In medias res

$RCS.MI $BHU.SI $LDB.MI $CARD.L $VNO $8881

After reflecting on my wins and losses in the last post, in this quick article, I'd like to provide you with an update on 6 of my current holdings and the KPIs and catalysts I’ll be looking at for each of them in 2024.

This is what the portfolio looks like as of January 13, 2024. With inflows from my salary, soon enough I’ll have enough spare cash to buy another large position.

Let’s go from the smallest to the largest position:

$8881 – Nisshin Group Holdings

To be honest, I don't have much to say about Nisshin. The combination of cheapness (0.5x P/NCAV) and positive changes in capital allocation mentioned in the July write-up makes me sleep well at night. This one doesn’t take much mental space and I only check it briefly, once a quarter. IMO It’s only a matter of time before the market realizes that Nisshin doesn’t deserve to be a net-net, and I’m comfortable with the dividend in the meantime. Recent positive developments in the Japanese market should only help this.

$VNO- Vornado Realty Trust

For me, the half of the position I decided to keep in December is the closest thing to a never-sell that I have in the portfolio. If it doesn’t get egregiously overvalued, I won’t be making any changes to this one. Owning real estate in the heart of the world's capital and buying it in what is arguably the most pessimistic market environment that it has ever been through is something I don’t want to give up easily. I too like Roth and the team very much and am impressed with their long history, even before Vornado was a REIT. Also, I am confident they’ll do a decent job navigating this tougher WFH and higher-interest rate environment going forward and will come out as a winner as the industry consolidates.

The PENN district prospects excite me too.

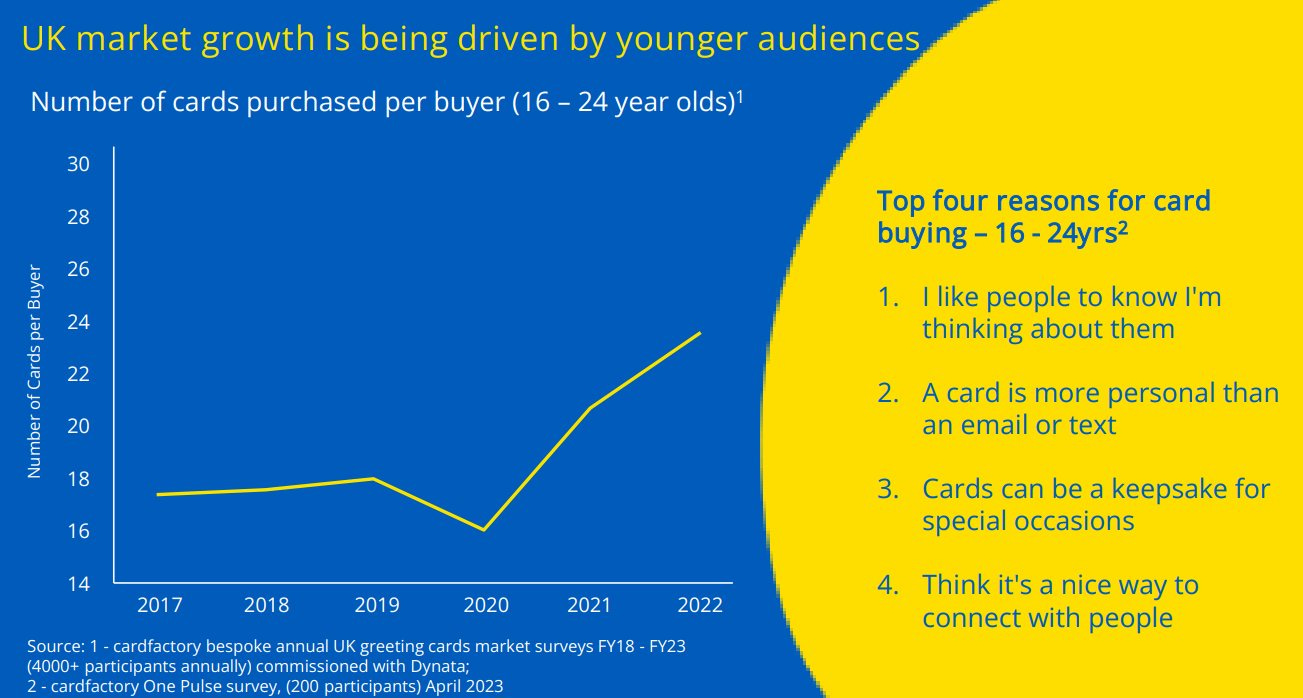

$CARD.L – Card Factory Plc

My most recent addition to the portfolio in October was $CARD.L. UK’s only vertically integrated retailer of greeting cards (and celebration gifts and “essentials” that come with them). Almost four years have passed since Card Factory was deemed a business of the past by Wall Street, and, even to this day, it is always a reliable source of negative news, regardless of how the company performs. As a result, despite the recent run-up, it still only trades at a TEV of 550M while it is on track to generate >100M in FCF this FY.

The good news is that Card Factory has now completed its deleveraging, and when debt covenants expire at the end of January, I expect them to begin paying a 6–8 cent dividend next year, resulting in a 5.5% to 7.5% yield on the current price of 108 GBX. The company reported both the highest revenue and highest gross profit figure on record this H1, and the net profitability in the same half was on par with the results recorded before COVID, so I see no reason to expect H2 to be lower. Especially now that they’ve reorganized their store layouts, expanded their gift and non-card offerings, reduced rents, and successfully hiked prices in targeted categories.

In the last period they were reporting this type of results, the stock was trading at no less than 200 GBX per share and as high as 400 GBX. So, let’s see if it can reach similar levels in the next few years, now that selling pressure on the stock will probably subside as the largest holder, Teleios Capital, exits its position.

Some KPIs that I’m paying close attention to with this one is: the number of adults that bought a card in the last year, retail volume and value of cards, how they managed inventory this Christmas season, more competitors going bust or downsizing their store footprint and, of course, LFL.

A positive surprise for investors in 2024 would be a special dividend announcement or the initiation of a buyback. Though I think both are not that likely.

Online still remains the weakest link of the business; however, their click-and-collect strategy combined with the largest store footprint in the UK and the recently implemented ERP makes a lot of sense to me

$LDB.MI – Lindbergh SpA

Interesting news came from Lindbergh this Thursday. Sun Mountain Fund LP, an institutional investor based in Boston, has bought a 3.86% stake in the company.

I feel optimistic about this development since one of the two managers running the fund is none other than Will Thorndike, the author of arguably the best book on capital allocation ever written, The Outsiders. Also, this is the first time I've been aligned with a well-known investor in a micro-cap company, and I’m very curious how Will discovered a 20M market-cap Italian business trading on the secondary stock exchange.

The few things that I’m keeping an eye on with Lindbergh in 2024 are: successful contract renewals and/or price increases (like the one done with Bosch and Kone in December), implementation of waste management and overall progress in France (WM would be a big, big positive) and how many firms/technicians they will be able to add + the ARPU.

I sleep well with this one as one of my larger holdings. Lindbergh is a team of killers.

$BHU.SI – SUTL Enterprise

There is not much to add since I outlined my thesis in August, except that the stock price is a bit higher, but the earnings are better than expected. H1 results were great, and I expect the positive industry prospects and the growth alone should take care of the remaining discount.

H1 2023:

pretax profit of 5.2M for, 23% YOY growth

4.7M in OCF, 21.9% YOY growth

60M market cap, 6M enterprise value atm

And if good capital allocation trends persist, this might just be an excellent investment. Let's keep track of it.

$RCS.MI – RCS Media Group

A good old friend reported satisfactory results in 2023 and remained the undisputed leader on both the Italian and Spanish markets. Gazzetta was impressive again; it retained its position as the most-read Italian newspaper and grew its online subscriber base by 52% YoY to 211 thousand subscriptions in the first 9M of 2023.

Also, especially strong results came from the RCS Sport subsidiary, which organizes world sporting events, including Giro d’Italia. It recorded 35% growth in 2022 to 40+ million in EBITDA, which was sustained in 2023 as well. This is particularly interesting given that the Saudi sovereign fund PIF has declared an interest in acquiring it and entering the cycling market. However, allegedly, Cairo appears to be unwilling to sell unless he gets a huge offer.

And if the world of football taught us one lesson last year, it would be that the Saudis are willing to spend as much money as possible to enter the sports market. I wouldn’t be surprised if they offered anywhere between 10-15x EBITDA, which at that point would be equal to 1-1.5x RCS’s current market cap. I think Cairo will try to further monetize Giro d’Italia and then try to sell, but that’s just speculation, and I still like the risk-reward if nothing were to happen.

I still think that the chance that this works out vs. loses money remains asymmetric. My friend @SchopenhauerCap said it best;

A dividend increase, a share buyback (already authorized but not announced or executed), an RCS Sports sale, Marca spin-off. Cairo doing M&A in this dirt-cheap environment for the media industry.

I consider Cairo a very rational person and think that at least one of the mentioned corporate activities is likely and will unlock the “true value” of the business. Until then, I’m fine waiting and getting paid an 8% dividend.

Except for corporate actions, I’ll continue to keep an eye on digital subscriber growth, look for mentions of price increases in their digital offerings, and monitor the paper cost situation and the stability of gross margins.

That’s all from me, folks. Thanks again for reading!

P.S. It’s been a while since I've found a $5 billion+ company appealing, but $PARA looks more than interesting to me here, so if you have any useful insights, feel free to reach out.

This is NOT investment advice. All content on this website is for entertainment, informational, and educational purposes only and should not be considered to be advice of any nature. Due your own due diligence.

Note: FCF number for $CARD.L mentioned in the write up is FCF that is not adjusted for leases and the TEV number is EV + leases

I guess, if it was close to 1.5 I'd start thinking about it. Thinking, not selling