drop in demand for CBA’s services. During recessions or financial sector downturns, FIs increase the frequency of bulk credit risk checks on their (new) clients and as well as their spending on monitoring services, in order to better track their NPLs and avoid undesirable risks.

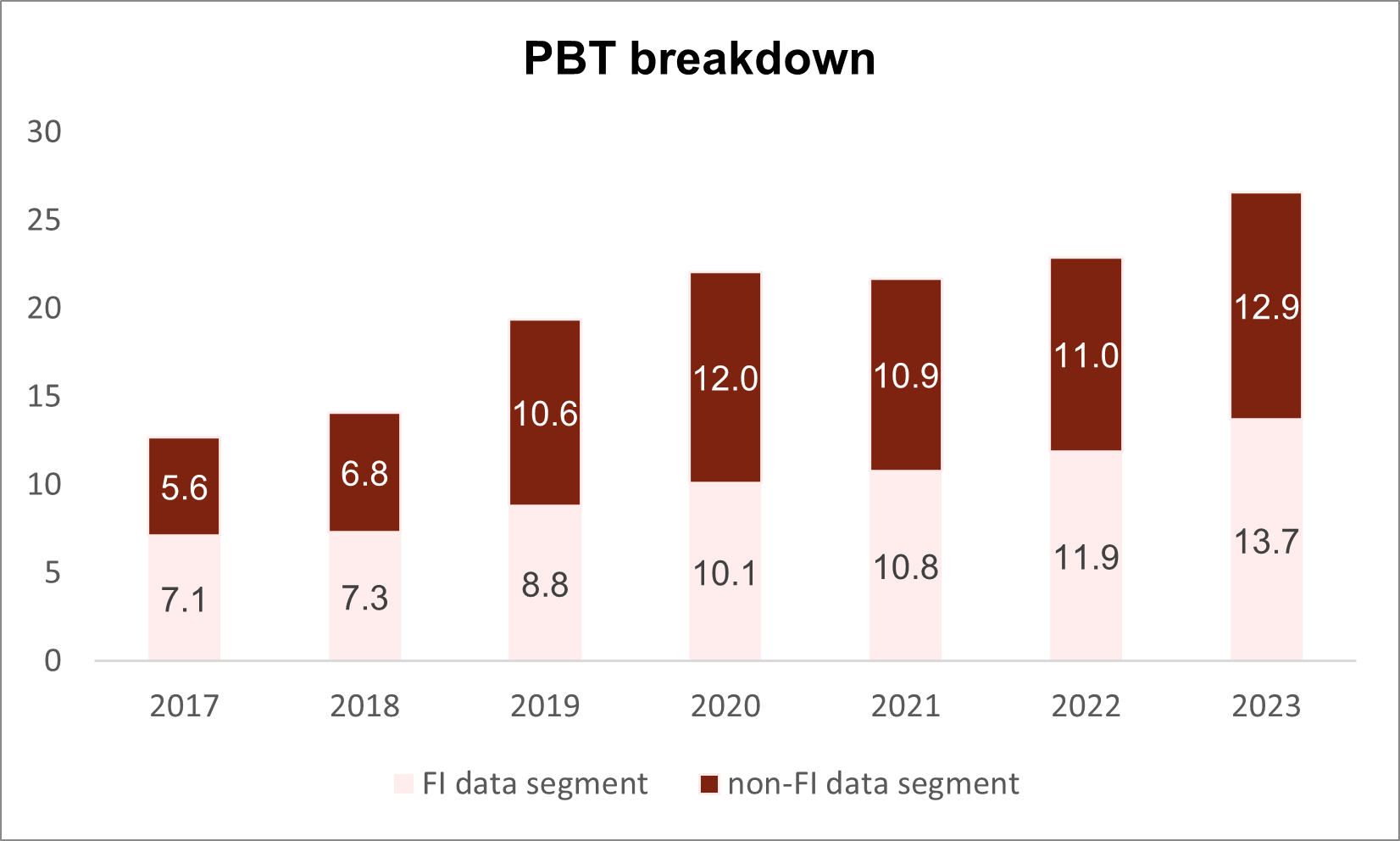

The recession-proof nature of CBA’s business is best demonstrated in 2020, when the FI data segment revenue grew 5% and the segment's PBT grew 15%. Or look at how the growth continued in 2022, despite all the concerns around SVB, FRP, and other regional banks. To top it all off, CBA's FI data business has steadily grew revenue and PBT year after year since 2017 (the oldest accessible data).

I’ll conclude this section with the following statistic: The only available data on credit report pricing shows that 20 million standard consumer reports were sold for 16.2 million in 2019. This means that five years ago, the average consumer credit report cost was only 81 cents. And, in my mind, 81 cents for a credit report can only mean one thing—untapped pricing power.

Non-FI data

Aside from the FI data segment, which accounts for 46% of total revenue as of 2023, CBA also operates a non-FI data business segment, which accounts for the remaining 54%.

28% of the non-FI data business also runs a credit bureau model. That sub-segment is called the “Commercial Credit Bureau." The model is very similar to the one described above; lenders also subscribe to CBA's service and purchase credit reports, but as the name implies, this business line deals with commercial credit, not consumer credit. So, lenders utilize this service when approving loans to businesses. Also, it doesn't rely on data provided by FIs but rather on corporate data obtained from public registries such as ACRA (Accounting and Corporate Regulatory Authority of Singapore).

In addition, CBA developed an online Singapore Commercial Credit Bureau. The website is primarily to meet the needs of SMEs and other real-economy businesses who want or need to better understand the credit and risk profiles of (potential) business partners or competitors. Moreover, as was the case with the consumer credit bureau model, CBA leverages its extensive data to provide additional services to customers. Here's an example below:

Commercial credit bureau segment has an even more-monopolistic position in the market, as it holds the sole license for commercial credit in Singapore. Furthermore, this segment also couldn’t care less about what the cycle is doing since during recessions, companies do more thorough checks on their (potential) suppliers as well as increase the frequency of credit checks and monitoring of their customers. The lack of revenue decline during down-cycles can also be observed in 2020 numbers below.

Let's continue.

Global Credit Risk Management is the bread and butter of CBA's non-FI data business, accounting for 60% of the segment's revenue and a third of overall revenue.

The business model differs here and is the reason why the non-FI data segment got its name.

CBA manages this sub-segment as a JV with Dun & Bradstreet, a large global risk management player. They collect and combine data from a variety of publicly accessible registries, from D&B Worldwide Network, which provides access to business records from 200 different markets, as well as payment information provided by businesses that use CBA's payment bureau service. Public registry data is obviously not exclusive; however, 250 million business records-sized D&B data and payment bureau data are.

CBA serves more than 6,000 customers in this segment. Typical and most valuable customers are large multinational corporations such as P&G, Samsung, or Unilever, as they want to have access to this wide range of business information, in order to assess a potential partner or evaluate the risk of a transaction.

Key products include risk management reports, KYC checks, credit and counterparty risk checks, and anti-corruption and anti-money laundering checks:

There are three players that operate in this industry in Singapore. As of 2018, the most recently available data, Experian had the largest market share with 57%, followed by CBA with 40% and Crif BizInsights with the remaining 3%. Both globally and in Singapore, credit risk management is also the “winner takes most “type of market.

Although barriers to entry to this industry are lower than those in the FI data segment, one barrier remains: data. In order to compete, you still need to have an extensive, regularly updated database as well as infrastructure and models in place to properly analyze it and provide it to customers instantaneously, with the click of a button. Few companies do.

Among the players who can do so, such as Experian, the competition is primarily centered on how they display information. Experian might use different types of data in order to deliver insights to their customers than CBA. So customers choose one company over another based on the specific information provided and how it is presented, or simply because they are familiar with the format in which a particular company presents their reports. Once you've become accustomed to a specific standardized format and are a subscriber to CBA, Dun & Bradstreet, or Experian, you usually don't switch. This means that the product is sticky, with an average yearly churn rate of 7%, and is safe against existing competitors or new entrants trying to grab your business.

During expansionary periods, Global Credit Risk Management grows with the increased demand for loans, business transactions and overall trade activity, which drives a greater demand for reports. Positively, this business line is also resilient throughout downturns. During recessions, corporations become more concerned about their partners’ finances and tend to perform credit and risk information evaluations more regularly. Especially their overseas clients, who want to know that their suppliers or customers aren’t going bust and will be able to pay their invoices on time.

This is best illustrated in the chart below, which shows consistent revenue growth year after year after year. Regardless of the disruption in supply chains in 2020 or the shutdown.

The final part of the business, and the last sub-segment of the non-FI data segment is Sales & Marketing Solutions. It generates 12.5% of the segment's revenue and 6.8% of the total. It uses the same data as other non-FI data segments but offers S&M solutions to help companies generate leads or market their offerings. Although, the business line is not as much of a “necessity” as others, it is a good example of how a business like CBA can leverage its extensive data.

In this situation, you as a customer, based on the data CBA and D&B have, can either find new leads and generate more revenue or can become somebody else’s lead. You can also do stuff like market segmentation or customer profiling. This business is also sticky and hard to replicate because CBA is D&B’s exclusive distributor in Singapore for this service. However, it is not recession-proof. Naturally, the first thing corporations cut during downturns is sales and marketing.

Now, that I’ve broken down CBA into segments and probably overwhelmed you with too much information, it’s time to see what the business looks like as one whole and sum things up.

Whole in one

Another attractive feature of CBA is the geography in which they operate. Singapore is naturally a more appealing place to conduct this type of business because it is Asia’s, if not the world’s, center of trade. It is where multinational companies like to setup their HQs, where all the decision-making regarding credit and risk takes place. Being the wealthiest Asian country with the freest market economy also helps with the demand for credit.

Credit bureaus are such a necessity in any economy that if CBA were to be displaced and someone started another credit bureau from scratch, it would cause an instant recession in Singapore. There would be too much information asymmetry in the financial sector, and banks would be afraid to approve as many loans based on inferior external data or inadequate internal data and would increase interest rates. Credit reports make the banks and thus the economy more competitive since they allow them to be more confident in the data, authorize more loans, or offer lower interest rates without fear of their NPLs skyrocketing.

The positioning is monopolistic and will remain so; the products are indispensable; and the business is more than 90% recession-proof.

Also, while I don’t like quoting Buffett in my write-ups, I think this business is a textbook example of a great business by his standards. An asset-light franchise that can grow without having to retain earnings.

To double-check this argument, you only need to take a quick glance at the dividend payout ratio and revenue growth. The business increased revenue organically from 40.6M in 2019 to 54.1M last year, or at an average rate of 7.5%, while paying out more than 110% of its net income (after minorities) and 118% of FCF as dividends in the same period. This means that this isn’t some kind of business that needs to retain earnings and thus have a lower dividend payout ratio in order to grow. It can grow without the incremental capex; it can grow for free.

This “infinite” ROIC is best shown when trying to calculate invested capital. In most years, the invested capital is negative, while in years when it marginally turns positive, the business starts generating ROIIC in 1000s of%. Also, adjusting the equity for the cash pile and calculating ROE paints the same picture.

ROA adjusted for cash-pile confirms CBA’s ridiculously attractive economics.

So, before I go into its future growth potential and valuation, it’s be useful to say a few things about the ownership structure and capital allocation.

The insiders

The company’s two main faces are Kevin Koo, the founder and the current CEO, and William Lim, who joined the company more than 20 years ago and is currently an executive director at Credit Bureau Singapore. Mr. Koo owns 64% of the business while Mr. Lim owns 6.2%, making them aligned with our interests.

Other board and management members don't own a lot of stock; however, most have been with the company for a decade(s), during its formative years.

(PS - one of the directors just bought 100K shares on the open market about a month ago.)

From an operational standpoint, there's no way to tell how good or bad they are. It's a business that even my little sister could run and generate good returns. However, I don't find the management particularly savvy when it comes to capital allocation and maximizing value per share.

For starters, an acyclical (if that’s even a word) business of this quality, has far too much cash on its balance sheet. Current net-cash after minority interest size is 40M, and IMO it should be run with at least a net-debt position of that size. Also, despite them authorizing the buyback twice in the past few years, they have never used it, and I doubt they will in the future. The stock is too illiquid for a proper buyback, and I don't believe they are “sophisticated“ enough to do a tender offer.

As there are no real capex opportunities, the only thing left to do with FCF is pay out dividends, which management has been doing consistently while waiting for an acquisition opportunity to deploy their spare cash:

“CBA has been growing organically since inception, but we are actively pursuing inorganic growth opportunities. However, the management is cognizant of the many public-listed companies getting embroiled in financial difficulties after their mergers and acquisitions spree soured. Hence, we are taking a very prudent approach and will only consider opportunities which will add real value to CBA’s long-term objective and at the right valuation.” ~ AR 2023

All in all, with this wording and the insider ownership, I doubt they would overpay for a large acquisition. And although one fellow investor, whom I respect, has talked to them in the past and didn’t find them particularly inspiring, I think it’s hard to destroy shareholder value when you have a 100% payout ratio, no need to employ capital, and a monopolistic business generating incredibly high returns.

Although dividend payout is not fixed, they loosely aim for at least 90% of net profit after minorities. High dividends are especially appealing for SGX-listed companies since both locals and foreigners pay no withholding tax.

Now that you’ve read my (biased) view about the company, it’s time to cover the…

Risks

The main risk comes from their Dun & Bradstreet license. CBA is heavily reliant on D&B’s licenses for its non-FI data business, and if D&B were to decide to stop providing them data or start increasing costs unreasonably (CBA currently pays a fixed royalty for D&B’s reports), it would severely impact CBA’s positioning in the non-FI data segment. Also, revenue from the sale of reports to D&B typically accounts for a quarter to a fifth of its total revenue.

The two companies had disagreements in the past, but they’ve been working together for 25 years, and their contracts have always been renewed. Most recently in January 2024 for another period of five-year period.

Going forward, I think there’s only a minuscule likelihood the license won’t be renewed since CBA and D&B have a close, interdependent relationship. CBA is the sole and exclusive distributor of D&B reports on foreign companies to their Singapore customers, while D&B is the sole and exclusive distributor of CBA reports on Singapore entities to their international customers. Meaning, one is encouraged to do business with the other since they would otherwise lack critical international or domestic information, required to sell reports.

Another license risk relates to commercial and consumer credit bureau licenses, which are renewed every 5 years. Due to my prior ramblings around CBA being a necessity in the Singapore economy, I don’t consider this a risk at all. I just thought it’s a piece of information worth mentioning to you. The license doesn’t even get mentioned in the annual report.

The third risk comes not from the business, but from the structure.

If I wasn’t able to follow the money, this kind of complex structure would be a huge warning sign for me. However, it's not hard to “follow the cash” when a company pays you 100% of their FCF share after minorities as dividends. Moreover, CBA was built up through joint ventures and subsidiaries in order to secure the right local or international partners. This means that they use jointly owned software technologies and licenses to run their business.

For example, they rely on TransUnion in credit scoring and work with FICO's algorithms for commercial credit bureau segment:

“We currently rely on credit scoring algorithms from providers of business intelligence services in the determination of credit scores featured in our commercial and consumer credit reports. In particular, CBS’s ‘Generation 2’ score, is based on an algorithm developed by TransUnion which takes into account factors including the length of one’s credit history, amount of overdue balances, presence of delinquency, litigation or bankruptcy as well as payment behavior. In addition, CBS’s SME Blended Score is based on an algorithm developed by FICO which ties together both the credit profiles of the owner or director as well as of the SME in question to provide a comprehensive credit risk profile.” ¨~prospectus

The partnership/collaboration approach is what CBA's peers have done in Asia as well, so it makes me think of it as an industry standard for setting up credit bureau businesses in other countries.

Other risks worth mentioning but not delving into are lower regulation, which lowers barriers to entry, and a potential downturn in international trade as a result of US-China trade wars, or even real wars. And supplier concentration or unwanted regulation from the Singapore government.

Now back to positives and…

Growth prospects

Although, after reading the prospectus, it's not hard to figure out how competitively advantageous CBA is and how high returns it can generate, projecting future growth is a far more difficult endeavor.

For example, this is what Frost & Sullivan, their independent IPO researcher, had highlighted as key market drivers:

If somebody was to dig deep, he would most likely find the expected growth rates for each of the growth drivers, but he would never be able to determine the actual impact of each driver on the revenue growth.

For example, credit card penetration in Singapore is still much lower than in most developed countries and should grow faster. However, more than 98% of the population over 15 are banked, indicating there's no room to grow there. So, which factor should bear more weight?

IMO, the most important trend for the FI data segment is the consumer and commercial loan activity, whereas the trade activity is what is heavily driving the non-FI data segment.

However, while it’s difficult to be precise with future FCF growth, there are numerous trends that should and will boost growth further, both in the short term and long run. The trends that enabled CBA to increase revenue year in and year out, without missing a beat.

Aside from the increase in value of consumer and credit loans, I want to list the three key incremental drivers for each vertical:

geography

inorganic expansion into new ASEAN markets

expected launch in China and Vietnam

increase in banked population in countries where CBA already operates in

macro

population and number of households growth

credit card penetration growth

rate cuts or inflation

industry

increase in financial industry regulation, due dilligence and compliance requirements,

expanded service offering and new customers from recently onboarded digital banks

further penetration of Singapore market which had a credit bureau coverage rate of 64.2% as of 2019

micro

widening credit bureau membership base to include insurance businesses, utilities, moneylenders and leasing companies

leveraging data and AI to launch new services or bundle existing services in a different way

further penetration into the corporate credit business

operating leverage

employee expense as a % of revenue should decline over time

FI data is higher margin and growing faster than the non-FI data business

non-Singapore geographies getting to scale

Given all of these variables, it is not unreasonable to expect CBA will grow FCF at, at least, a high-single-digit CAGR over the long-term and probably well into the double-digits in the short term.

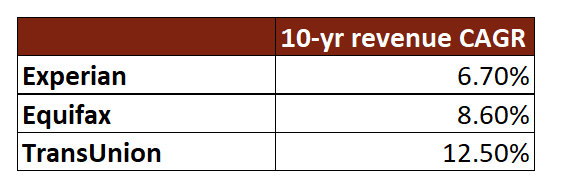

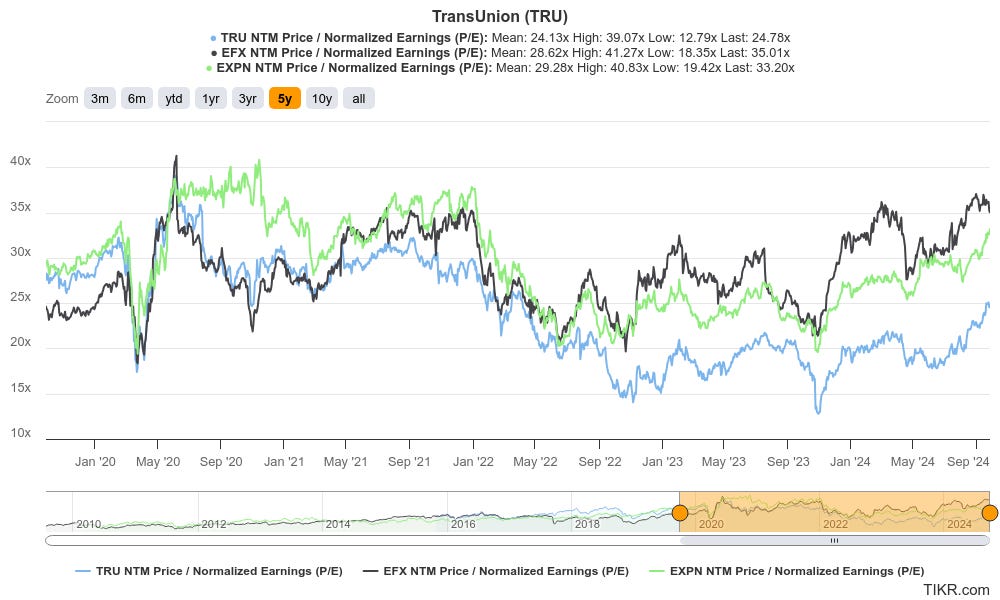

We can “test” it against CBA's historical results as well as compare them to its credit and risk information players who dominate international markets. Specifically, Experian, Transunion, and Equifax.

Since FY 2017, the oldest available data, CBA revenues have grown at a 7.2% CAGR to FY2023 and another 12.2% in H1 2024. It also grew net income after minorities at a 11.1% CAGR within the same period and another 25.1% in H1 2024.

And when compared to its, much larger global credit bureau peers, we can see a similar revenue growth trends of 6.7-12.5%

Now onto the

Valuation

Due to its asset-light nature and ability to grow without retaining earnings, I valued this business as a bond with a coupon that grows into perpetuity.

Since CBA has paid out an average of 118% of FCF as dividends over the last 5 years, I am taking FCF as a coupon. And with a strong balance sheet in place and no growth capex required, I expect this practice of paying out all FCF as dividends to continue.

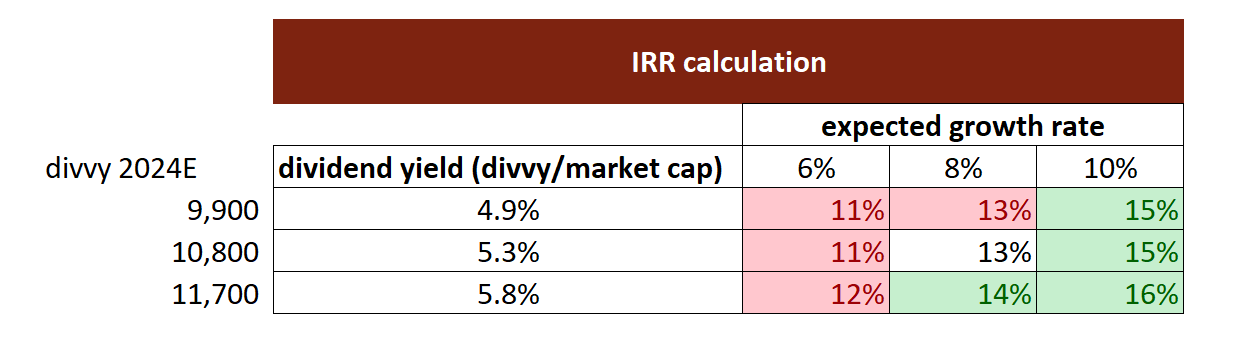

I handicapped three growth scenarios, and I find them all reasonable when estimating future FCF growth.

The reason I am not more precise with my numbers is because it is impossible to do so. Revenue growth for CBA is unknowable, as is the amount of operating leverage that will kick in. However, the good news is that you're buying from investors who also don't know the true value. No one has the “insider information “here or an ability to precisely project growth; not even management possesses such mystical powers.

I believe an acceptable method to think about the valuation of this business is to stick to different FCF growth scenarios ranging from 6 to 10%.

I expect CBA to earn between 11M and 13M in FCF this year. By dividing FCF and EV of 162M (adjusted for non-controlling interests), I get the FCF yield number, which is then added to the expected growth rate number to calculate the IRR.

These are potential returns one might expect from this investment, without taking into consideration multiple expansion or contraction.

And if you want to be even more conservative and assume that only 90% of FCF will be paid out to you in the long run, and that 40M in net-cash after minorities on the balance sheet will never end up in your pocket or will be spent in ways that don't create shareholder value. Your expected returns would look something like this.

I noted that I didn't include multiple expansion in my IRR calculations. However, I wouldn't be surprised if the multiple for a business of this caliber re-rates in the (not too distant) future. Only 4 years ago, CBA's IPO at 0.93 SGD per share was 60 times oversubscribed. IPO investors fell in love with the business, and the stock quickly rocketed and debuted at 1.15 per share, showing investors’ readiness to pay 40X P/E for this business. Compared to 18x today.

I'm not saying it will shoot back up to 40x, but I'm not saying it will stay at 18x either. Especially after the 25% EPS growth recorded in H1 2024.

Furthermore, while I do realize this is a SGX listed micro-cap business, when compared to their Western markets' peers, you can clearly notice the valuation disparity and how high of a multiple these businesses usually warrant on the market.

Interest rate cuts in Singapore might be a trigger for a re-rate of this business, simultaneously boosting loan and trade activity among CBA's customers as well as making CBA's growing dividend yield that more appealing compared to treasuries.

Now that my valuation work is complete, the only question remaining is why the market is handing me this opportunity.

Structural advantage

I find this situation as unique as I do this business. IMO, this is a good example of a stock where retail investors have a structural advantage over institutions.

For starters, as I previously mentioned, this is a 202M market cap company 70% owned by insiders. Moreover, the top 20 shareholders own 95% of the company, and I'd bet most of them are here for the long term. Which means there isn’t much stock for the taking on the open market.

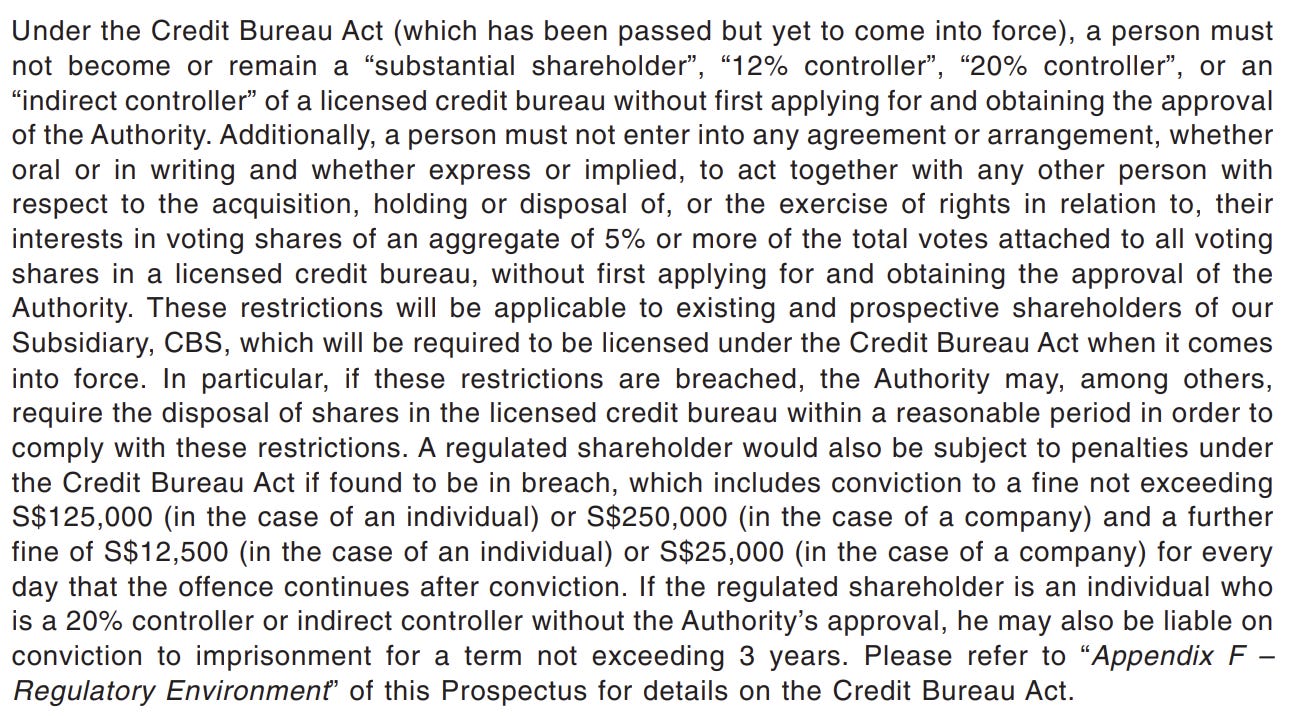

Additionally, under the rigorous regulation of the Credit Bureau Act of Singapore, there's a specific that prohibits you from buying 12–20% of this microcap without prior approval. Also, you cannot buy or sell more than 5% of the company without prior clearance of the regulator. If you do that, you will either face fines of hundreds of thousands of Singapore dollars or, in the worst case, jail time.

If a tiny free-float adjusted market cap doesn’t prevent institutions from participating, this sure as hell makes it that much more difficult. Or impossible.

Furthermore, Mr. Koo and Mr. Lim and their JV partners have agreed to maintain a minimum of 51% and 2% shareholdings in CBA, respectively. Their shares are currently locked up in a moratorium account, keeping most of their stake in the company unavailable to potential institutional investors.

This illiquidity can be seen most clearly in the average yearly share turnover, which is in single digit percentage range, or in the 5-yr beta which is currently at 0.06. This stock couldn’t care less about what S&P 500 or the stock market are doing.

Aside from the illiquidity concerns, there are a few more reasons why other investors might be overlooking this stock.

The first thing they notice is an 18x P/E ratio for a micro-cap, which is either an instant pass for many or won't pass the screens.

If they do look at the financials, the only thing they'll notice is unimpressive revenue growth and “not that high” ROIC/ROE or ROA. What they won’t realize at first glance is that this revenue growth came for free and that ROIC/ROE and ROA numbers appear low because of the cash on the balance sheet, leading them to believe that business economics are not as strong as they truly are.

The ugly stock chart since the IPO also makes most investors uneasy. Not me, though. If this stock suffered another 30-50% drawdown, I'd probably make it a core 15-20% position.

It's perhaps the highest-quality micro-cap business I’ve seen in a long long time.

However, my pickiness around valuation, other opportunity set, and the trend in the stock price makes me think that there will be enough time to DCA into this one. And that I shouldn't go “all in“ at once. For now, I'm keeping it at 6% of my portfolio.

That’s it from me today. Thank you for reading! And if you wish to support this kind of work, consider becoming a free or paid subscriber.

This is NOT investment advice. All content on this website is for entertainment, informational, and educational purposes only and should not be considered to be advice of any nature. Due your own due diligence.

This was a very well written thesis, one could even say it's a model thesis. I enjoyed reading it highly. Credit Bureau Asia should definitely be monitored in the future.

Stupid question: help me understand Credit bureaus valuation at the moment. So looking backwards now 2024 FCF was 29,2 million. EV is 266,33 million. Almost 11% yield?

Still it has only 3% divident yield with 82% payout. Do you think the yield is wrong or do you think its realistic to assume that all the (fcf)yield would be paid as a divident in the future? Thanks !