This is not a drill

digging into $MSV.AX, Mitchell Services

This is a drill. A drilling services company.

If you've been following me for a while, you're probably aware that anything remotely related to metals and mining is not my cup of tea. Only 2 weeks ago, I would have told you that an Australian drilling micro-cap was something that tops the list of companies I'd never dare to invest in.

But it appears that desperate times call for desperate measures, and I did exactly that.

Here is my thesis and the story behind Mitchell Services' transformation.

$MSV.AX

Mitchell Services is the largest provider of mine-site drilling services on Australia's East Coast. They own and operate a fleet of 98 rigs that extract metals, energy and minerals. Out of which, their coal and gold clients are the two most important drivers of business

The company went public in late 2013 through a reverse merger and has since undergone nearly as significant a transformation as Michael Corleone by the end of The Godfather films.

Mitchell's transformation was more positive than Michael's though, so I'll go through it one by one.

Clients

In 2014, only 50% of operating rigs were utilized to serve global Tier 1 clients. Today, that percentage is 88.4%. These include Newmont, South 32, Glencore, Agnico Eagle, Anglo American, and BHP.

This is important since Tier 1s undertake far less „speculative“ activities than junior miners and other smaller clients. Their sites have more long-lasting reserves and operate with the lowest of costs among mining companies. Although all mining businesses are at least partially exposed to the „boom and bust“ nature of the cycle, doing work for resilient Tier 1s should allow Mitchell to maintain most business and keep drilling throughout the cycle. Furthermore, this also allows Mitchell to compete on quality and technical expertise rather than merely price, which Tier 1s value more than other variables. This is most evident when looking at MSV's gross margins, which are both high and stable.

This can act as a barrier for new entrants because Tier 1s don't want to work with the smaller, less reputable guys that come and go with each cycle. Working with Tier 1s also enables you to sign longer-term contracts. For example, Mitchell's typical contract length is 3 years.

Commodity mix

Mitchell's client base diversification efforts were accompanied by changes in the commodity base. The oldest data detailing revenue by commodity given in annual reports was from fiscal 2017. Back then, 51.1% of revenue was generated from coal, 28.6% from gold, and 18.6% from copper, lead, zinc, and silver. Today, the company is more exposed to gold, which now accounts for 42.3% of revenue, and less to copper/lead/zinc/silver which has been nearly cut in half to 10.3%. Steelmaking coal has remained constant at 44.2%.

I understand that this is not a big change, nor a positive one if you're bearish on gold mining activity. However, what met coal and gold combination provides, is a good balance due to the likely near-zero correlation of their commodity cycles. One is used to make steel, while the other acts as a safe haven for central banks or as an input in jewelry for your loved ones.

Drilling type

More important than what you extract is how and where you extract it from. According to the oldest available data from 2015, surface drilling (used in open-pit mining) accounted for more than 96% of revenue that year. Via numerous acquisitions made since, Mitchell Services has been able to diversify more into underground drilling (drilling done underground, of course), which currently accounts for 45.6% of total revenue compared to only 3.8% in 2015. This is significant since underground drilling is highly specialized and faces less competition, allowing you to price it higher and increase your revenue per shift and rig. Surface drilling as a percentage of revenue has decreased to 54.2%.

„It's the same old story, to be honest, it's specialist drilling that's highly technical in nature, where the clients are forced to pay for the technical aspect or a high quality of work, you can price it better. Where it's probably more of a commodity-style drilling and a high level of competition, you're not going to be able to get that exceptional pricing that you can with that other work. And to put that in more context, I think the surface minerals business, again, is the most competitive part of the market. There's a lot of people out there, and it's probably easy to come and go.

When you move into underground, it is more specialized. And again, the switching costs are larger for clients. You then look at underground coal that we operate in, highly specialized work. You look at the work that Scott and his team are doing with deep hole directional diamonds underground, highly specialized work with specialized rigs made out of their workshop in Bendigo. And again, the market is hitting underground, the market is getting deeper. So I certainly think with a lot of specialty work that we do as a team, as a business and where we're positioned.“ ~H1 2020 earnings call

(don’t skip the quotes!)

Capital allocation

The fourth and most important transformation was what piqued my interest in the stock in the first place. In July of 2022, the management unveiled MSV's new capital allocation strategy.

The new strategy was and remains centered on delevering the balance sheet, paying out 75% of earnings in dividends, and buying back stock from surplus rig sales. What was once a business on an aggressive growth journey that heavily diluted shareholders, pursued numerous acquisitions, and used a big amount of growth capex is now a business that puts „shareholders first“ oriented with the aim of returning as much cash flows to shareholders as possible.

„The message is loud and clear that we have spent the money that we needed to spend to put ourselves at the top of the rank. And now, we want to look at returning even shareholder dividends and cash. And as the major shareholder, I can say, that's something that we want to do.“ ~ AGM 2022

Growth capex is now also restricted only to opportunities that meet management's investment hurdles. And these hurdles are high, as you'll see later on, while the dividend has been pushed to 94% payout, even beyond the 75% target.

It has been 2 years since the new capital management strategy was announced, and these are the results since:

Net debt down from 40 million to 1.9 million, 13 million in dividends, and 4.7 million in buybacks completed at an average price of 0.378 (current price is 0.37). That's 57.7 million returned to shareholders in 2 years compared to the current fully diluted market cap of 83 million. Or, in percentage terms, 70% of the market cap and 67% of MSV's present enterprise value have been returned to shareholders in just 24 months. Pretty neat, huh?

With a robust balance sheet in place and high FCF generation, it's not too hard to imagine how capital will be spent in the future.

Hint:

„And to the extent that those free cash flows increase, then so too should be -- should the returns to shareholders.“ ~ Q2 2024

But first, with this quick summary out of the way, it's time to dig deeper into management, why they had a „change of heart“ regarding aggressive growth, and what makes me think the current shareholder-friendly cap allocation strategy is here to stay.

The management

Since taking control of the company in 2013, management has completed four acquisitions and one large growth capex purchase. I would be lying if I didn't say they perfectly nailed the timing. And I mean perfectly.

Their first two acquisitions were made at commodity cycle lows of 2014/15, buying assets from bankrupt competitors. First, they acquired Tom Browne's assets out of receivership for 9.5 million, gaining 29 rigs. Later, in 2015, they purchased Nitro Drilling's 25 rigs for 16.1 million. Also, out of receivership.

To put this in context, in these two transactions, MSV paid on average 320K per rig in 2014 and 644K per rig in 2015. Today, Mitchell Services' average revenue per operating rig is 3.3M.

And to give you an idea of how much the private market value of these rights might be today, here's an example of a similar transaction mentioned in AGM 2022. Indicating the private market value of a similar 10-year-old rig is approximately 1.5 million.

In June this year, as part of the ongoing fleet management, we entered into a sale to dispose of 2 older rigs, 2 rigs that we bought right at the start in 2014. Now in 2014, we purchased those rigs for $400,000, $200,000 each. And under the terms of the sale agreement last, we sold those for $2.5 million. So it gives you some understanding of the value of 100 rigs. ~ AGM 2022

Aside from buying assets from competitors who have been placed in receivership, they have also made two purchases of companies that were profitable at the time Mitchell acquired them and had a more “sophisticated” rig fleet. In 2018, they paid 5.3M, or 2x EBITDA, to acquire Radco Drilling and enter the specialized underground coal drilling market. While in 2019, they paid 3.5x forward EV/EBITDA to acquire Deepcore Drilling for 32M, which specializes in deep hole drilling and has rigs that can reach as deep as 2000M underground.

The final domino of MSV’s growth frenzy was the August 2021 purchase of twelve LF160 rigs for 10M. The appeal of this purchase stems from the fact that these rigs were brand new at the time and could drill automatically, hands-free, which was in high demand among Mitchell’s clients. Even with this one, they nailed the timing right, as this transaction occurred before the interest rate hiking cycle, just as inflation was beginning to ramp up and commodities prices were on the rise.

“Look, I think we have regular strategy sessions with the Board, and certainly something that the Board are very mindful of is what we call the stage of the cycle and where we're at in the market.” ~ 2020 earnings call

Aside from the boosted drilling demand that followed rising commodity prices, the purchase of these rigs also enabled MSV to take advantage of Australia’s instant asset write-off program, significantly reducing its tax bill.

Overall, Mitchell's bargain purchases have resulted in substantial revenue growth from 15M in FY2014 to 236M in FY2024. Profitability followed, and headline EBITDA increased from a negative in 2014 to a positive 40M in 2024. MSV operated an average of 70-75 rigs in FY2024, up from 4 in 2013.

It's all about timing the market, right?

The per-share problem

However, it would be foolish to focus just on the cumulative growth of revenue, EBITDA, or FCF figures and ignore the share count. Unfortunately, MSV's track record on that front hasn't been that pretty. They used stock as a means of financing in the majority of their deals, and the weighted average sharecount went from 27 million in 2014 to 224 million (including ESOP) in 2024.

So to better appreciate the impact of sharecount growth on per share value, it'd be wise to check how EBITDA and FCF have grown on a per share basis over time.

Based on the last 10-years of EBITDA per share numbers calculated using Tikr, as well as the last six years of EBITDA per share and FCF per share numbers that were adjusted for one-offs by my part, it is clear that, despite significant dilution, management has been able to substantially increase per share value since taking over MSV. (you'll understand why I decided to use EBITDA later on)

This is hardly surprising when you look at the list of Mitchell Services' major shareholders.

Nathan Mitchell, the Chairman, owns close to 20% of the company. Scott Tumbridge, non-executive director and the founder of Deepcore, which MSV acquired, owns 7.6%. Furthermore, Peter Miller, another non-executive director, owns about 1%. Other board members own some stock, but not a percentage worth mentioning.

It's safe to say that insiders are well alligned and have the incentive to „get the stock price up.“ This is a stark contrast to most mining-related micro-caps that you'll find on the ASX.

“So we're both in the same boat there. But at the share price of $0.35 to $0.40, it's pretty cheap. And I -- my belief is that at some point in the future, we will be paying good dividends. And at that point, you and I should be getting more dividends and better dividends. So that's my plan. I'm hoping it's the rest of the shareholders' plans. But at the moment, to me, it seems a better option to buy those shares back at $0.35 than to give it out. And that's because I'm a long term -- I'm not looking at it from a short-term position.” ~ H1 2023 earnings call

All of the aforementioned factors tell me that MSV is a type of company where it is okay to look beyond dilution and trust management with capital allocation going forward. Nathan and Andrew Elf (the CEO) think in terms of investment hurdles and ROIC, they have proved themselves with successful counter-cyclical acquisitions and a well executed pivot towards shareholder returns, so I'm not concerned that they'll do a dumb debt-funded acquisition near the cycle-tops or dilute going forward.

“We're not just going to win contracts for the sake of winning contracts at a low price, and it is not at the right margins and we might do it -- we're not going to put the company in a huge amount of debt with regards to potentially what happens in coal in 3 years' time.” ~ 2020 earnings call

On the contrary, I wouldn't be surprised if Nathan Mitchell decides to sell the company if/when the drilling industry begins to exhibit peak-of-cycle type behavior. While running his prior company, he nailed the cycle peak perfectly (again) and sold his company to AJ Lucas for 150M, or 7x trailing EBITDA and 5.6x estimated fwd EBITDA multiple. These multiples were slapped on peak profitability.

It's worth noting that, despite recent increases in labor expenses in the mining sector, about which you can read about daily in the finance paper, management has managed to maintain employee costs fairly tight.

The final bonus point, at least in my head, is that they ceased giving guidance because they found it too difficult and risky.

Now that you know I like and trust the management and am impressed with how they have altered the business and their capital allocation decisions over the last ten years, let's check for how much the market is offering us Mitchell Services today.

Valuation

Based on my normalized FCF numbers, which did more harm than good to MSV's profitability (I'll include them at the end of this article), it's clear that I don't need a DCF to figure out whether something trading at a 20-35% normalized owner earnings yield is cheap.

Unfortunately, my analysis cannot end here as this is still a business operating in a cyclical industry, so one needs to make sure that the next six years will at least be somewhat comparable to the previous six and MSV won't show profitability completely evaporate.

The cycle of life

I'm basing my KPI analysis on six years beginning in FY 19 (ending June 30th, 2019).

This includes both the pre-pandemic and post-pandemic periods. Also, 2019 came after Deepcore and Radco acquisitions, which, as previously mentioned, marked MSV's entry into more specialized drilling, resulting in a substantial increase in average revenue per operating rig. I realize that the 2014-2018 environment would provide a better snap of what „bottom of the market“ profitability might look like. However, comparing a higher mix of commoditized surface drilling with a higher mix of technical underground drilling would not be an apples-to-apples comparison. Also, as I have already stated, the business was exposed to a different commodity mix, worse clients, shorter contracts, and a more fragmented industry at the time.

Four of the most important KPI's I'm tracking to judge cyclicality are utilization rate, average revenue per operating rig, number of shifts worked per average operating rig, and average revenue per shift.

The last two years have seen elevated utilization, and I deem anything above 70% to be "desirable" cycle levels. Management has stated that utilization can never reach 100% because at all times the number of rigs that are stopping, starting, finishing, moving, or being rebuilt, so a good proxy for a fully utilized drilling business is 90%.

I should also mention that 5 out of these 98 rigs are now old, will soon be „out of life“ and won't get rebuilt, so if you adjust for that, the „real“ utilization would be 83% in 2022 and 78% in 2024.

The average revenue per operating rig has increased from 2.5M in 2019 to nearly 3.3M in 2024, a 33% increase. However, to better assess how much of the increase was cycle-driven and how much was just inflation doing its thing, I compared it to the Australian CPI.

Adjusted for inflation, the increase is far more acceptable at 12%.

There's undoubtedly a higher degree of rig activity than in pre-pandemic years, and Mitchell appears to be also benefiting from favorable dry weather conditions, which result in a higher number of shifts done by an average operating rig.

On the other hand, there has been no rise in average revenue per shift over the last six years, indicating that there is still space for pricing improvement. The 2023 numbers are a decent indicator for what can happen to pricing if your rigs are carrying out a more specialized mix of work and you're drilling on the back of rising coal prices.

In the end, I'm left without a firm conclusion about the cycle. Except that drilling activity is elevated, and we're probably closer to the peak than we are to the trough.

To gain a better understanding of the cycle and where it might be heading, I looked for data that could and will impact these KPIs coming outside the company, from the industry.

The life of a cycle

First, let's cover coal, which accounts for 44.2% of total revenue.

It'd be prudent to begin with one key distinction. When I say coal, I'm not talking about thermal coal, which is mostly used for electricity generation and heating purposes. Mitchell has little to no exposure to that. I'm talking about metallurgical coal. This type of coal, also known as cooking coal, is used primarily for steelmaking or, in some minor cases, for the smelting of iron ore. What makes this attractive is that you have no risk of other "green" alternatives taking your business, as you might have with thermal coal. There's currently no viable substitute for met coal.

In the short term, there's definitely a slowdown in coal activity, coming off of late 2022 highs when coal was cooking (pun intended). However, in the medium term, global metallurgical coal demand is projected to rise from 317 million metric tons in 2023 to 331 million metric tons by 2029. While the global steel output is expected to grow at a 1.5% CAGR until 2029.

I definitely won’t get into nuances here to avoid further biasing myself or you, but the more I read about steelmaking coal, the more I concluded that the demand profile supported by infrastructure spending is stable here, whereas the supply is rather limited. Management seems to agree:

„I think it's just going to run out for the next 10, 15, 20 years. There's a couple starting. But I think, as I said before, it's a strong and steady industry. It's not boom and bust. We certainly saw that 10, 15 years ago, they're in the coal industry. I think that at the moment, these guys -- the miners are committed to trying to get out what they need to get out of the ground. And for them to ramp up or ramp down, I think it's difficult. So I think we're pretty busy doing the gas drainage for all those mines up there in the underground. I think they'll just stay steady. I can't see that suddenly people coming in and buying new mines and starting again.“~ Q2 2024 earnings call

Drills and Shovels

The second factor influencing MSV is gold activity. First, let's address the obvious. For more than six months, gold prices have been consistently hitting new highs. As the theory of capital returns suggests, sustained high(er) prices lead to more mining. More mining leads to increased demand for drilling.

While I recognize that there are numerous interconnected factors impacting the price of a certain commodity in the short-term and it would be foolish to simply come up with a narrative on „why something is up,“ I will still provide you with the mainstream narrative on why gold is up in the recent months or years and let you draw your own conclusions.

A combination of expectations around lower interest rates, escalating geopolitical tensions, and just pure momentum is what gold bulls and the media are citing as reasons behind strong gold this year. China helped too with 18 consecutive months of buying gold.

China's Central bank reversed course and halted gold purchases in May of this year, however, while other central banks, including Poland, Turkey, India, Kazakhstan, Singapore, Qatar, and Czechia, continued their buying journey. Another bullish factor for gold going forward is the reversal of gold ETF flows, which have seen outflows since mid-2022 despite rising gold prices but are now finally seeing net inflows in recent months.

To me, the short-term outlook for gold drilling demand appears promising, but the medium-term outlook remains unpredictable, and is most likely dependent on inflation, geopolitics, and people's perceptions of how shiny gold truly is.

With a help of a friend who works in the industry, I was able to find data on gold exploration budget trends at brownfield mine-sites in Australia over the last 15 years.

There should be a strong correlation between exploration drilling demand and this data.

Based on the data presented, my conclusion is that I like the absence of coal and gold correlation, like the stability of coal, and like to see what rising gold prices will bring to the Mitchell's table over the next few years. Unfortunately, I still don't have a firm conclusion about where MSV is in the cycle. One thing I know is that we're somewhere in the middle; I'm not buying 2008 or 2011 highs, nor am I buying 2009, 2015, or 2020 lows. I'll chat with the CEO next Thursday and check what he has to say about the state of the cycle. Given the track record, he certainly knows a thing or two about it.

Until then, my mind remains flexible, my position remains small, and I'll leave it to the smarter commodity market specialist in the room to determine where we're heading next.

Even if Tier 1 spending doesn't prove out to be as resilient and profitability cuts in half from here, 4x EV/EBITDA and 6-10x EV/FCF would still not be an expensive price for what Mitchell Services has become.

One positive tailwind for the drilling industry in general over the long-term is that mineral grades have declined, requiring more drilling to maintain the same output. Moreover, the mining industry in general, faces limited access to capital, leading them to rent drilling services rather than buy rigs and equipment and do it themselves.

Why is the market offering me this opportunity

A questions to always ask yourself.

Obviously, this is an ASX-listed micro-cap whose stock has gone nowhere in the last 10 years. A small business operating in an already hated and underinvested drilling industry with barely 100K dollars worth of shares changing hands on a daily basis. And don't get me started on the ESG mandates around coal, which certainly don't encourage institutions to pile into this thing.

However, there are some less obvious one-off items that are affecting Mitchell's present financials and making it appear more expensive than it actually is.

Despite appearing optically cheap on EV/EBITDA or EV/FCF multiple for some time now, MSV has never appeared particularly cheap on P/E multiple basis. The multiple most widely used by investors screening for cheap stuff.

The only year that sticks out is 2019, with a P/E of 5.9, which coincides with the 10-year high share price of 68 cents compared to the current price of 37 cents.

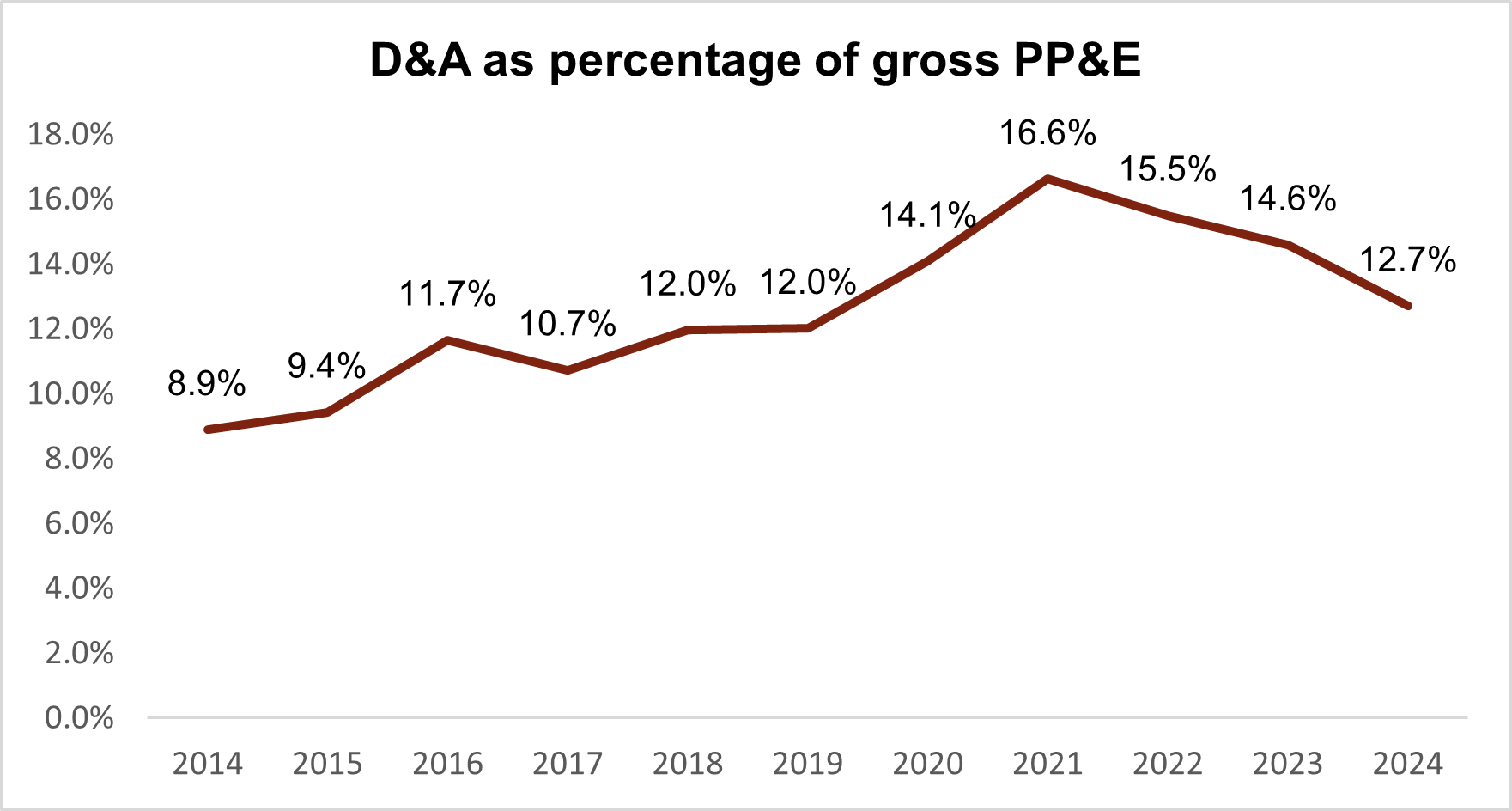

The reason behind understated or, dare I say, hidden earnings in recent years is D&A.

First, as previously shown, Mitchell has historically had a substantially higher debt position, mostly due to equipment financing, which was being amortized quite aggressively through the P&L. Secondly, following the purchase of Deepcore in 2019, MSV has had some intangible assets on its balance sheet that needed to be amortized, particularly customer contracs, which are not a cash-expense and have been fully amortized as of FY2023. Obviously a one-off.

Finally, MSV has benefited from ATO's instant write-off program in relation to capex in fiscal 2021 and 2022, allowing the company to avoid paying tax. The tax advantage will remain in place at least until FY 2025, and the business doesn't expect to pay any income tax until then.

The financial statements are about to change in the future years, with cash flows experiencing a steady decline due to the lack of tax-shield from D&A, while P&L profits will trend higher, closer to FCF (ceteris paribus, of course). The first is a negative for the business; the second is likely a positive for the stock since more value investors will notice how cheap it is.

„The best way I can explain that timing difference, though, is to -- there's about $12 million in ongoing depreciation that will not be allowed as a tax deduction, sort of the flip side of the benefit that we've received previously. So for purposes of anyone's modeling, $12 million of that $25 million, there won't be a tax deduction on.“ ~ Q4 2024

To conclude this section, below is a graph that depicts the relationship between total D&A and what management highlighted as maintenance capex during the last 5 years.

Risks

20–35% normalized owner earnings yield takes care of most risks and makes it hard not to outperform at such a valuation. Still, certain larger risks make me hesitant to make MSV a core position.

First, the annual reports are insufficiently detailed and missing the data that I would want to see. I understand that Mitchell is doing this to avoid revealing any crucial information to its competitors-However, without the necessary information, I am trapped in a position where „I don't know what I don't know.“ For example, in FY2024, MSV had around 5.4M in "other expenses," which weren't addressed or explained in the notes at all.

Quite a few related party transactions that aren't thoroughly explained don't help either.

The second main risk is that I'm completely wrong about the cycle. By my estimates, if utilization rates plummet to below 30-35%, for whatever reason, MSV's FCF will turn negative, and if utilization plummets to below 25-30%, MSV should be unprofitable on an EBITDA basis. I doubt this scenario is plausible, but it is something to consider when investing in drilling businesses that aren't exactly at the bottom of the cycle.

MSV does have ways to prevent the cash bleed by sacking people and putting their rigs on "standby“ mode.

“My father always said to me, if you're not making new money mill park them on the side, and that stands true today. I think you try and get the rig working on good margins, otherwise don't get it working” ~H1 2023

However, if we have another sever mining recession and 2013-2016 type of environment becomes the „new normal.“ I'm likely lose money or underperform the market even at this valuation.

The third and last major risk comes from client concentration.

Risks in the short term—the ones I'm not paying much attention to—include Grosvenor mine fire, continuation of softer utilization numbers observed in June 2024, perhaps rainy weather, and probably a less specialized mix of work for coal. So we're probably heading into a softer year.

One „upside risk“ worth mentioning is a recent JV foray into decarbonization solutions. You can learn more about it in the most recent two earnings calls.

“So that is a very exciting growth opportunity for the company. It's probably the first time since the early 2000s when coal seam gas started that you're seeing a whole new potential total available market for drilling. But as I said, it's very early days, and it's going to take some time to come on.”

Obviously, continuation of a positive cycle for commodities and drilling would push profitability above the 20% internal EBITDA margin target, or to 50-60M in EBITDA on an 86M enterprise value.

That's enough from me for today. I still have some things on my mind that I want to say about MSV, but I think it's best if I wait until after my meeting with the management. This write-up is already longer than usual.

Thank you for reading!

disc: I have a ~3% position and will probably add if it drops to 34 cents per share

This is NOT investment advice. All content on this website is for entertainment, informational, and educational purposes only and should not be considered to be advice of any nature. Due your own due diligence.

Great insights to the company. FYI there are 3 other write-ups on the name that each have a similar thesis overall, but with each one in its own flavor (and more condensed):

https://roguefunds.substack.com/p/mitchell-services-is-a-potential-4-bagger-hidden-by-a-tax-write-off-scheme

https://valueinvestorsclub.com/idea/Mitchell_Services_Ltd/2377650240

https://overandunder.substack.com/p/mitchell-services-msv

Cheers

Great Read!