2023 was a good year.

In the midst of Mag7 outperformance and micro-cap underperformance, my portfolio did well, delivering 29% pre-tax performance and outperforming my two benchmarks.

However, I’ve made more mistakes than these results suggest and learned more lessons than one could hope for in a year when the S&P is up >25%.

So here it is: what I have learned, what I have unlearned, and what I'll focus on in 2024.

Losers

First, let’s start with the losers. Or with a loser. Thankfully, I had just one this year. His name was Big Lots. (You can read the original write-up here, and the selling rationale here)

Losing money on Big Lots reminded me just how important the “management” factor is when investing in industries with low/no barriers to entry, such as retail, restaurants, or hotels. When a business lacks a moat, you’re at the mercy of the operators running it. And the more of a “turnaround story” your investment setup becomes, the more your success is dependent on the competency of the people running it.

Damn retailers such as this one are likely one of few of the businesses in the markets, where having 31 out of 34 years of consistent profitability doesn’t mean a thing and where one management change or one larger inventory build-up can be the difference between a decent business model and a model that’s 12 months away from bankruptcy.

Also, looking at this another way, searching for beaten-down retailers where there has been a management transition can be a decent hunting ground. And if the new guys running it have a reputation for honesty, a track record of competency, and good cap allocation, that could be your inflection.

To be fair, I was aware of the risks before investing in this one and therefore sized it small. However, the guidance misses, the promotional conference calls, the data cherry-picking, the buzzwords and excuses, the over-promising and under-delivering were all present before I bought, and I was still dumb enough to pull the trigger;

“Big Lots is not for everyone. This is not the type of no-risk, high-reward opportunity that I would typically look for in the market. This is a unique investment that I believe has value only for a specific kind of investor.

The profile of an investor who is either well-diversified so that this is only one of many bets with favorable odds or a young investor who can still earn a majority of his portfolio in a given year so that the permanent loss does not bother him.”

“High risk, higher returns, my friends. You will either be left holding the bag, or it will prove out that the business is at least as stable as it has historically been, and you will make a killing from the revaluation.”

Narrator: he was, in fact, left holding the bag.

P.S. When you hear a statement like this on the conference call, it's time to run away:

“On that note, tough times don't, last tough companies do, and Big Lots is damn tough.“

Winners on paper but losers in my mind

After holding my $ARNT(ZSE) and $PPH.L positions for about a half-year, I was able to sell them for single-digit gains plus the dividend.

The takeaway from these two investments is something I should probably just frame on my wall.

When an asset-play lacks a catalyst or growth, capital allocation becomes crucial!

Being cheap is not enough. This is where you’ll get a value trap.

I’ve written about this very same concept both on Substack and Twitter multiple times, yet, here and there, somehow, I still manage to buy the business with a lousy capital allocation strategy or a business where underlying assets aren’t causing the discount to widen by growing in value year after year.

From here on, I will either not invest in asset-heavy businesses that lack a clear catalyst but are heavily discounted on a P/B or P/NAV basis (unless there is like an 80–90% discount to the NAV that I’m certain about). Or I will size them smaller in the portfolio and follow Dave Waters's "one-day stocks" method.

You can find more on my selling decision here.

Flip-flops

Another thing these three mistakes reminded me of was the necessity of selling as soon as you begin to feel uneasy about the stock's decline, rather than wanting to buy more. Holding onto something only for the sake of being labeled a “buy and hold” investor or a “long-term horizon” investor has always cost me money.

Flip-flopping shows that you continuously try to disprove your thesis and do not allow yourself to fall in love with ideas. As a result, your mind is flexible and is more concerned with not losing money than with appearing smart on Twitter.

We are all in the process of learning as investors, so it’s only natural to change our minds and admit our mistakes in order to grow. And - if you ask me, it's far better to grow while not losing money in a concentrated position.

All in all, I plan to maintain a larger portfolio turnover in the future.

Winners

I don't think it's very beneficial to analyze stock picking ability where gains(losses) have yet to be realized. Therefore, the only big winner I'll mention in this section is Vornado; I sold half of my position 3 weeks ago, locking in an 88% gain over <1 year.

This one reinforced my belief that leaders in troubled industries can be terrific investments. These often lead to an event triggering a huge drop in supply (in this case, lending + WFH trends), competition dying or exiting the industry, and eventual survival of the fattest scenario where the pricing power of survivors skyrockets.

Especially when Mr. Market is discounting them as if they were junk…

(my bet is that both $CARD.L and $RCS.MI will join this club in the next few years)

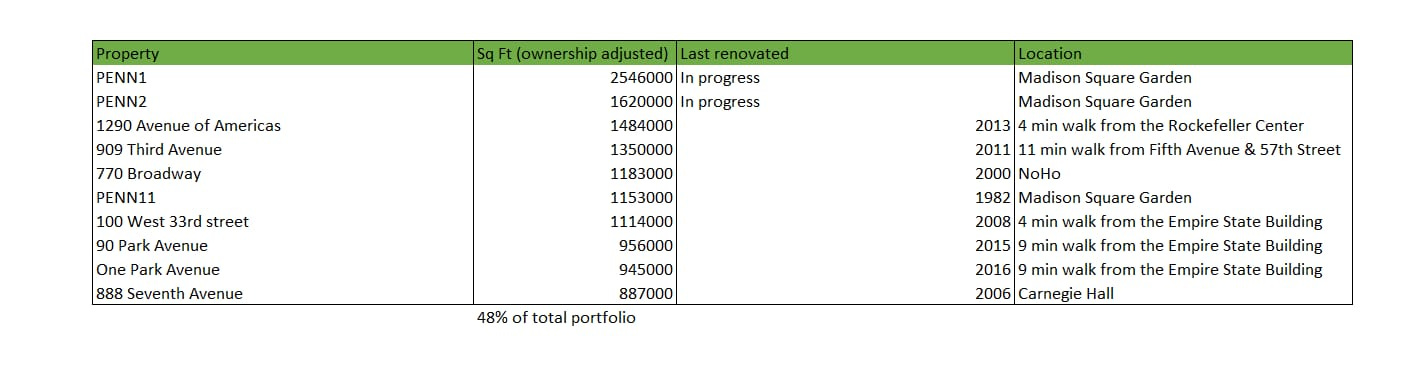

Well - there was indeed asset protection in place here…and during springtime, Vornado’s market cap was equal to the value of just the two buildings they owned. Penn 2 and the Farley building. Both are completely unlevered and the rest you would get for free.

This portfolio. Talk about efficient markets.

Aside from the lessons I've learned from my selling decisions, there are a few more things I'll focus on in 2024.

Hurdle rate

In comparison to 2022, I’m almost fully invested and now have a portfolio of companies I am quite comfortable with. Also, regardless of the run-up in price, I believe that the big asymmetry with all of my positions persists; therefore, I'll raise my hurdle rate even higher.

I want to stay concentrated (maximum 8 positions), thus any new addition should pass a 20–30% hurdle rate (depending on how confident I am in my understanding of the business).

The Spider Web

Another deliberate change I intend to make this year is to "screen" Fintwit.

After my first full year of being active on Twitter, I finally understand what Ian Cassel means by having a spider web of investors. I used to think that the only investors who got ideas from Twitter were those who were lazy and lacked critical thinking. That couldn't be further from the truth.

So this year, instead of doing it "casually" when I feel like it, I'll consciously flip between everyday A-Z turning over rocks and doing deeper work on the ideas that resonate with me on Twitter.

I've already updated my Following list, and I exchange ideas with 20-30 investors I admire on a monthly basis.

Now let's see what the spider web has in store for me in 2024.

Another (dis)advantage of Twitter is the high number of echo chambers. And I've realized that when everyone mocks a particular pocket of the market or is asking, “Why would anyone own this?” it’s time to take a much closer look.

Buying road kill, as Burry likes to call it, and selling it once it's been polished up a little.

While we can all agree that the For You page can be irritating, I believe it may also serve as a great fear tracker when sentiment gets out of wack. Fortunately, that same sentiment tracker helped me go down a rabbit hole on $VNO this spring, which is enough for me to continue paying attention to what Twitter deems disgusting.

So, where await the next extremely pessimistic sentiments, fellas??

Another thing I've recently learned to appreciate are decisions to add or trim a position. I'm not sure yet how or whether I'll put it into action. However, I have seen them prove to be just as valuable as the initial buying position.

For the time being, that is something I will consider more carefully when analyzing companies with higher growth. Adding when the company executes and naturally concentrating my portfolio in this manner.

I've also come to appreciate acting quickly in the micro-cap world, especially when insiders are buying or a large risk is taken off the stable, and you are aware that you know more about the company than 90% of shareholders. Or when mispricing is just dumb and it takes you much less work to validate the thesis.

Most importantly!

My primary focus remains on “these opportunities don’t exist anymore” and “these are impossible to find.”

Those two phrases are like fuel to me. I want to find these companies and I will find them.

To keep this e-mail short, I'll continue my review and send you a full portfolio analysis next week (2023 performance + what I'm tracking in 2024).

So in this spirit, let’s close this e-mail and begin the year with this quote:

“Based on our proprietary research, enlightened superinvestors in financial history are all tireless at exploring unpopular stinky places and turning over countless ugly stones in the dark corners where nobody wants to go near. Joel Greenblatt is such a tireless explorer.” ~ Columbia Class Notes – Joel Greenblatt

I wish you all the luck in 2024, dear readers!

This is NOT investment advice. All content on this website is for entertainment, informational, and educational purposes only and should not be considered to be advice of any nature. Due your own due diligence.

Excellent observations. Nice post.

"So, where await the next extremely pessimistic sentiments, fellas??"

https://www.youtube.com/watch?v=RDrfE9I8_hs

“When an asset-play lacks a catalyst or growth, capital allocation becomes crucial!

Being cheap is not enough. This is where you’ll get a value trap.” - I agree and also made that learning last year.